Invest in the best stock opportunities right now and every-time.

Start Systematic Stock Investing ...in less than a minute.

Indian equity benchmarks showed stability till the end of the session, with Nifty and Sensex settling above the psychological 22,650 and 74,700 levels, respectively. Markets hit record highs during the day ahead of 2024 general elections. Meanwhile, traders were keenly watching out for Index of industrial production (IIP) and Consumer Price Index (CPI) data. As for broader indices, the BSE Mid cap index ended in green, while Small cap index ended in red. Buying was witnessed in Auto and Oil & Gas sectors’ stock.

Markets made positive start and extended their gains tracking positive global cues. Foreign fund inflows aided domestic sentiments. Foreign institutional investors (FIIs) net bought shares worth Rs 1,659.27 crore on April 5, provisional data from the NSE showed. Traders took encouragement as a recent bi-monthly survey conducted by the Reserve Bank of India (RBI) from March 2 to March 11, 2024 showed that consumer confidence in India has soared to its highest level since mid-2019. The survey, which included 6,083 respondents, with females comprising 50.8 percent of the sample, revealed a significant uptick in consumer sentiment. In afternoon session, indices scaled new high levels. Some support came as India Ratings and Research (Ind-Ra) has put out a report maintaining a neutral outlook on the finances of Indian states for the fiscal year 2024-2025 (FY25), showing States' aggregate revenue deficit is projected to be 0.4 per cent of gross domestic product (GDP) for FY25, down from 0.5 per cent in FY24. Markets continued to trade higher in late afternoon session as investors continued to hunt for fundamentally strong stocks. Finally, markets closed the optimistic day of trade with gains of over half a percent.

On the global front, European markets were trading higher as investors braced of key U.K. and U.S. economic releases this week for clues on the interest rate path. Asian markets ended mostly in green amid traders weighed the chances of the Federal Reserve cutting interest rates this year after a forecast-busting US jobs report dented hopes for a first move in June. Back home, Federation of Automobile Dealers Associations (FADA) has said that automobile retail sales in India saw double-digit growth in 2023-24 driven by record offtake of passenger vehicles, three- wheelers and tractors. The retail sales across segments rose by 10 per cent to 2,45,30,334 units last fiscal as compared with 2,22,41,361 units in 2022-23.

The BSE Sensex ended at 74,742.50, up by 494.28 points or 0.67% after trading in a range of 74,410.07 and 74,869.30. There were 22 stocks advancing against 8 stocks declining on the index. (Provisional)

The broader indices ended mixed; the BSE Mid cap index gained 0.26%, while Small cap index was down by 0.06%. (Provisional)

The top gaining sectoral indices on the BSE were Auto up by 1.65%, Oil & Gas up by 1.51%, Energy up by 1.24%, Realty up by 1.21% and Consumer discretionary was up by 1.14%, while IT down by 0.55% and TECK down by 0.10% were the only losing indices on BSE. (Provisional)

The top gainers on the Sensex were Maruti Suzuki up by 3.58%, Mahindra & Mahindra up by 3.42%, NTPC up by 2.71%, JSW Steel up by 2.42% and Larsen & Toubro up by 1.83%. On the flip side, Nestle down by 1.56%, Wipro down by 1.07%, Sun Pharma down by 0.59%, HCL Tech down by 0.36% and TCS down by 0.25% were the top losers. (Provisional)

Meanwhile, SBI Research, in a report, is anticipating the rate cut cycle to begin from October 2024, As the Reserve Bank of India (RBI) maintained the status quo in repo rate for the seventh time this week. The repo rate is the rate of interest at which RBI lends to other banks. Along expected lines, RBI kept the policy repo rate unchanged at 6.50 per cent, the seventh time in a row. The central bank also decided to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target of 4 per cent, while supporting economic growth.

RBI retained its inflation projection for 2024-25 at 4.5 per cent with Q1 at 4.9 per cent, Q2 at 3.8 per cent, Q3 at 4.6 per cent, and Q4 at 4.5 per cent. However, it noted that the outlook for inflation will largely be shaped by food price uncertainties (indications of a normal monsoon on one side while increasing incidence of climate shocks on other side). As per the report, ‘The good thing is however, that with 4 per cent inflation target in FY26, the RBI is possibly guiding the market with a prolonged rate cut cycle’. It argued ‘Possibly with more than a couple of rate cuts. We expect a series of rate cuts beginning October 2024, followed by another in December 2024 and possibly in February 2025. The stance change can happen in October itself’.

