Create stable, long-term investment portfolio with strong, consistent stocks.

Start Research-backed Investing ...Now.

Indian equity benchmarks erased all the intraday gains and ended in the negative zone on Tuesday, amid a fag-end sell-off in IT, TECK and Metal shares. That apart, profit booking by investors ahead of the US Federal Reserve policy meeting outcome, coupled with weekly expiry of the Bank Nifty F&O contracts dampened sentiment. Benchmark indices made a positive opening and extended gains as the day progressed as sentiments got a boost with economic think tank National Council of Applied Economic Research (NCAER) stating that the Indian economy has continued to do well in the last two months and forecast of an above-normal monsoon augurs well for the immediate future. NCAER said a range of high-frequency indicators reveal the resilience of the domestic economy with the Purchasing Managers' Index (PMI) for manufacturing at a 16-year high and UPI, the leading digital payments system, touching the highest volume since its inception in 2016. Some support also came with exchange data showing that Foreign Institutional Investors (FIIs) turned buyers on Monday after continuous offloading. They bought equities worth Rs 169.09 crore.

Sentiments remained up-beat in afternoon deals, taking support from a private report stating that India's services exports will increase to $800 billion by 2030 from $340 billion in 2023, making the external sector resilient to supply-side shocks and reducing rupee volatility. It said India's foreign trade policy announced last year targeted $1 trillion of service exports by 2030. Traders got support as the government is looking at ways to improve the competitiveness of exports amid mounting geopolitical tensions and has begun examining the export credit landscape. The commerce and industry ministry has sought details on exporters' financial needs, challenges faced in accessing export credit and the ways to improve it. However, a sharp reversal in the last hour of trade dragged the indices lower to settle the session in red. Traders turned cautious as Crisil in its report stated that India Inc is likely to log 4-6 per cent revenue growth in the January-March quarter of 2023-24, marking the slowest quarterly growth since recovery from the Covid-19 pandemic which began in September 2021.

On the global front, European markets were trading mostly in red as investors looked forward to the Federal Reserve providing an update on when interest rates might be cut. The downside remained capped as preliminary flash estimate from Eurostat showed that the euro area economy expanded in the first quarter after two consecutive declines. Gross domestic product grew by more-than-expected 0.3 percent on quarter following a 0.1 percent fall each in the fourth and third quarters of 2023. Thus, the economy recovered from a recession. Asian markets settled mostly higher on Tuesday, following the broadly positive cues from Wall Street, as traders cautiously looked ahead to the US Fed's monetary policy announcement on Wednesday after the central bank's preferred inflation gauge largely met expectations.

Finally, the BSE Sensex fell 188.50 points or 0.25% to 74,482.78 and the CNX Nifty was down by 38.55 points or 0.17% points to 22,604.85.

The BSE Sensex touched high and low of 75,111.39 and 74,346.40 respectively. There were 12 stocks advancing against 17 stocks declining, while 1 stock remained unchanged on the index.

The broader indices ended in green; the BSE Mid cap index rose 0.49%, while Small cap index was up by 0.10%.

The top gaining sectoral indices on the BSE were Auto up by 1.70%, Realty up by 1.46%, Power up by 1.04%, Consumer discretionary up by 0.93% and Utilities up by 0.80%, while IT down by 0.98%, TECK down by 0.98%, Metal down by 0.85%, Oil & Gas down by 0.85% and Basic Materials down by 0.56% were the top losing indices on BSE.

The top gainers on the Sensex were Mahindra & Mahindra up by 4.53%, Power Grid Corporation up by 2.71%, Indusind Bank up by 1.87%, Bajaj Finance up by 1.52% and Bajaj Finserv up by 1.27%. On the flip side, Tech Mahindra down by 2.08%, JSW Steel down by 1.50%, Tata Steel down by 1.46%, HCL Technologies down by 1.41% and Sun Pharma down by 1.29% were the top losers.

Meanwhile, credit rating agency Crisil in its latest report has said that India Inc is likely to log 4-6 per cent revenue growth in the January-March quarter of 2023-24 (Q4FY24), marking the slowest quarterly growth since recovery from the Covid-19 pandemic which began in September 2021. The report is based on an analysis of 350 companies which exclude financial services and oil and gas sectors firms.

According to the report, the moderation follows stronger growth in previous years. It said among the 47 sectors monitored by Crisil, only 12 are expected to have clocked an improvement in revenue growth both sequentially and on-year for the quarter. Consumer discretionary products and services are expected to have led the show in the January-March quarter. Among discretionary products, the automobiles sector was steered by healthy growth in passenger vehicles on the back of higher volumes and price hikes in the past year.

The report said the organised retail sector grew for the thirteenth quarter in a row, on healthy urban demand. Discretionary services, such as airlines and hotels benefited from MICE (meetings, incentives, conferences and exhibitions), weddings and rebound in corporate travel. On the other hand, it said revenue from construction-linked sectors is expected to have grown at a tepid pace, essentially on account of a high base of the fourth quarter of fiscal 2023 that saw construction companies achieving their highest quarterly revenue. It further said that the cement sector, despite steady demand momentum during the quarter, recorded moderate revenue growth as prices remained under pressure amid higher supply and intense competition.

