Create stable, long-term investment portfolio with strong, consistent stocks.

Start Research-backed Investing ...Now.

Indian equity benchmarks made a second straight day of gains on Friday, shrugging off weak global cues. Headline indices opened higher and traded in green for most part of the day as provisional data from the NSE showed foreign institutional investors (FIIs) bought shares worth Rs 1,513.41 crore on January 4. Sentiments remained positive with the United Nations (UN) World Economic Situation and Prospects (WESP) 2024 report stating that India’s Gross domestic product (GDP) growth is projected to remain strong at 6.2 per cent in 2024 mainly supported by resilient private consumption and strong public investment. It also said that GDP in South Asia is projected to increase by 5.2 per cent in 2024, driven by a robust expansion in India, which remains the fastest-growing large economy in the world. Some support came in with a private report that India is likely to project higher economic growth estimates of around 7% for the 2023/24 fiscal year ending in March, compared with earlier government forecasts when the National Statistical Office releases its first advance GDP estimates on Friday.

However, markets gave up early gains to slip in red in late afternoon deals, as traders turned cautious with a private report that the JN.1 subvariant has become the dominant Covid-19 variant in India, accounting for more than 60% of the coronavirus cases in the country. As of Thursday, 511 cases of the subvariant JN.1 have been reported across the country. India recorded 760 new Covid-19 cases and two deaths, while the active caseload saw a slight dip to 4,423 from 4,440 on the previous day. Some concern also came with Secretary in the Department for Promotion of Industry and Internal Trade (DPIIT) Rajesh Kumar Singh stating that India will have to eventually move to a lower customs duty regime and cannot continue to protect domestic manufacturers by citing infant industry argument. However, markets soon regained traction to end higher, taking support from data showing that India's services sector ended 2023 on a firm footing, with activity expanding at its fastest pace in three months in December on buoyant demand and an optimistic year-ahead outlook. The HSBC India Services Purchasing Managers' Index, compiled by S&P Global, rose sharply in December to 59.0 from November's one-year low of 56.9

On the global front, European markets were trading lower as investors awaited euro area consumer and producer inflation reports as well as U.S. non-farm payrolls data later in the day for important clues as to whether the European Central Bank and the Federal Reserve would cut interest rates this year. Fears of an escalation of the Israel-Hamas war into a broader regional conflict also dented investor sentiment. Asian markets ended mostly lower on Friday as traders remained cautious amid renewed uncertainty about the outlook for interest rates following the release of the minutes of the US Fed's latest monetary policy meeting earlier in the week. They now look ahead of the closely watched monthly US jobs report for further cues.

Finally, the BSE Sensex rose 178.58 points or 0.25% to 72,026.15 and the CNX Nifty was up by 52.20 points or 0.24% to 21,710.80.

The BSE Sensex touched high and low of 72,156.48 and 71,779.83, respectively. There were 15 stocks advancing against 15 stocks declining on the index.

The broader indices ended in green; the BSE Mid cap index rose 0.19%, while Small cap index was up by 0.61%.

The top gaining sectoral indices on the BSE were IT up by 1.29%, Capital Goods up by 1.27%, TECK up by 1.03%, Industrials up by 0.97% and Telecom up by 0.59%, while Basic Materials down by 0.43%, Healthcare down by 0.29%, Consumer Durables down by 0.24%, Metal down by 0.16% and Utilities down by 0.11% were the top losing indices on BSE.

The top gainers on the Sensex were TCS up by 1.93%, Larsen & Toubro up by 1.62%, Infosys up by 1.37%, Axis Bank up by 1.16% and HCL Technologies up by 1.13%. On the flip side, Nestle down by 1.65%, JSW Steel down by 1.06%, Kotak Mahindra Bank down by 0.83%, Sun Pharma Industries down by 0.78% and Asian Paints down by 0.71% were the top losers.

Meanwhile, the rating agency -- Icra has said that revenue of 25 leading domestic pharmaceutical companies is expected to grow 9-11 per cent in the current fiscal year (FY24). The projected revenue growth in 2023-24 will be primarily supported by 11-13 per cent expansion in the US market and 7-9 per cent growth in the domestic market, while revenues from the European market and emerging markets are expected to rise 11-13 per cent and 13-15 per cent, respectively.