Coming to real GDP growth projection for 2024-25, it has been retained at 7.0 per cent (Q1: 7.1per cent, Q2: 6.9 per cent, Q3: 7.0 per cent, and Q4: 7.0 per cent) with risks evenly balanced. While agriculture may be supported by the expected normal monsoon in the best-case scenario, manufacturing is expected to maintain its momentum on the back of sustained profitability. Inflation has been a concern for many countries, including advanced economies, but India has largely managed to steer its inflation trajectory quite well. Barring the latest pauses, the RBI raised the repo rate by 250 basis points cumulatively to 6.5 per cent since May 2022 in the fight against inflation. Raising interest rates is a monetary policy instrument that typically helps suppress demand in the economy, thereby helping the inflation rate decline.

The CNX Nifty ended at 22,666.30, up by 152.60 points or 0.68% after trading in a range of 22,550.35 and 22,697.30. There were 37 stocks advancing against 13 stocks declining on the index. (Provisional)

The top gainers on Nifty were Eicher Motors up by 4.33%, Maruti Suzuki up by 3.57%, Mahindra & Mahindra up by 3.22%, NTPC up by 2.52% and JSW Steel up by 2.26%. On the flip side, Adani Ports down by 1.96%, Nestle down by 1.56%, Apollo Hospital down by 1.41%, Wipro down by 1.06% and LTIMindtree down by 0.61% were the top losers. (Provisional)

European markets were trading higher; UK’s FTSE 100 increased 6.44 points or 0.08% to 7,917.60, France’s CAC rose 42.99 points or 0.53% to 8,104.30 and Germany’s DAX was up by 105.33 points or 0.58% to 18,280.37.

Asian markets settled mostly higher on Monday as investors were awaiting speeches by Federal Reserve officials, US inflation data and the release of minutes of the Federal Reserve's March monetary policy meeting due later in the week for further cues. Market sentiments improved further as Middle East tensions eased after Israel withdrew more soldiers from parts of Gaza and committed to fresh talks over a potential ceasefire with Hamas. Japanese shares gained due to Wall Street gains backed by upbeat jobs data from the United States, while a weaker yen also lent support. Hong Kong shares gained marginally after Chief Executive John Lee Ka-chiu said the authorities were considering additional measures to bolster the securities market in the Asian financial hub, which has taken a hit from China's economic slowdown and geopolitical tensions. However, Chinese markets declined with caution ahead of key data on inflation and foreign trade due this week. Indonesian market is closed for Id-Ul-Fitr (Ramadan Eid).

| Asian Indices | Last Trade | Change in Points | Change in % |

| Shanghai Composite | 3,047.05 | -22.25 | -0.73 |

| Hang Seng | 16,732.85 | 8.93 | 0.05 |

| Jakarta Composite | -- | -- | -- |

| KLSE Composite | 1,559.98 | 4.73 | 0.30 |

| Nikkei 225 | 39,347.04 | 354.96 | 0.90 |

| Straits Times | 3,215.99 | -2.27 | -0.07 |

| KOSPI Composite | 2,717.65 | 3.44 | 0.13 |

| Taiwan Weighted | 20,417.70 | 80.10 | 0.39 |

MoneyWorks4Me rating and ranking of funds for SIP is available to subscribers only. Moneyworks4Me is not a rating and ranking agency, however it is required that users have a way of selecting funds and building a Portfolio. The method used by it are described below to enable users to understand the logic behind the rating and ranking Subscriber will find more details on this in the various content made available from time to time. In case you need more please write to besafe@moneyworks4Me.com

MoneyWorks4Me rates and ranks mutual funds based on the following data-driven system:

Funds ranking in screeners: Performance Consistency and Quality are two parameters used for ranking funds for SIP. The ranking as follows GG, GO, GR, OG, OO, OR, RG, RO and RR.

With the same color-coded funds, the one with the higher Average 3-year rolling returns (over 5 to 10 years), the number that appears in the Performance tag, ranks higher.

Here is the summary:

The third tag Upside Potential is not relevant for SIP. It is relevant for lumpsum investments in Mutual Funds.

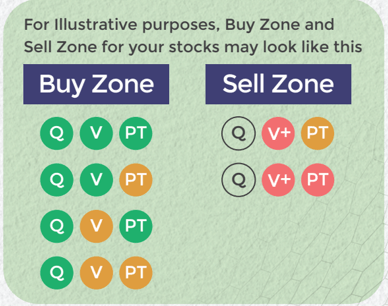

Buy quality Stocks when they are available at reasonable prices and supported by an upward price trend and Sell when they are Overvalued using the Decizen Rating System. Covers 3500+ stocks

Download APP

Download APP