Create stable, long-term investment portfolio with strong, consistent stocks.

Start Research-backed Investing ...Now.

Indian equity markets ended last trading day of week with cut of over half a percent, as traders avoided to take risk ahead of key macroeconomic data due in next week. After making positive start, indices spent their entire day in red. As for broader indices, the BSE Mid cap index and Small cap index ended in red.

Markets made positive start tracking gains across global markets as traders pulled forward expectations for the Federal Reserve's first interest-rate cut by a month to November. Some support also came in as the Organisation for Economic Co-operation and Development (OECD) raised its growth forecast for India by 40 basis points to 6.6 per cent for 2024-25, holding that buoyant public investment and improved business confidence are expected to propel India’s gross domestic product (GDP) growth. However, indices failed to hold their gains and entered into red territory, as traders turned cautious with Reserve Bank data showing that India's services exports declined 1.3 per cent in March to $30 billion while imports fell by 2.1 per cent to $16.61 billion. As per RBI's data on India's international trade in services, the trade surplus during March 2024 was $13.4 billion. Meanwhile, economic think tank GTRI in its report said India's imports of electronics, telecom, and electrical products soared to $89.8 billion in 2023-24 and over half of these imports are sourced from China and Hong Kong. Further, in afternoon session, markets continued their free fall, as traders preferred to sell their riskier assets. Traders overlooked a private report stating that the stock market reflects India's ascendance as an economic superpower with premium valuations, but challenges remain for inclusive growth. Markets remained lower till the end of the session with Nifty and Sensex settling below the psychological 22,500 and 73,900 levels, respectively.

On the global front, European markets were trading higher after a closely watched survey showed the British economy is ‘pulling further out of last year's shallow recession’ as the dominant services sector grew at its fastest pace in nearly a year. Asian markets ended mostly in green with tech shares leading the charge following Apple's quarterly earnings beat and massive buyback program. Back home, Credit rating agency, India Ratings and Research (Ind-Ra) in its latest report has maintained a neutral outlook on the construction sector for FY25, while maintaining a deteriorating sub-sector outlook for roads engineering, procurement and construction (EPC).

The BSE Sensex ended at 73,878.15, down by 732.96 points or 0.98% after trading in a range of 73,467.73 and 75,095.18. There were 6 stocks advancing against 24 stocks declining on the index. (Provisional)

The broader indices ended in red; the BSE Mid cap index declined 0.21%, while Small cap index was down by 0.55%. (Provisional)

The top gaining sectoral indices on the BSE were Metal up by 0.81%, Healthcare up by 0.15% and PSU was up by 0.12%, while Telecom down by 1.42%, Capital Goods down by 1.18%, Realty down by 1.09%, TECK down by 0.96% and Oil & Gas was down by 0.80% were the top losing indices on BSE. (Provisional)

The top gainers on the Sensex were Bajaj Finance up by 0.75%, Bajaj Finserv up by 0.69%, Mahindra & Mahindra up by 0.21%, ICICI Bank up by 0.18% and SBI up by 0.18%. On the flip side, Larsen & Toubro down by 2.74%, Maruti Suzuki down by 2.37%, Nestle down by 2.22%, Reliance Industries down by 2.17% and Bharti Airtel down by 2.03% were the top losers. (Provisional)

Meanwhile, the Organisation for Economic Co-operation and Development (OECD) in its latest Economic Outlook report has projected India’s Gross Domestic Product (GDP) to grow at 7.8 per cent in the just-concluded financial year 2023-24 and the forecast is for around 6.6 per cent in each of the following two fiscal years (FY25 and FY26). However, global near-term developments pose obstacles to higher growth. It has said India’s domestic demand will be driven by gross capital formation, particularly in the public sector, with private consumption growth remaining sluggish. OECD is a group of 37 member countries that discuss and develop economic and social policy.

In the report, OECD asserted that exports will continue to grow, especially of services such as information technology and consulting where India will continue to increase its global market share, supported by foreign investment. It added headline inflation will decline gradually, although uncertainty about food inflation remains elevated. In India, consumer price index (CPI) inflation was 4.9 per cent in March after averaging 5.1 per cent in the preceding two months, following the recent peak of 5.7 per cent in December 2023.

