Invest in the best stock opportunities right now and every-time.

Start Systematic Stock Investing ...in less than a minute.

Tracking positive cues from India’s retail inflation data, Indian benchmark indices finished the productive day of trade with gains of over half a percent. Banking sectors’ stock led the position in the markets. Despite making cautious start, key gauges soon gained traction to trade higher, as traders got support with a report that retail inflation based on Consumer Price Index (CPI) eased to a three-month low of 5.1 per cent in January 2024. Inflation was at 5.69 per cent in December 2023. It was 6.52 per cent in January 2023. Investors overlooked report that India’s industrial production growth slowed to 3.8 per cent in December 2023, mainly due to poor performance of mining and power generation segments. The factory output growth measured in terms of the Index of Industrial Production (IIP) was at 5.1 per cent in December 2022. Sentiments also got some support after a survey conducted by Federation of Indian Chambers of Commerce and Industry (FICCI) has revealed sustained and continued growth for India's manufacturing sector in the last two quarters of 2023-24 (October-March). Compared to the previous quarter, October-December, when 73 per cent of respondents had reported higher production levels, in the current January-March quarter, around 87 per cent of respondents expected either higher or the same level of production.

Despite some profit booking in noon deals, markets regained momentum and continued trading in green. Some support came in with Reserve Bank Governor Shaktikanta Das’ statement that lower government borrowings than the market estimates will free more capital for the private sector resulting in easing of inflation and bolstering growth. Markets added gains end near day’s high levels, as investors continued to hunt for fundamentally strong stocks. Meanwhile, the Periodic Labour Force Survey (PLFS) data, released by the National Statistical Office showed that the jobless rate in urban India marginally declined further in Q3 (October-December) of FY24 to 6.5 per cent from 6.6 per cent in the preceding quarter, thus reflecting continued improvement in the labour markets. Investors now turn their attention towards U.S. inflation data due later in the day.

On the global front, European markets were trading lower as investors assessed incoming corporate earnings reports and awaited a key U.S. inflation print. Asian markets ended mostly in green led by a powerful rally in Tokyo. Markets in China, Hong Kong and Taiwan remain closed for the Lunar New Year holidays. Back home, Union Minister Hardeep Singh Puri lauded the economic growth of India, citing a robust expansion of 7.6 per cent in the last three quarters. Puri highlighted the significant strides made in employment across government, public, private, and informal sectors. He expressed optimism about India's economic trajectory, referencing projections from international analysts and rating agencies forecasting India's economy to rank among the top three globally within the next five years.

Finally, the BSE Sensex rose 482.70 points or 0.68% to 71,555.19 and the CNX Nifty was up by 127.20 points or 0.59% to 21,743.25.

The BSE Sensex touched high and low of 71,662.74 and 70,924.30 respectively. There were 25 stocks advancing against 5 stocks declining on the index.

The broader indices were trading in green; the BSE Mid cap index was up by 0.61%, while Small cap index up by 0.18%.

The top gaining sectoral indices on the BSE were Bankex up by 1.44%, PSU up by 1.24%, Energy up by 1.03%, Healthcare up by 0.74% and TECK was up by 0.40%, while Metal down by 1.44%, Basic Materials down by 0.94% and Realty was down by 0.01% were the few losing indices on BSE.

The top gainers on the Sensex were ICICI Bank up by 2.46%, Axis Bank up by 2.30%, Wipro up by 2.14%, NTPC up by 1.85% and Kotak Mahindra Bank up by 1.58%. On the flip side, Ultratech Cement down by 1.03%, Mahindra & Mahindra down by 0.85%, Titan Company down by 0.60%, Tata Motors down by 0.48% and ITC down by 0.06% were the top losers.

Meanwhile, a survey conducted by Federation of Indian Chambers of Commerce and Industry (FICCI) has revealed sustained and continued growth for India's manufacturing sector in the last two quarters of 2023-24 (October-March). Compared to the previous quarter, October-December, when 73 per cent of respondents had reported higher production levels, in the current January-March quarter, around 87 per cent of respondents expected either higher or the same level of production.

