This article covers the following:

Review

For the year ending Jan’21, Nifty closed at 13,634, around 14% higher over last year. In the last 3 years, Nifty is up 23% translating into ~7% CAGR.

Out of the total 14% return last 1 year, 10% came from just four stocks HDFC Bank (1.43%), Infosys (3.43%), Reliance Ind (2.81%), and TCS (2.2%).

Low-interest rates globally and optimism around vaccines have led to new highs for Nifty. The recent rally is led by cyclical stocks that were beaten down due to uncertainty about economic recovery. Incremental macro data suggests an improvement in economic activity and better utilization. Unabated FII inflows into the emerging markets are leading to new highs for Nifty. Pro expansionary Budget announced on Feb 1, 2021, further lead to a rally in the cyclical and infrastructure sector as they could benefit from the government’s focus on investments.

Stocks that benefitted from the Covid crisis may cool off but individual stocks that report good results will continue to perform well in lines with earnings. We find broader sectors to start doing well as they report recovery from lows. There is another scenario where economic recovery may extend to earnings growth in a more sustained manner in select sectors.

After inflows of Rs. 45,000 Cr in Dec’20, FII bought additional Rs. 19,500 Cr worth of stocks in January’21, Like we shared in our blog circulated internally, FII buying or selling doesn’t provide any hint on future market direction.

Outlook

As of date, the average upside of our coverage universe is likely to be less than 10% CAGR over the next 3 years basis based on current estimates. The Valuation of companies goes up every quarter if the company reports growth in earnings. This can improve the upside potential of stocks. If we see growth improving next year, we may see an upward revision in our estimates. We have made upward revisions in sectors where we are seeing a sustained recovery in earnings and cash flows.

Nifty 50 index trades above its fair value while there are pockets of extreme overvaluation and undervaluation. A lot of liquidity helped beaten-down stocks to rally however, the economic indicator does not show full recovery in all sectors.

We are looking at opportunities in infrastructure, building materials, export-oriented chemicals, PSUs and import substitute ideas. We have incrementally added stocks in capital goods and Infrastructure as we started seeing sustained growth versus volatile growth earlier.

We look at companies that have good earning triggers over the next 2 years as we are not certain whether broad-based recovery will happen immediately. We are investing in companies i) coming out of sector consolidation/debt reduction, or ii) introducing new products, or iii) commissioning new capacities, or iv) executing orders in hand. This gives certainty of growth rather than plain anticipation or, v) Export-oriented companies as economic recovery is better in western countries.

Many stocks with poor earnings temporarily have also rallied quite sharply. This might be in anticipation of recovery over the next 2 quarters. FII inflows have led to aggressive price recovery in banks and cyclical. Current prices in quite a few names already reflect high growth thereby increasing downside risks.

Register FREE | Schedule a DEMO | Solution Enquiry | Themes | Subscribe

Risks

Indian Economy

GDP data saw two-quarters of year-on-year decline, while the recent quarter was more reasonable 7.5% versus the previous quarter decline of 23%. Fortunately, the cases have subsided and fear of the second wave is receding.

Auto sales are robust in pockets, however, vehicle registration has fallen in Jan’21. Also, disruption in semiconductor shortage may affect Auto sales which don’t reflect any insight into economic recovery.

There is good demand for cement and steel and power. Electricity consumption has been consistently growing since Oct’20 and last month was also higher than the previous year indicating pick-up industrial activity.

Rising oil prices are a risk as oil-producing countries are cutting supply leading to price rises. Fiscal Deficit in FY21 and FY22 is likely to be elevated versus long-term range which can lead to a sharp rise in bond yield affecting equity and bond prices. Inflation from rising commodity and oil prices can spark fear in economic recovery. However, without job/income growth and under-utilized capacities in the various sectors make the fears of inflation transitionary in nature for now.

Global Economy

Western countries are more vulnerable to a second wave of Covid-19 as their aging population can lead to higher fatalities. This has led to aggressive lockdown measures in countries like Germany, the UK, and some states of the US. This can slow down economic recovery.

Central banks have been keeping liquidity high which has lowered the interest rate for government bonds and corporate bonds. Savings are finding their way into higher-yielding assets like stocks, emerging markets debt, and equity.

The low-interest-rate may continue till the time economy doesn’t come back to pre-covid levels. Offlate there are signs of speculative fervor in US markets and Cryptocurrencies. A lot of trading activity has led to increasing in leverage and higher trading volume. There is a risk of synchronous global market correction at some point.