Retail inflation in India is in RBI’s two-six per cent comfort level but is above the ideal 4 per cent scenario. Inflation has been a concern for many countries, including advanced economies, but India has largely managed to steer its inflation trajectory quite well. The Indian central bank’s monetary policy, the OECD report said that the monetary policy easing is projected to start in the second half of the year once lower inflation is maintained.

The report said ‘Assuming a normal monsoon season and no other supply shocks that may de-anchor inflation expectations, a first cut of the policy rate is projected in late 2024, with cumulative cuts of up to 125 basis points implemented before March 2026. The RBI will only switch the stance to neutral during 2025’. Further, the report suggested that India needs to achieve a higher level of real GDP growth to address the country’s multiple development challenges, especially job creation.

The CNX Nifty ended at 22,475.85, down by 172.35 points or 0.76% after trading in a range of 22,348.05 and 22,794.70. There were 15 stocks advancing against 35 stocks declining on the index. (Provisional)

The top gainers on Nifty were Coal India up by 4.56%, Grasim Industries up by 1.81%, ONGC up by 1.17%, Dr. Reddy's Lab up by 0.99% and Hindalco up by 0.88%. On the flip side, Larsen & Toubro down by 2.77%, Maruti Suzuki down by 2.45%, Nestle down by 2.24%, Reliance Industries down by 2.22% and Bharti Airtel down by 2.04% were the top losers. (Provisional)

European markets were trading higher; UK’s FTSE 100 increased 34.42 points or 0.42% to 8,206.57, France’s CAC rose 50.25 points or 0.63% to 7,964.90 and Germany’s DAX was up by 89.34 points or 0.5% to 17,985.84.

Asian markets settled mostly higher on Friday, tracking Wall Street gains overnight with tech shares leading the charge following Apple's quarterly earnings beat and massive buyback program. Meanwhile, traders pulled forward expectations for the Federal Reserve’s first full interest-rate cut by a month to November ahead of a key US jobs data report later in the day. Hang Seng shares gained on improved market sentiments as China stepped up efforts to boost the economy. But regional trading volumes were thin due to market holidays in China and Japan.

| Asian Indices | Last Trade | Change in Points | Change in % |

| Shanghai Composite | -- | -- | -- |

| Hang Seng | 18,475.92 | 268.79 | 1.45 |

| Jakarta Composite | 7,134.72 | 17.29 | 0.24 |

| KLSE Composite | 1,589.59 | 9.29 | 0.59 |

| Nikkei 225 | -- | -- | -- |

| Straits Times | 3,292.93 | -3.96 | -0.12 |

| KOSPI Composite | 2,676.63 | -7.02 | -0.26 |

| Taiwan Weighted | 20,330.32 | 107.88 | 0.53 |

MoneyWorks4Me rating and ranking of funds for SIP is available to subscribers only. Moneyworks4Me is not a rating and ranking agency, however it is required that users have a way of selecting funds and building a Portfolio. The method used by it are described below to enable users to understand the logic behind the rating and ranking Subscriber will find more details on this in the various content made available from time to time. In case you need more please write to besafe@moneyworks4Me.com

MoneyWorks4Me rates and ranks mutual funds based on the following data-driven system:

Funds ranking in screeners: Performance Consistency and Quality are two parameters used for ranking funds for SIP. The ranking as follows GG, GO, GR, OG, OO, OR, RG, RO and RR.

With the same color-coded funds, the one with the higher Average 3-year rolling returns (over 5 to 10 years), the number that appears in the Performance tag, ranks higher.

Here is the summary:

The third tag Upside Potential is not relevant for SIP. It is relevant for lumpsum investments in Mutual Funds.

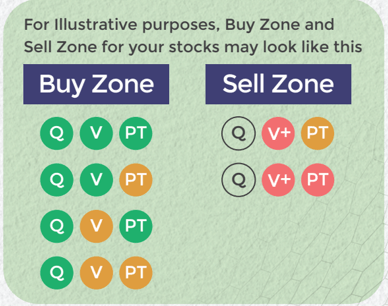

Buy quality Stocks when they are available at reasonable prices and supported by an upward price trend and Sell when they are Overvalued using the Decizen Rating System. Covers 3500+ stocks

Download APP

Download APP