Invest in the best stock opportunities right now and every-time.

Start Systematic Stock Investing ...in less than a minute.

Go Digit General Insurance

Profile of the company

The company is one of the leading digital full stack insurance companies, leveraging its technology to power what it focuses to be an innovative approach to product design, distribution and customer experience for non-life insurance products. Full-Stack Insurers are insurance firms that are fully licensed and controlled by a regulatory authority and perform sourcing, underwriting and servicing all in-house. Digital full stack insurers are insurance manufacturing companies that focus on integrating technology in their operations. The company offers motor insurance, health insurance, travel insurance, property insurance, marine insurance, liability insurance and other insurance products, which the customers can customize to meet his or her needs. As a digital full stack insurance company, it deploys a combination of insurance and technology solutions to assist in enrolment, insurance claims processing, underwriting, policy administration, data insights and fraud detection. The company also offer its products directly to customers through its website and through web aggregators. Since the commencement of its operations, in relation to its motor vehicle insurance, it has focused on underwriting policies and collecting data in states or areas containing prospective customers with more preferred risk profiles, in compliance with applicable data protection norms.

The company’s technology platform supports its product design by enabling the incorporation of a modular product architecture and provides the backbone for its application program interfaces (API), applications, portals and website that allow customers and partners to engage with it conveniently. Its insurance products, supported by its technology platform, help its customers to secure the right coverage to protect the things they love at a price that suits their budget and empower its distribution partners to improve their sales process and productivity. These technologies enable it to achieve underwriting in an efficient manner, which is a differentiator among insurers. Further, the company uses various data points when underwriting insurance for a new customer which will vary depending on the type of insurance. Relevant material data points may include the vehicle make, model, subtype and vehicle value, the address and name of the customer, the scope of coverage and the age of the customer.

Further harnessing its technology platform, it has developed predictive underwriting models that leverage the insights gathered by its data bank. Its predictive underwriting models aid it in determining and targeting the markets and customers in India that are expected to be more profitable and hence, allows it to accurately price its coverage. It also has modular APIs that allow it to share data between its systems and its partners’ third-party website and/or portal in a specified manner, allowing it to reduce human intervention. It integrates APIs in its business across products for policy issuance, policy servicing, payments and claims. Its blend of a simple and tailored customer experience, technological integration and pricing enjoys broad appeal, including for customers who are new to purchasing insurance.

Proceed is being used for:

Industry overview

As of Financial Year 2023, the GDP of India is approximately $3.73 trillion and the non-life insurance market was $33.30 billion measured by GWP, as per the General Insurance Council. This indicates a non-life insurance penetration rate of 1.0% (as measured by GWP) with significant room for improvement. The global average insurance penetration amounted to 4.0% among leading global economies, with the 2022 penetration rate of China and the United States at 1.9% and 9.0%, respectively. In addition, the non-life insurance density in India was $ 23.00 as of Financial Year 2023, measured by premium per capita, which is the lowest across some of the largest markets in the world with a global average at $ 499.00 as of calendar year 2022. Low penetration in the insurance industry stems from financial illiteracy, lack of awareness of need and sufficiency of insurance, low household disposable income, complex products, gaps in product offerings and inefficiencies in the distribution system. High penetration rates amongst leading global markets are also driven by mandatory insurance policies. Other reasons include better quality of life and higher life expectancy, which have led to lower premium rates being offered in those nations. Furthermore, traditionally, customers have been wary of purchasing insurance products due to unfamiliar terms, confusing jargon-laden documentation, and uncertainty around the claims settlement process. This creates opportunities for players seeking to disrupt the market with products crafted with simplicity and transparency.

India’s insurance regulatory body, the IRDAI, has been undertaking targeted initiatives to promote transparency and efficiency in the non-life insurance market, insurance penetration and customer experience. The regulatory body has also taken steps to advance technological integration within the industry. One key driving changes across the industry is “Insurance for All by 2047”. The initiative aims to provide life, health, and property insurance coverage to every citizen. To achieve this ambitious goal, IRDAI is implementing a comprehensive strategy that includes promoting microinsurance products for low-income groups, collaborating with the government on social welfare schemes such as PMJAY for health insurance, and enhancing financial inclusion by integrating insurance with existing programs. Furthermore, IRDAI is advocating for standardized insurance plans to facilitate easier comparison and is leveraging technology to streamline processes and enhance accessibility, particularly in rural areas. Through initiatives aimed at bolstering financial literacy and ensuring efficient claim settlements, IRDAI is committed to building a future where every Indian can benefit from the security provided by insurance coverage.

Pros and strengths

Simple and Tailored Customer Experience: The customer experience is core to what it does. Insurance products have historically been hard to understand and sign up for, and making and settling claims has been cumbersome. It is dedicated to establishing trust and promoting transparency in its relationships with its customers by simplifying insurance and offering easy-to-understand, customizable products that enhance its customers’ experience. Its focus on the customer experience has resulted in high customer satisfaction, evidenced by its net promoter scores of 73.3% for non-claims and 93.1% for motor claims as of December 31, 2023, and high customer satisfaction by users of its “Digit Insurance” mobile application available on android and iOS. Its products are designed to be relevant and customizable in order to meet the needs of each of its customers. During the application process, its customers can select from a menu of coverage options with transparent pricing across its portfolio of products, allowing them to opt for coverage according to their needs and budget.