The CNX Nifty traded in a range of 22,783.35 and 22,568.40. There were 24 stocks advancing against 25 stocks declining, while 1 stock remained unchanged on the index.

The top gainers on Nifty were Mahindra & Mahindra up by 4.57%, Power Grid Corporation up by 2.77%, Shriram Finance up by 2.12%, Hero MotoCorp up by 2.09% and Bajaj Auto up by 1.78%. On the flip side, Tech Mahindra down by 2.00%, Tata Steel down by 1.58%, Dr. Reddy's Lab down by 1.54%, Sun Pharmaceutical Industries down by 1.51% and HCL Technologies down by 1.44% were the top losers.

European markets were trading mostly in red; France’s CAC fell 11.28 points or 0.14% to 8,053.87 and Germany’s DAX lost 59.66 points or 0.33% to 18,058.66, while UK’s FTSE 100 increased 41.55 points or 0.51% to 8,188.58.

Asian markets settled mostly higher on Tuesday, with the weakness in gold, crude oil, strong corporate earnings report and on optimism over more stimulus measures in mainland China followed by mixed PMI data. Japan's Nikkei advanced to its two-week high level followed by robust industrial production growth. While, investors also digested muted unemployment data and slower than expected retail sales growth. Market also closely monitored currency moves amid reports on intervention of Japanese authorities to support the yen as it tumbled to 160 per dollar.

Indian equity benchmarks erased all the intraday gains and ended in the negative zone on Tuesday, amid a fag-end sell-off in IT, TECK and Metal shares. That apart, profit booking by investors ahead of the US Federal Reserve policy meeting outcome, coupled with weekly expiry of the Bank Nifty F&O contracts dampened sentiment. Benchmark indices made a positive opening and extended gains as the day progressed as sentiments got a boost with economic think tank National Council of Applied Economic Research (NCAER) stating that the Indian economy has continued to do well in the last two months and forecast of an above-normal monsoon augurs well for the immediate future. NCAER said a range of high-frequency indicators reveal the resilience of the domestic economy with the Purchasing Managers' Index (PMI) for manufacturing at a 16-year high and UPI, the leading digital payments system, touching the highest volume since its inception in 2016. Some support also came with exchange data showing that Foreign Institutional Investors (FIIs) turned buyers on Monday after continuous offloading. They bought equities worth Rs 169.09 crore.

Sentiments remained up-beat in afternoon deals, taking support from a private report stating that India's services exports will increase to $800 billion by 2030 from $340 billion in 2023, making the external sector resilient to supply-side shocks and reducing rupee volatility. It said India's foreign trade policy announced last year targeted $1 trillion of service exports by 2030. Traders got support as the government is looking at ways to improve the competitiveness of exports amid mounting geopolitical tensions and has begun examining the export credit landscape. The commerce and industry ministry has sought details on exporters' financial needs, challenges faced in accessing export credit and the ways to improve it. However, a sharp reversal in the last hour of trade dragged the indices lower to settle the session in red. Traders turned cautious as Crisil in its report stated that India Inc is likely to log 4-6 per cent revenue growth in the January-March quarter of 2023-24, marking the slowest quarterly growth since recovery from the Covid-19 pandemic which began in September 2021.

On the global front, European markets were trading mostly in red as investors looked forward to the Federal Reserve providing an update on when interest rates might be cut. The downside remained capped as preliminary flash estimate from Eurostat showed that the euro area economy expanded in the first quarter after two consecutive declines. Gross domestic product grew by more-than-expected 0.3 percent on quarter following a 0.1 percent fall each in the fourth and third quarters of 2023. Thus, the economy recovered from a recession. Asian markets settled mostly higher on Tuesday, following the broadly positive cues from Wall Street, as traders cautiously looked ahead to the US Fed's monetary policy announcement on Wednesday after the central bank's preferred inflation gauge largely met expectations.

Finally, the BSE Sensex fell 188.50 points or 0.25% to 74,482.78 and the CNX Nifty was down by 38.55 points or 0.17% points to 22,604.85.

The BSE Sensex touched high and low of 75,111.39 and 74,346.40 respectively. There were 12 stocks advancing against 17 stocks declining, while 1 stock remained unchanged on the index.

The broader indices ended in green; the BSE Mid cap index rose 0.49%, while Small cap index was up by 0.10%.

The top gaining sectoral indices on the BSE were Auto up by 1.70%, Realty up by 1.46%, Power up by 1.04%, Consumer discretionary up by 0.93% and Utilities up by 0.80%, while IT down by 0.98%, TECK down by 0.98%, Metal down by 0.85%, Oil & Gas down by 0.85% and Basic Materials down by 0.56% were the top losing indices on BSE.

The top gainers on the Sensex were Mahindra & Mahindra up by 4.53%, Power Grid Corporation up by 2.71%, Indusind Bank up by 1.87%, Bajaj Finance up by 1.52% and Bajaj Finserv up by 1.27%. On the flip side, Tech Mahindra down by 2.08%, JSW Steel down by 1.50%, Tata Steel down by 1.46%, HCL Technologies down by 1.41% and Sun Pharma down by 1.29% were the top losers.

