This article covers the following:

Review

Nifty Total Return Index (Nifty including dividends) earned ~12% Year to date Nov’19 and ~15% CAGR in the last 3 years from demonetization lows.

Nifty continues to remain steady thanks to a handful of stocks making all-time highs while the rest of the market is at 52-week lows or even 3-year lows. This has led to underperformance for most advisors and MFs.

Overall the sentiment remained negative due to no uptick from festive demand. The economy remains sluggish due to credit squeeze, lack of employment growth and no increase in demand.

Outlook

As on date, the average upside of our coverage universe is likely to be less than 10% CAGR over the next 3 years. Given quality companies are trading at steep price multiples & our coverage mostly has quality companies, expensive valuation is getting reflected in average upside potential too.

Just a handful of companies are delivering moderate earning growth due to slow economic growth. These companies are enjoying high valuation as more and more investors are chasing them.

4 out of 5 stocks reported below 10% growth and but arrested operating profit as raw material costs were favorable in general.

Some pockets of the market like consumer staples, consumer discretionary and now insurance and AMCs are trading at stretched valuation.

As consumption acts like defensive, it is natural that consumer stocks were sought over economically sensitive stocks. Temporary problems in NBFCs and smaller private banks led to money chasing insurance and AMC.

We expect below-average returns from these baskets over the next 3 years even if earnings growth is good. Starting valuation plays an important role in long term returns.

Barring a few, auto companies may have run ahead of their valuation due to positive sentiments from festive period sales.

We will be reducing exposure to stocks that are not showing signs of improvement in the near term due to economy slowdown or company-specific issues.

Even if the overall market doesn’t look cheap, we don’t mind buying stocks with low valuation and good future prospects.

We are looking at companies that have good earning triggers over the next 2 years as we are not certain whether broad-based recovery will happen immediately.

Incrementally we are deploying funds in companies that have individual stories rather than economy sensitive.

We are investing in companies i) coming out of sector consolidation, or ii) introducing new products, or iii) commissioning new capacities or iv) executing the order in hand.

These can help us sail through the current environment and generate above-average returns.

An investor can consider investing in value and high dividend yield stocks like Infra & Infra-related companies like capital goods, high-quality PSUs, corporate banks, pharmaceuticals, and select NBFCs.

Incrementally consider investing in stocks that show promise of better growth over the medium term from company-specific triggers discussed above.

We have included stocks meeting the above criteria with Green Flag in our “Stocks in Buy Zone”.

We are also evaluating ‘Credit Risk funds’ as they might have become cheap, due to herd’s negativity, even after considering the risks they carry.

If we find any merit, we will share our recommendations and analysis with our subscribers. Maybe the aggressive risk profile investors would be interested.

We are still working on it, and not in hurry to board the bus as they won’t be moving up in a hurry. We will be waiting for better liquidity conditions before jumping into Credit Risk funds.

Few advisors are recommending small and mid-cap companies as they have seen a free fall in stock prices. However, we believe that small and mid-cap are not cheap yet to make risk-adjusted returns over an entire cycle.

Growth in small-cap stocks is poorer than large-cap stocks as they can’t wither the storm.

The price fall doesn’t indicate anything about valuation. As of now, less than 33% of small and mid-cap companies have reported more than 10% net sales growth.

Even if they rise from here, long term returns won’t be commensurate for the risk one takes investing in small and mid-cap companies today.

A SIP product may work in such a situation but we recommend caution on lump-sum purchases till we don’t see broad-based earnings recovery in mid and small-cap companies.

Risks

India

GDP Slowdown

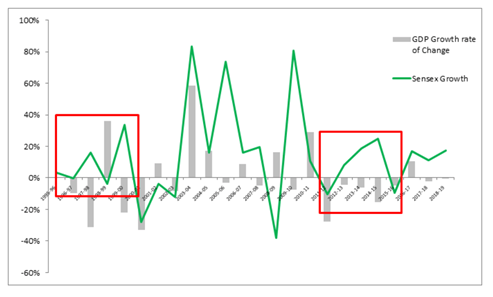

GDP growth averaged around 4.75% in the first half of FY20. This was the lowest in almost 8 years. One will also notice that the slowdown is entrenched from large size purchases to small ticket items.

Private investment grew at only 1 percent. Nominal GDP growth fell to a new low of 6.1 percent. As we know that equity returns have strong co-relation to the nominal GDP growth rate, the equity market has been underperforming.

Usually, slowdown stays for 2-4 quarters after which the low base effect kicks in thereby leading to above-average growth and sentiment improvement. So it is a wait and watches mode to see how it pans out.

We expect sectors like Agri, rural-based economy and small ticket goods companies to show the first signs of revival. These are the purchases that won’t be postponed for long.

Only post that we would see some growth recovery in companies selling large items. Housing, cars and commercial vehicles will have a lag effect.