Focus on Empowering Distribution Partners: The company is dedicated to establishing a ‘partnership’ in its relationship with its distributors. Its distribution partners include individual agents, POSPs, corporate agents, motor insurance service providers (MISPs) and brokers. The company’s customer journeys are tailor-made to each distribution partner with engagement at three levels: Engagement with distribution partners to optimize possibilities; Product design that is relevant and customized to its partners’ customer base, enabled by the modular product architecture in its technology platform; and Customer journeys that are developed to align with its Business Process, IT, Operations and Customer Service functions, managed by its Project Office. Its partners range from older agencies to new non-bank financial companies, and each has a different way of operating and a different level of technical capability. It understands these differences and extend its technology and expertise to its distribution partners to develop customized solutions that provides them with the tools, products, information and support to effectively target and service customers.

Predictive Underwriting Models: The company has combined its expertise in the motor insurance market with its data bank to build extensive underwriting models that it uses to accurately assess risk and predict losses for its motor insurance products at a granular level. This allows it to better manage its costs, and in turn allows it to better tailor its products to serve more customers, which provides it with more data, completing a pricing feedback cycle that helps it to continue to refine its products and lower its costs. It utilizes data from its existing policies and prior claims experience to develop predictive models that generate insight into the risk of loss associated with a particular application. Thus, it has a good understanding of a customer’s risk profile upon which to base its underwriting decisions. Aided by its technology platform, its automated underwriting models for its personal lines of business can aggregate and interpret a vast set of variables across geographies, product risks and customer types. It is currently able to issue all of its motor, and retail health insurance applications on an automated basis, which, it leads to efficiency and lower costs.

Advanced Technology Platform: The company’s technology enables it to achieve efficient underwriting, which is its differentiator among insurers. It builds technology-enabled solutions and employ a hybrid model of AI-enabled analytics and human assessment to streamline the value chain, aids its customers, partners and employees and drive efficiency. Around the core of its technology platform, it has developed in-house microsystems, that allow it to facilitate a range of routine tasks, from policy design, underwriting, pricing and issuance to servicing and claims management. Its platform is entirely cloud-based, making its system agile, connected and scalable. It utilizes its technology platform to simplify the insurance process, empower its customers and partners and allow customers to customize insurance features, such as pricing and coverage.

Risks and concerns

Subject to extensive supervision and regulatory inspections by IRDAI: In the regular course of the company’s business, it has received various queries, clarifications and observations from IRDAI. The IRDAI conducted an onsite inspection of the company on Digit Contractual Liability from October 10, 2022, to October 13, 2022. The company received an inspection report vide email dated January 27, 2023, from IRDAI in reference to the said inspection (Inspection Report). The company was directed to respond to these observations within 7 days from the receipt of the inspection report. After being granted an extension of time, the company filed its reply dated February 28, 2023, and provided responses to the observations raised in the Inspection Report. The company stated that compliance of any directions/advice will be undertaken. The matter is currently pending with the IRDAI. Failure to address or satisfactorily address queries and clarifications from IRDAI or other regulatory authorities in a timely manner or at all may result in it being subject to statutory or regulatory actions, directions to take remedial action and/or monetary penalties. Because any regulatory action in response to any IRDAI inspection report or query is subject to inherent uncertainties and complexity, there can be no assurance as to such actions’ outcome and extent, or that any such actions or other penalties will not have a material adverse effect on its business, prospects, financial condition and results of operations.

Rely on motor vehicle insurance products: Sales of the company’s motor insurance products have largely been driven by the continued growth in consumer demand for motor vehicles in India. It cannot assure that such growth in consumer demand for motor vehicles in India will continue in the future. As a result of the substantial amount of revenue it derives from motor vehicle insurance products, in particular, any material deviation in the projected businesses and claims ratio focused on its motor insurance business may have a more exacerbated impact on its business, financial condition, results of operations and prospects. As a result of any adverse changes in consumer demand for motor vehicles in India and/or any unfavourable change in government policies which may affect such demand, the revenues derived from motor vehicle insurance products could be lower than its expectations. This could have a material adverse effect on its business, financial condition, results of operations and prospects.

Credit risks related to investments and day-to-day operations: The company is exposed to credit risks in relation to its investments. As of December 31, 2023, 97.3% of its assets were invested in Indian government securities or corporate bonds. Of its corporate bond exposure, as of December 31, 2023, 71.8% was invested in AAA rated bonds rated by all SEBI authorised credit rating agencies. The value of its debt portfolio could be affected by changes in the credit rating of the issuer of the securities as well as by changes in credit spreads in the bond markets. In addition, issuers of the debt securities that it owns may default on principal and interest payments. Furthermore, the counterparties in its investments, including issuers of securities it holds, counterparties of any derivative transactions that it may enter into, and banks that hold its deposits and debtors, may default on their obligations to it due to bankrulptcy, lack of liquidity, economic downturns, operational faiure, fraud or other reasons beyond its control, and its rights against these counterparties may not be enforceable in all circumstances. Any of the foregoing could significantly decline or eliminate the value of its debt portfolio, and have an adverse effect on its financial condition, results of operations and prospects.