Is the market rally overdone, are we up for deep correction?

We think that compared to the US, Indian markets haven’t done much over the last 5 years to fear prolonged correction. India has been in downcycle for the last 5-8 years and it is still has below-average corporate profits to GDP. This means that even if the Indian market will correct with global markets, all markets move together in short term, there are higher chances Indian markets will recover faster. Besides, Govt pro-business outlook has further put a floor to valuation.

“Be fearful when others are greedy and be greedy when others are fearful.” We have seen quite a few Indian investors very fearful during the rally from lows. This is the nature of the market to rise and fall in quick succession. We advise looking at long term returns of the market to see whether we are in bubble territory. Given our last 5 years or 10 years, returns are similar versus average long term returns (12-13% CAGR), we do not seem to be in bubble territory. This reduces the risk of very poor returns from the current price.

In our November 2020 outlook, we recommended holding on to stocks because we don’t know whether we are amidst the 2003-04 or 2007 market rally.

In 2003-04 past 5-7 years, returns were low, valuations of economy sensitive stocks were low. In 2007-08, valuations were high, past 5/10 years’ returns were spectacular. So the risks were higher. We find that with an expansionary budget outlook, current market positioning resembles 2003 more than 2007.

We have generated good returns, how to protect them?

MoneyWorks4me portfolio has earned 28% in the calendar year 2020 versus Nifty’s 15%. For the last 3 years, most advisors and Mutual Fund portfolios lagged Nifty as the rally was concentrated in just 5-10 stocks. Out of the total 23% return of Nifty in last 3 years, HDFC Bank, Reliance, Infosys, TCS, HDFC Ltd, ICICI Bank, and Kotak Mah Bank (HRITIK) just six stocks together delivered 25% returns. This means the overall market was flat or negative for the last 3 years. In this year, broad-based rally across sector and market cap helped us win back our performance.

In long term (5 years+), or even medium-term (3 years), stock prices go up in lines with earning growth and company quality. Even if there is volatility in the interim, the stock prices of good companies recover to match respective earning growth. This is the reason we suggest focusing on the larger picture rather than interim events. If our companies are delivering earning growth, they will come back from interim corrections. We can’t time them as we risk missing out on big gains.

Odds are highly in favour of staying invested rather than exiting or delaying fresh addition.