Responses have been drawn from over 400 manufacturing units from both large and SME segments with a combined annual turnover of over Rs 3.4 lakh crore. This upbeat assessment of Indian manufacturing is also reflected in higher-order books. As per the survey, 85 per cent of the respondents in the current January-March quarter are expecting a higher number of orders compared to the previous quarter. Domestic demand conditions also show optimism. The existing average capacity utilization in manufacturing is around 73 per cent, which reflects sustained economic activity in the sector, which is more or less the same as reported in previous surveys.

It stated the future investment outlook also looks steady, with over 50 per cent of respondents indicating plans for investments and expansions in the next six months. On the contrary, the availability of raw materials and their escalating prices, uncertainty in global demand, shortage of skilled labour, market volatility, increased power costs, unutilized capacities, and high bank interest rates, are some of the major constraints that are affecting expansion plans of the respondents.

The CNX Nifty traded in a range of 21543.35 and 21766.80. There were 36 stocks advancing against 14 stocks declining on the index.

The top gainers on Nifty were UPL up by 4.52%, Coal India up by 4.52%, ICICI Bank up by 2.38%, Axis Bank up by 2.30% and SBI Life up by 2.20%. On the flip side, Hindalco down by 12.42%, Grasim Industries down by 3.87%, Ultratech Cement down by 1.12%, Divi's Lab down by 1.06% and BPCL down by 1.04% were the top losers.

European markets were trading lower; UK’s FTSE 100 decreased 9.5 points or 0.13% to 7,564.19, France’s CAC fell 20.72 points or 0.27% to 7,669.08 and Germany’s DAX was down by 88.35 points or 0.52% to 16,949.00.

Asian markets ended mostly higher on Tuesday ahead of January's US inflation data due out later in the day that could provide more cues on the timing of interest rate cuts in the United States. Meanwhile, the Federal Reserve Bank New York survey showed consumer expectations for 1-year and 5-year inflation growth were unchanged at 3% and 2.5% in January. Many regional markets were resumed trading after a long holiday weekend. Markets in mainland China remain closed for the Lunar New Year holiday, with trade expected to resume on February 19, Hong Kong market is due to resume trading on February 14. Japanese shares gained after data showed producer prices in the country edged up 0.2% from a year earlier in January, while remaining flat month-on-month.

| Asian Indices | Last Trade | Change in Points | Change in % |

| Shanghai Composite | -- | -- | -- |

| Hang Seng | -- | -- | -- |

| Jakarta Composite | 7,209.74 | -87.93 | -1.22 |

| KLSE Composite | 1,531.37 | 19.09 | 1.26 |

| Nikkei 225 | 37,963.97 | 1,066.55 | 2.81 |

| Straits Times | 3,141.87 | 3.57 | 0.11 |

| KOSPI Composite | 2,649.64 | 29.32 | 1.11 |

| Taiwan Weighted | -- | -- | -- |

MoneyWorks4Me rating and ranking of funds for SIP is available to subscribers only. Moneyworks4Me is not a rating and ranking agency, however it is required that users have a way of selecting funds and building a Portfolio. The method used by it are described below to enable users to understand the logic behind the rating and ranking Subscriber will find more details on this in the various content made available from time to time. In case you need more please write to besafe@moneyworks4Me.com

MoneyWorks4Me rates and ranks mutual funds based on the following data-driven system:

Funds ranking in screeners: Performance Consistency and Quality are two parameters used for ranking funds for SIP. The ranking as follows GG, GO, GR, OG, OO, OR, RG, RO and RR.

With the same color-coded funds, the one with the higher Average 3-year rolling returns (over 5 to 10 years), the number that appears in the Performance tag, ranks higher.

Here is the summary:

The third tag Upside Potential is not relevant for SIP. It is relevant for lumpsum investments in Mutual Funds.

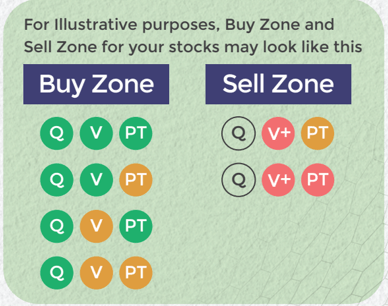

Buy quality Stocks when they are available at reasonable prices and supported by an upward price trend and Sell when they are Overvalued using the Decizen Rating System. Covers 3500+ stocks

Download APP

Download APP