Icra expects the revenues of a sample set of 25 Indian pharmaceutical companies (which account for 60 per cent of the overall revenues of the Indian pharmaceutical industry) to expand by 9-11 per cent in FY24, post a year-on-year growth of 10 per cent in FY23. Icra said it foresees research and development expenses for its sample set of companies to stabilise at 6.5-7 per cent of their revenues as they will optimise spending, focusing more on complex molecules and specialty products against plain vanilla generics. The US has always been a key market for most leading Indian pharmaceutical companies, accounting for a sizeable share of their revenues.

However, it stated the share of revenues from the US market for Icra's sample set of companies declined to 35 per cent in FY22 as compared with 40 per cent in FY20, owing to consistent pricing pressure, lack of major blockbuster products going off-patent and increased regulatory scrutiny in recent years. Nonetheless, with the easing of pricing pressure, significant new launches, and shortages of some products, the same increased to 37 per cent in FY23 and 38 per cent in the first half of FY24.

The CNX Nifty traded in a range of 21,749.60 and 21,629.20. There were 23 stocks advancing against 27 stocks declining on the index.

The top gainers on Nifty were Adani Ports & SEZ up by 2.65%, Larsen & Toubro up by 2.60%, TCS up by 1.96%, SBI Life Insurance up by 1.60% and LTIMindtree up by 1.37%. On the flip side, Britannia Industries down by 1.62%, Nestle down by 1.61%, JSW Steel down by 1.04%, Kotak Mahindra Bank down by 1.01% and Divi's Laboratories down by 0.99% were the top losers.

European markets were trading lower; UK’s FTSE 100 decreased 66.76 points or 0.86% to 7,656.31, France’s CAC fell 80.25 points or 1.08% to 7,370.38 and Germany’s DAX lost 123.97 points or 0.75% to 16,493.32.

Asian markets ended mostly lower on Friday ahead of key US payrolls data due out later in the day. Market sentiments weakened further by tracking Wall Street’s fall overnight as strong labor market data fueled uncertainty about early interest rate cuts by the Federal Reserve. Meanwhile, Chinese and Hong Kong shares leading regional losses on persistent concerns over economic recovery, while four Chinese bad debt managers were downgraded by Fitch Ratings in line with concerns over their financial situation and hopes of reduced government support. Although, Japanese shares gained as a weaker yen boosted exporters.

Asian Indices | Last Trade | Change in Points | Change in % |

Shanghai Composite | 2,929.18 | -25.17 | -0.86 |

Hang Seng | 16,535.33 | -110.65 | -0.67 |

Jakarta Composite | 7,350.62 | -9.14 | -0.12 |

KLSE Composite | 1,487.61 | 10.35 | 0.70 |

Nikkei 225 | 33,377.42 | 89.13 | 0.27 |

Straits Times | 3,184.30 | 10.29 | 0.32 |

KOSPI Composite | 2,578.08 | -8.94 | -0.35 |

Taiwan Weighted | 17,519.14 | -30.51 | -0.17 |

MoneyWorks4Me rating and ranking of funds for SIP is available to subscribers only. Moneyworks4Me is not a rating and ranking agency, however it is required that users have a way of selecting funds and building a Portfolio. The method used by it are described below to enable users to understand the logic behind the rating and ranking Subscriber will find more details on this in the various content made available from time to time. In case you need more please write to besafe@moneyworks4Me.com

MoneyWorks4Me rates and ranks mutual funds based on the following data-driven system:

Funds ranking in screeners: Performance Consistency and Quality are two parameters used for ranking funds for SIP. The ranking as follows GG, GO, GR, OG, OO, OR, RG, RO and RR.

With the same color-coded funds, the one with the higher Average 3-year rolling returns (over 5 to 10 years), the number that appears in the Performance tag, ranks higher.

Here is the summary:

The third tag Upside Potential is not relevant for SIP. It is relevant for lumpsum investments in Mutual Funds.

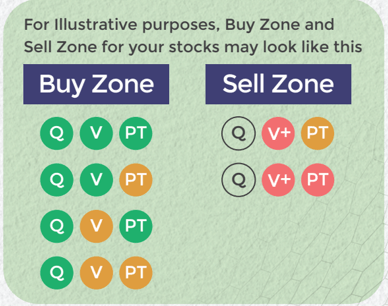

Buy quality Stocks when they are available at reasonable prices and supported by an upward price trend and Sell when they are Overvalued using the Decizen Rating System. Covers 3500+ stocks

Download APP

Download APP