Out of the four critical components of GDP growth i) consumption ii) private & housing capital investment iii) exports and iv) government capital investment. If we observe recent data, all the four pockets have slowed synchronously.

Prior to 2019, consumption and government capital investment were growing but that too have slowed down substantially due to i) liquidity issues in the financial system, ii) government’s control on expenditures to meet fiscal deficit target and iii) drop in state government’s revenue from the slow growth of past few years.

Government’s role

There are some obvious bottlenecks like existing capacities in bankruptcy court, real estate starved of capital even for viable projects, etc that have affected normal business sentiment.

Besides, delay in the release of payments from government organizations and tax disputes with tax authorities are causing a strain on businessmen. If these issues get relief temporarily, the dwindling sentiment can be arrested.

To set India on a growth trajectory in the future, the government needs to take large structural measures.

Source: MoneyWorks4me analyst team

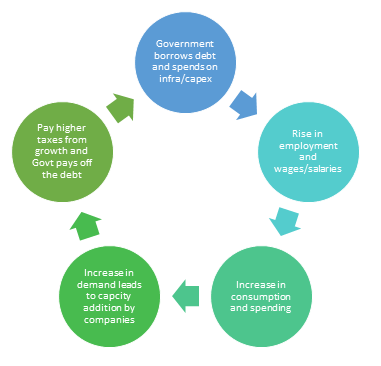

The consensus expects the government to increase its borrowing (/breach it fiscal deficit target) and use the proceeds to i) spend heavily on infrastructure, ii) lend to low return but productive projects and iii) bring down personal income taxes.

This would lead to a rise in salaries/wages and a rise in employment. The intention is to increase spending power and ultimately pick up in consumption like cars/housing/renovation.

Rising demand would encourage the companies to expand their capacities and they would see a rise in sales/employment. This will start an economic cycle that will become self-sustaining.

The government can again get back its funds via taxes/GST on increased sales and profitability of corporates.

Hon. FM Nirmala Sitaraman announced cuts in corporate tax to lure corporates to invest in new capacities. But with so much existing capacity in bankruptcy court with hardly any demand, this incentive is not sufficient to kick off the animal spirits.

Recent announcements indicate that developed market companies are likely to make investments (also called, Foreign direct investment FDI) with the government’s assurance of good infrastructure facility, lower tax rate, and easy financing.

This could help to boost employment, however, the quantum of the same is unknown.

The government is proactively fixing some of the bottlenecks that led to a drop in business and consumer sentiments like release of payments, real estate slowdown and NBFC crisis; however, the timeline of the resolution is uncertain.

Some customers did ask us, “shall we redeem our funds from the market and wait for a better price”. Very valid question but isn’t this question obviously asked by everyone?

If we see share price data from 2018, more than 80% of the stocks are at least 25% below their peak price. This has already factored in a slowdown.

If the slowdown is severe and extended there could be more drop but no so much in stocks that have already fallen.

We have written in our previous blog that how GDP and the stock markets do not move in sync. Often market return leads or lags GDP movement.

We can’t time either GDP growth trajectory nor can we time the markets. We can wait for stocks to get cheaper but once they are cheaper we find no sense in avoiding stocks just to save ourselves from the temporary drop (10-20%) in value.

Equity is meant to be volatile, we can’t expect linear returns whatsoever.

Opportunity for long term investors

Markets may remain subdued until the time earnings growth kick in. But this doesn’t mean stocks won’t rise. Those that are underpriced can rebound even of expectation that the worst scenario is behind us.

We are seeing a lot of NBFCs and banks recovering as the government’s push to resolve the liquidity crisis has brought some hope.

Near term uncertainty in structural growth, story spells an opportunity for long term investors. Stocks are beaten down from short term fears.

We do not find any merit in second-guessing what’s going to happen in the next 6months-1year. We leave this field open for speculators, fear mongers, and punters.

We also recommended sticking to one style of investing and not hop one style to another just because is it not working temporarily.

We are getting persistent queries on richly valued consumer stocks, we recommend to avoid this pocket and focus on reasonably valued companies.

We are managing only long term money and predicting near term events is futile. Asset allocation has taken care of several such uncertainties like we have gold almost 5% in our client’s portfolio which has performed well thereby protecting the downside.

Beyond this, tinkering asset allocation will only reduce long term returns thereby missing one’s target corpus. Equity returns often give surprises, we wish to stay invested to enjoy such surprises.

MoneyWorks4me Outlook:

If you liked what you read and would like to put it in to practice Register at MoneyWorks4me.com. You will get amazing FREE features that will enable you to invest in Stocks and Mutual Funds the right way.

![]()

Need help on Investing? And more….Puchho Befikar

Kyunki yeh paise ka mamala hai

Start Chat | Request a Callback | Call 020 6725 8333 | WhatsApp 8055769463