Create stable, long-term investment portfolio with strong, consistent stocks.

Start Research-backed Investing ...Now.

Indian equity markets traded higher most part of the day and concluded the trade with gains of above half a percent. Traders were hoping that Reserve Bank of India (RBI) likely to keep interest rate unchanged for the sixth consecutive time at 6.5 per cent. Traders were seen piling up positions in IT and Oil & Gas sectors’ stocks. The broader indices, the BSE Mid cap index and Small cap index ended with gains of over a percent.

Markets made optimistic start and maintained their gains amid Foreign fund inflows. Foreign institutional investors (FIIs) net bought shares worth Rs 518.88 crore on February 5, provisional data from the NSE showed. Traders took encouragement as the Organization for Economic Co-operation and Development (OECD) raised India’s growth outlook for 2024-25 (FY25) to 6.2 per cent from the 6.1 per cent estimated earlier in its November outlook. Traders took note of report that S&P Global Ratings said India’s sovereign rating support may strengthen over time if the next government - post general elections - could fund large infra projects without widening the country’s current account deficit and can shrink the fiscal deficit significantly. Indices continued to trade in green in afternoon session. Some support also came in as according to data from the Central Depository Service and National Securities Depository, the number of demat accounts opened in January totalled over 46.84 lakh, compared to 40.94 lakh a month ago and 21.90 lakh a year ago. The total demat tally crossed 14.39 crore, up 3.4 percent from a month ago and 30.3 percent from a year ago. Markets traded in fine fettle till the end of the session as investors continued to hunt for fundamentally strong stocks.

On the global front, European markets were trading mostly in green after BP Plc unveiled more share buybacks and announced plans to boost shareholder returns. Asian markets ended mostly higher with Chinese and Hong Kong markets rallying after a government investment fund said it would expand purchases of stock index funds to counter heavy selling in the Chinese markets. Back home, India is likely to sign a multi-billion-dollar deal to extend LNG imports from Qatar till 2048 at rates that are lower than current prices.

The BSE Sensex ended at 72,186.09, up by 454.67 points or 0.63% after trading in a range of 71,625.18 and 72,261.40. There were 19 stocks advancing against 11 stocks declining on the index. (Provisional)

The broader indices ended in green; the BSE Mid cap index gained 1.06%, while Small cap index was up by 1.23%. (Provisional)

The top gaining sectoral indices on the BSE were Oil & Gas up by 3.02%, IT up by 2.91%, TECK up by 2.74%, Telecom up by 2.17% and Energy was up by 2.02%, while Power down by 0.39%, Bankex down by 0.36%, Utilities down by 0.24%, FMCG down by 0.07% were the losing indices on BSE. (Provisional)

The top gainers on the Sensex were HCL Tech. up by 4.57%, TCS up by 3.94%, Maruti Suzuki up by 3.84%, Wipro up by 3.46% and Larsen & Toubro up by 2.53%. On the flip side, Power Grid down by 2.74%, Indusind Bank down by 1.64%, ITC down by 1.45%, Kotak Mahindra Bank down by 1.03% and Bajaj Finserv down by 0.90% were the top losers. (Provisional)

Meanwhile, Fitch Ratings has said that India's interim Budget presented last week pointed to a slightly faster pace of consolidation in the next two fiscal years than was previously expected, and it reinforced its commitments to raise capital investment. The targets are broadly in line with Fitch's assumptions when they affirmed India's rating at 'BBB-' with a 'Stable' outlook in January. As such, they are unlikely to lead to significant changes in the sovereign's credit profile, although this modestly reduces near-term risks to the fiscal trajectory and signals the government's commitment to its fiscal consolidation plans. The Budget is an interim one, as elections are due in April-May 2024 and the incoming government will provide further clarification of its fiscal plans once it has taken office.

The rating agency said ‘Pre-election budgets tend to contain limited policy announcements, but budget deficit targets are typically carried through to the post-election budget when the incumbent government returns to office, as we believe is likely this year’. The government's decision to lower its deficit target for the fiscal year ending March 2024 to 5.8 per cent of GDP, from 5.9 per cent, is a modest change. However, it said ‘we believe it signals a reduced risk that the process of fiscal consolidation could be set back by a pre-election spending surge. In addition, the deficit target of 5.1 per cent of GDP in FY25 would keep the government on track to reach its medium-term goal of narrowing the deficit to 4.5 per cent of GDP in FY26.’