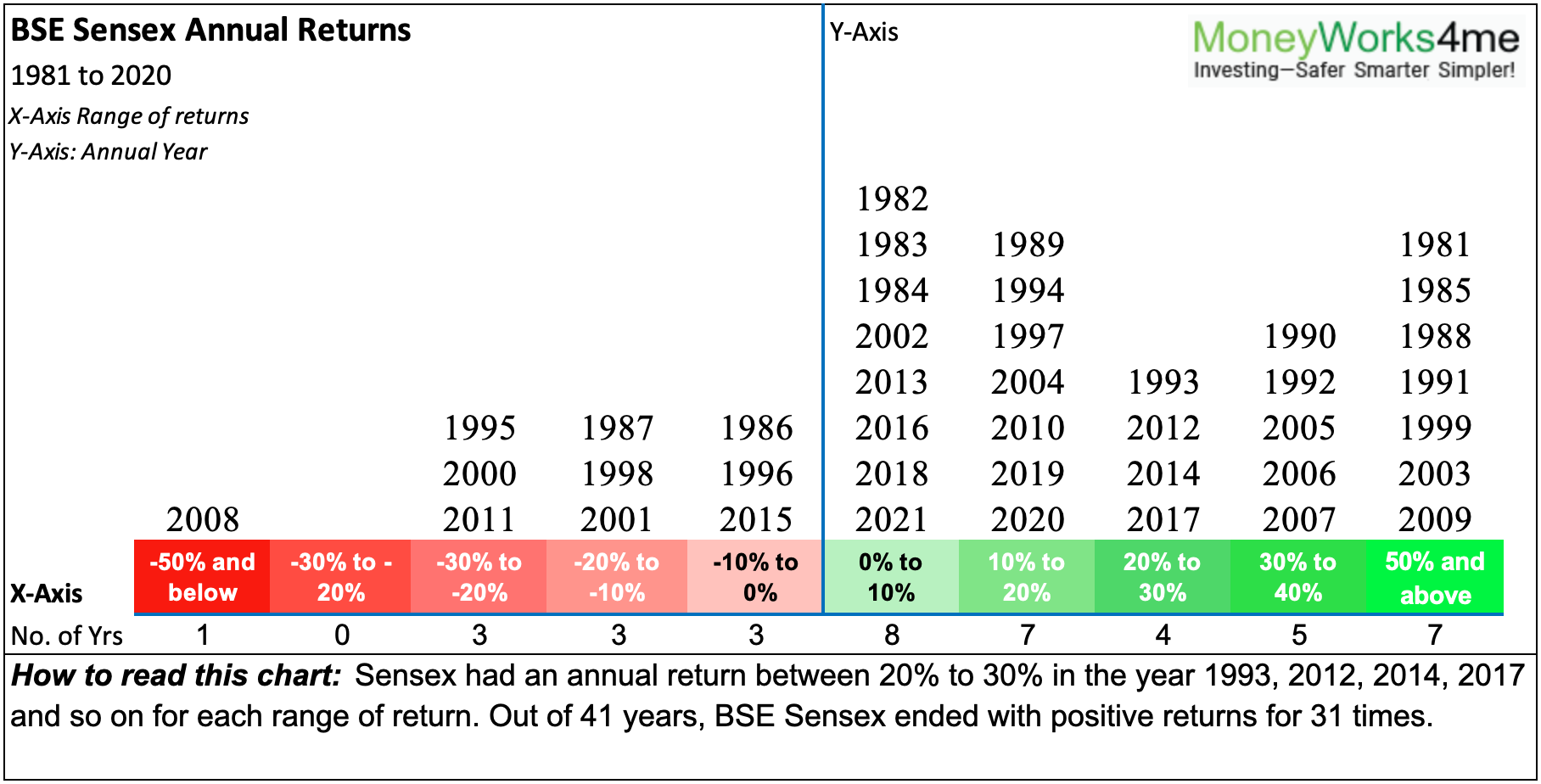

We would advise tracking returns on a longer timeframe like every year rather than every month or every quarter. For 31 out of 41 years, equity has delivered positive returns. Every bad year was followed by at least one very good year.

If one looks at Sensex Annual Returns, one would have a very different experience of equity investing versus fear of losing money in the short term.

We can understand if one wishes to raise 10-20% cash in the equity portfolio, we will inform you which stocks to be sold if we see evidence of correction. The rest of the portfolio can be held despite volatility based on news flows. We can’t avoid volatility completely as markets move in unpredictable patterns.

For fresh funds, we recommend 50-75% investment into stocks/funds that will do well over the next 5 years. If your time horizon is long term, the current valuation will make lower sense as the law of averages will take your returns higher. Here is one such exercise:

How to think about market valuation

Let’s assume Nifty is indeed 20% expensive! (Nifty – led by a concentrated portfolio of Top 10 stocks – is around 20% higher than its fair price, not true for all stocks).

If Nifty were to give 13% CAGR returns over the next 10 years, buying 20% above fair value reduces your returns by 2% CAGR i.e. it will earn 11% CAGR versus 13% CAGR. Now it doesn’t look so bad.

If Nifty were to give 13% CAGR returns over the next 20 years, buying 20% above fair value reduces your returns by 1% CAGR i.e. it will earn 12% CAGR versus 13% CAGR. Now that’s a rounding error although it a reasonable sum in absolute terms.

We recommend equity investing only for long term savings so that near term events become irrelevant. We do not find any merit in second-guessing what’s going to happen in the next 6 months-1 year. If the shortlisted stocks are good companies, with good growth prospects, they will deliver returns in line with business performance. Picking the right stocks is easier than predicting the market direction.

We continue to recommend Gold Fund/Gold (up to 5-10% of the portfolio) as a hedge from contagion risks.

Avoid any type of regret while investing. Regret can come from either missing stock or not adding enough to a winning stock. Rather focus on overall strategy as explained above.

Beyond this, tinkering with asset allocation will only reduce long-term returns thereby missing one’s target corpus. We have diversified our stocks portfolio, we have diversified assets and we have a long term horizon. Together this takes care of all potential risks in investing.

MoneyWorks4me Outlook:

To know MoneyWorks4me way of investing:

If you liked what you read and would like to put it into practice Register at MoneyWorks4me.com. You will get amazing FREE features that will enable you to invest in Stocks and Mutual Funds the right way.

Register FREE | Schedule a DEMO | Solution Enquiry | Themes | Subscribe

![]()

Need help on Investing? And more….Puchho Befikar

Kyunki yeh paise ka mamala hai

Why MoneyWorks4me | Why Register | Call: 020 6725 8333 | WhatsApp 8055769463