Meanwhile, credit rating agency Crisil in its latest report has said that India Inc is likely to log 4-6 per cent revenue growth in the January-March quarter of 2023-24 (Q4FY24), marking the slowest quarterly growth since recovery from the Covid-19 pandemic which began in September 2021. The report is based on an analysis of 350 companies which exclude financial services and oil and gas sectors firms.

According to the report, the moderation follows stronger growth in previous years. It said among the 47 sectors monitored by Crisil, only 12 are expected to have clocked an improvement in revenue growth both sequentially and on-year for the quarter. Consumer discretionary products and services are expected to have led the show in the January-March quarter. Among discretionary products, the automobiles sector was steered by healthy growth in passenger vehicles on the back of higher volumes and price hikes in the past year.

The report said the organised retail sector grew for the thirteenth quarter in a row, on healthy urban demand. Discretionary services, such as airlines and hotels benefited from MICE (meetings, incentives, conferences and exhibitions), weddings and rebound in corporate travel. On the other hand, it said revenue from construction-linked sectors is expected to have grown at a tepid pace, essentially on account of a high base of the fourth quarter of fiscal 2023 that saw construction companies achieving their highest quarterly revenue. It further said that the cement sector, despite steady demand momentum during the quarter, recorded moderate revenue growth as prices remained under pressure amid higher supply and intense competition.

The CNX Nifty traded in a range of 22,783.35 and 22,568.40. There were 24 stocks advancing against 25 stocks declining, while 1 stock remained unchanged on the index.

The top gainers on Nifty were Mahindra & Mahindra up by 4.57%, Power Grid Corporation up by 2.77%, Shriram Finance up by 2.12%, Hero MotoCorp up by 2.09% and Bajaj Auto up by 1.78%. On the flip side, Tech Mahindra down by 2.00%, Tata Steel down by 1.58%, Dr. Reddy's Lab down by 1.54%, Sun Pharmaceutical Industries down by 1.51% and HCL Technologies down by 1.44% were the top losers.

European markets were trading mostly in red; France’s CAC fell 11.28 points or 0.14% to 8,053.87 and Germany’s DAX lost 59.66 points or 0.33% to 18,058.66, while UK’s FTSE 100 increased 41.55 points or 0.51% to 8,188.58.

Asian markets settled mostly higher on Tuesday, with the weakness in gold, crude oil, strong corporate earnings report and on optimism over more stimulus measures in mainland China followed by mixed PMI data. Japan's Nikkei advanced to its two-week high level followed by robust industrial production growth. While, investors also digested muted unemployment data and slower than expected retail sales growth. Market also closely monitored currency moves amid reports on intervention of Japanese authorities to support the yen as it tumbled to 160 per dollar.

Asian Indices | Last Trade | Change in Points | Change in % |

Shanghai Composite | 3,104.82 | -8.22 | -0.26 |

Hang Seng | 17,763.03 | 16.12 | 0.09 |

Jakarta Composite | 7,234.20 | 78.42 | 1.08 |

KLSE Composite | 1,575.97 | -6.69 | -0.42 |

Nikkei 225 | 38,405.66 | 470.90 | 1.23 |

Straits Times | 3,292.69 | 10.64 | 0.32 |

KOSPI Composite | 2,692.06 | 4.62 | 0.17 |

Taiwan Weighted | 20,396.60 | -98.92 | -0.48 |

MoneyWorks4Me rating and ranking of funds for SIP is available to subscribers only. Moneyworks4Me is not a rating and ranking agency, however it is required that users have a way of selecting funds and building a Portfolio. The method used by it are described below to enable users to understand the logic behind the rating and ranking Subscriber will find more details on this in the various content made available from time to time. In case you need more please write to besafe@moneyworks4Me.com

MoneyWorks4Me rates and ranks mutual funds based on the following data-driven system:

Funds ranking in screeners: Performance Consistency and Quality are two parameters used for ranking funds for SIP. The ranking as follows GG, GO, GR, OG, OO, OR, RG, RO and RR.

With the same color-coded funds, the one with the higher Average 3-year rolling returns (over 5 to 10 years), the number that appears in the Performance tag, ranks higher.

Here is the summary:

The third tag Upside Potential is not relevant for SIP. It is relevant for lumpsum investments in Mutual Funds.

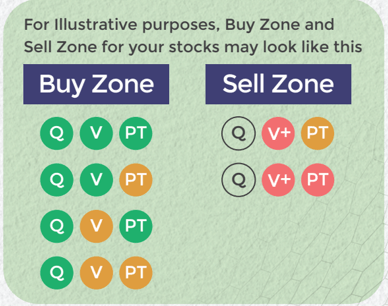

Buy quality Stocks when they are available at reasonable prices and supported by an upward price trend and Sell when they are Overvalued using the Decizen Rating System. Covers 3500+ stocks

Download APP

Download APP