The continued emphasis on capex investment, with a further 11 per cent spending increase, should remain supportive of the growth outlook in 2024-25, when real GDP growth is expected at 6.5 per cent. It further said ‘Strong capex should - if implemented as planned - reduce infrastructure bottlenecks and improve medium-term growth potential. We believe India is well-placed to sustain higher rates of growth in the medium term relative to many of its peers, with the capex drive helping to underpin this view.’ Fitch thinks that it will be challenging for the government to achieve its 2025-26 deficit target.

The CNX Nifty ended at 21,929.40, up by 157.70 points or 0.72% after trading in a range of 21,737.55 and 21,951.40. There were 35 stocks advancing against 15 stocks declining on the index. (Provisional)

The top gainers on Nifty were BPCL up by 6.01%, HDFC Life Insurance up by 5.22%, HCL Tech up by 4.40%, TCS up by 4.09% and Maruti Suzuki up by 3.99%. On the flip side, Power Grid down by 3.06%, Britannia down by 2.29%, Indusind Bank down by 1.72%, ITC down by 1.52% and Kotak Mahindra Bank down by 1.18% were the top losers. (Provisional)

European markets were trading mostly in green; UK’s FTSE 100 increased 29.15 points or 0.38% to 7,642.01 and France’s CAC was up by 13.42 points or 0.18% to 7,603.38. On the flip side, Germany’s DAX was down by 21.48 points or 0.13% to 16,882.58.

Asian markets ended mostly higher on Tuesday, with Chinese and Hong Kong markets surging after a government investment fund said it would expand purchases of stock index funds to counter heavy selling in the Chinese markets and a report said China’s leader Xi Jinping was set to discuss the nation's stock market with financial regulators. However, some gains were limited by concerns over heightened geopolitical tensions in the Middle East. Seoul markets fell after comments from US Fed Chair Jerome Powell and other Fed officials suggested that interest rate cuts may come later than anticipated. Japanese markets declined as investors booked profits and continued to assess domestic earnings reports. Meanwhile, Taiwan's stock market is closed from today to 14th February for the Lunar New Year holiday.

| Asian Indices | Last Trade | Change in Points | Change in % |

| Shanghai Composite | 2,789.49 | 87.30 | 3.13 |

| Hang Seng | 16,136.87 | 626.86 | 3.88 |

| Jakarta Composite | 7,247.41 | 48.79 | 0.67 |

| KLSE Composite | 1,512.98 | 1.64 | 0.11 |

| Nikkei 225 | 36,160.66 | -193.50 | -0.54 |

| Straits Times | 3,125.68 | -8.61 | -0.28 |

| KOSPI Composite | 2,576.20 | -15.11 | -0.59 |

| Taiwan Weighted | -- | -- | -- |

MoneyWorks4Me rating and ranking of funds for SIP is available to subscribers only. Moneyworks4Me is not a rating and ranking agency, however it is required that users have a way of selecting funds and building a Portfolio. The method used by it are described below to enable users to understand the logic behind the rating and ranking Subscriber will find more details on this in the various content made available from time to time. In case you need more please write to besafe@moneyworks4Me.com

MoneyWorks4Me rates and ranks mutual funds based on the following data-driven system:

Funds ranking in screeners: Performance Consistency and Quality are two parameters used for ranking funds for SIP. The ranking as follows GG, GO, GR, OG, OO, OR, RG, RO and RR.

With the same color-coded funds, the one with the higher Average 3-year rolling returns (over 5 to 10 years), the number that appears in the Performance tag, ranks higher.

Here is the summary:

The third tag Upside Potential is not relevant for SIP. It is relevant for lumpsum investments in Mutual Funds.

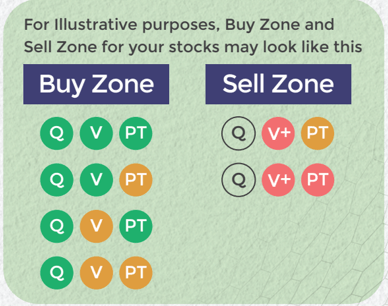

Buy quality Stocks when they are available at reasonable prices and supported by an upward price trend and Sell when they are Overvalued using the Decizen Rating System. Covers 3500+ stocks

Download APP

Download APP