The company’s investment portfolio is subject to liquidity risk which could decrease its value: Some of the company’s investments may not have sufficient liquidity as a result of a lack of market makers, market sentiment and volatility, and the availability and cost of credit. In these circumstances, its ability to sell its investment assets without significantly depressing market prices may be limited, or it may be unable to sell its investment assets at all. If it is required to dispose of these or other potentially illiquid investment assets on short notice due to significant number of insurance claims to be paid, a large claim to be paid, significant fall in value of its liquid investment assets, or for any other reason, it could be forced to sell such investment assets at prices significantly lower than the prices it has recorded in its financial statements. As a result, its business, financial condition, results of operations and prospects could be materially and adversely affected.

Outlook

Incorporated in December 2016, Go Digit General Insurance is an insurance provider offering motor insurance, health insurance, travel insurance, property insurance, marine insurance, liability insurance and other insurance products, which customers can customize to meet their needs. It has designed its underlying business model to minimize dependency on any single line of business. It offers a broad suite of products to satisfy its customers’ needs in motor, health, travel, property, marine, liability and other insurance lines. It launched 74 active products across all business lines. In addition, it constantly focuses on product innovations which help it satisfy real unmet insurance needs. It also offers its products directly to customers through its website and through web aggregators. Since the commencement of its operations, in relation to its motor vehicle insurance, it has focused on underwriting policies and collecting data in states or areas containing prospective customers with more preferred risk profiles, in compliance with applicable data protection norms. On the concern side, the company will continue to incur expenditure in maintaining and growing its existing business. It cannot assure that it will have sufficient capital resources for its current operations or any future expansion plans that it may have. While it expects its cash on hand and cash flow from operations to be adequate to fund its existing commitments, its ability to incur borrowings is dependent, in part, upon the success of its operations.

The company is coming out with an IPO of 9,83,71,043 equity shares of face value of Rs 10 each. The issue has been offered in a price band of Rs 258-272 per equity share. The aggregate size of the offer is around Rs 2537.97 crore to Rs 2675.69 crore based on lower and upper price band respectively. On performance front, the company’s income from investments (revenue account) increased from Rs 3,552.34 million in Financial Year 2022 to Rs 6,165.61 million in Financial Year 2023, an increase of 73.6%, primarily due to an increase in its AUM. Besides, the company has recorded a profit after tax of Rs 355.47 million in Financial Year 2023. It incurred a loss after tax of Rs 2,958.51 million in Financial Year 2022. Meanwhile, the company intends to continue to form new distribution partnerships to broaden its customer reach and use technology and innovation to target customers with insurance needs. It strives to increase its GWP among tech savvy customers and partners by building partnerships and ongoing engagement, including gathering insightful user data-points which, in turn, will improve its ability to create relevant insurance products. Going forward, it intends to maintain a healthy product pipeline focused on continuing its track record of innovation.

| Company Name | CMP |

|---|---|

| ICICI Prudential | 545.00 |

| Go Digit General Ins | 298.45 |

| Star Health and Allied | 519.70 |

| Life Insurance Corp | 1012.70 |

| HDFC Life Insurance | 550.10 |

| View more.. | |

MoneyWorks4Me rating and ranking of funds for SIP is available to subscribers only. Moneyworks4Me is not a rating and ranking agency, however it is required that users have a way of selecting funds and building a Portfolio. The method used by it are described below to enable users to understand the logic behind the rating and ranking Subscriber will find more details on this in the various content made available from time to time. In case you need more please write to besafe@moneyworks4Me.com

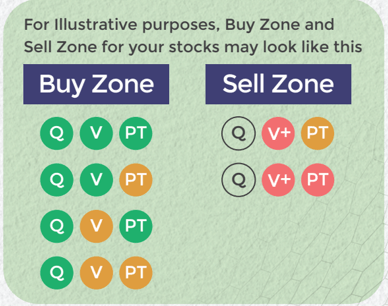

MoneyWorks4Me rates and ranks mutual funds based on the following data-driven system:

Funds ranking in screeners: Performance Consistency and Quality are two parameters used for ranking funds for SIP. The ranking as follows GG, GO, GR, OG, OO, OR, RG, RO and RR.

With the same color-coded funds, the one with the higher Average 3-year rolling returns (over 5 to 10 years), the number that appears in the Performance tag, ranks higher.

Here is the summary:

The third tag Upside Potential is not relevant for SIP. It is relevant for lumpsum investments in Mutual Funds.

Buy quality Stocks when they are available at reasonable prices and supported by an upward price trend and Sell when they are Overvalued using the Decizen Rating System. Covers 3500+ stocks

Download APP

Download APP