Create stable, long-term investment portfolio with strong, consistent stocks.

Start Research-backed Investing ...Now.

Indian equity benchmarks gained over half a percent on Monday amid positive global cues and easing crude oil prices. Markets opened higher and sustained gains for most part of the session as traders took support with provisional data from the NSE showing that foreign institutional investors (FIIs) net bought shares worth Rs 1,659.27 crore on April 5, 2024. Traders took encouragement as a recent bi-monthly survey conducted by the Reserve Bank of India (RBI) from March 2 to March 11, 2024 showed that consumer confidence in India has soared to its highest level since mid-2019. The survey, which included 6,083 respondents, with females comprising 50.8 percent of the sample, revealed a significant uptick in consumer sentiment.

Markets added some gains in late afternoon session, taking support with a latest data by the Reserve Bank of India (RBI) showing that India’s foreign exchange reserves rose to a new high for the third straight week, reaching $645.58 billion in the week ended March 29. The total reserves rose by $2.95 billion in the previous week. Some optimism also came as India Ratings and Research (Ind-Ra) has put out a report maintaining a neutral outlook on the finances of Indian states for the fiscal year 2024-2025 (FY25), showing States' aggregate revenue deficit is projected to be 0.4 per cent of gross domestic product (GDP) for FY25, down from 0.5 per cent in FY24. The buoyancy in sentiment continued, led by sectorial tailwinds and Q4 earnings growth expectations. The Nifty, Sensex scaled fresh all-time highs in today's session but pared some of the early gains to settle around the day's highs.

On the global front, Asian markets settled mostly higher on Monday as traders reacted to US data showing much stronger than expected job growth in March that pointed to a robust economy. European markets were trading higher as Middle East tensions eased, and investors looked ahead to an ECB policy meeting and key U.S. inflation data due later this week for important clues on the interest rate path. Meanwhile, investors cheered data showing that German industrial production rose more than expected in February, helped by a recovery in the construction and car industry.

Finally, the BSE Sensex rose 494.28 points or 0.67% to 74,742.50 and the CNX Nifty was up by 152.60 points or 0.68% points to 22,666.30.

The BSE Sensex touched high and low of 74,869.30 and 74,410.07 respectively. There were 22 stocks advancing against 8 stocks declining on the index.

The broader indices ended mixed; the BSE Mid cap index rose 0.26%, while Small cap index was down by 0.06%.

The top gaining sectoral indices on the BSE were Auto up by 1.65%, Oil & Gas up by 1.51%, Energy up by 1.24%, Realty up by 1.21%, Consumer Discretionary up by 1.14%, while IT down by 0.55% and TECK down by 0.10% were the top losing indices on BSE.

The top gainers on the Sensex were Maruti Suzuki up by 3.26%, Mahindra & Mahindra up by 3.22%, NTPC up by 2.54%, JSW Steel up by 2.39% and Larsen & Toubro up by 1.92%. On the flip side, Nestle down by 1.59%, Wipro down by 1.09%, Sun Pharma down by 0.51%, HCL Technologies down by 0.37% and Titan Company down by 0.32% were the top losers.

Meanwhile, India Ratings and Research (Ind-Ra) in its latest report said that it has maintained a neutral outlook on the finances of Indian states for the fiscal year 2024-2025 (FY25), showing States’ aggregate revenue deficit is projected to be 0.4 per cent of gross domestic product (GDP) for FY25, down from 0.5 per cent in FY24. Additionally, the agency expects the aggregate fiscal deficit of all states for FY25 to decrease to 3.1 per cent of GDP, compared to the revised figure of 3.2 per cent in FY24.

The report underscores the containment of revenue deficits, which provides greater fiscal flexibility to states, enabling them to sustain focus on capital expenditure (capex) projects. Anuradha Basumatari, director of Public Finance at Ind-Ra, emphasised the favorable conditions for capital expenditure, stating, “Containment of the revenue deficit provides greater fiscal flexibility to states, which is favourable to capital expenditure and is expected to continue in FY25.”

Besides, the report analyzed the budgets of 26 states (excluding Arunachal Pradesh and Sikkim), revealing a budgeted decline of 7.4 per cent in grants from the center for FY25 compared to the revised estimate for FY24. Consequently, Ind-Ra expects revenue expenditure to grow by 8.7 per cent yoy in FY25, commensurate with the projected growth in revenue receipts.

The CNX Nifty traded in a range of 22,697.30 and 22,550.35. There were 37 stocks advancing against 13 stocks declining on the index.

The top gainers on Nifty were Eicher Motors up by 3.91%, Mahindra & Mahindra up by 3.36%, Maruti Suzuki up by 3.33%, NTPC up by 3.16% and SBI Life Insurance Company up by 2.27%. On the flip side, Adani Ports &SEZ down by 1.64%, Nestle down by 1.49%, Apollo Hospital down by 1.23%, Wipro down by 0.99% and Sun Pharma down by 0.58% were the top losers.

European markets were trading higher; UK’s FTSE 100 increased 9.40 points or 0.12% to 7,920.56, , France’s CAC rose 48.09 points or 0.6% to 8,109.4 and Germany’s DAX was up by 107.89 points or 0.59% to 18,282.93.

Asian Indices | Last Trade | Change in Points | Change in % |

Shanghai Composite | 3,047.05 | -22.25 | -0.73 |

Hang Seng | 16,732.85 | 8.93 | 0.05 |

Jakarta Composite | -- | -- | -- |

KLSE Composite | 1,559.98 | 4.73 | 0.30 |

Nikkei 225 | 39,347.04 | 354.96 | 0.90 |

Straits Times | 3,215.99 | -2.27 | -0.07 |

KOSPI Composite | 2,717.65 | 3.44 | 0.13 |

Taiwan Weighted | 20,417.70 | 80.10 | 0.39 |

MoneyWorks4Me rating and ranking of funds for SIP is available to subscribers only. Moneyworks4Me is not a rating and ranking agency, however it is required that users have a way of selecting funds and building a Portfolio. The method used by it are described below to enable users to understand the logic behind the rating and ranking Subscriber will find more details on this in the various content made available from time to time. In case you need more please write to besafe@moneyworks4Me.com

MoneyWorks4Me rates and ranks mutual funds based on the following data-driven system:

Funds ranking in screeners: Performance Consistency and Quality are two parameters used for ranking funds for SIP. The ranking as follows GG, GO, GR, OG, OO, OR, RG, RO and RR.

With the same color-coded funds, the one with the higher Average 3-year rolling returns (over 5 to 10 years), the number that appears in the Performance tag, ranks higher.

Here is the summary:

The third tag Upside Potential is not relevant for SIP. It is relevant for lumpsum investments in Mutual Funds.

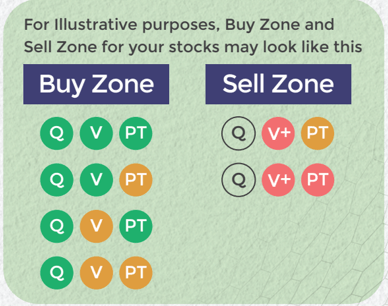

Buy quality Stocks when they are available at reasonable prices and supported by an upward price trend and Sell when they are Overvalued using the Decizen Rating System. Covers 3500+ stocks

Download APP

Download APP