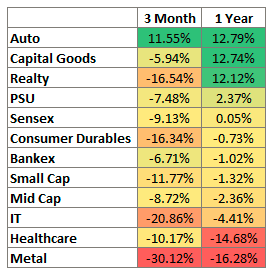

Zero returns in a year, but 33% up in 3 years!

As we write this note in June, we are staring at a 0% return by Sensex in the last 12 months. However, in the last 3 years, Sensex is up 33% a 10% CAGR.

In the last decade, and especially the last 2 years, low-interest rates and high liquidity led to a bull run in equities, globally. Now that the central banks are acting to control inflation with rate hikes equity prices are correcting across the board, some quite sharply.

Equity markets are factoring in higher inflation expectations, and rising crude oil prices. This is visible in the volatility which has remained high with Nifty Vix (volatility index) reaching its 52-week high in Feb’22.

Correction across the board

Among headline indices, metals have seen a sharp correction followed by Consumer Durables, Utilities, Metals, Healthcare, Realty, and IT. Metals, after a bull run for more than a year, saw a deep correction on account of the duty levied (for the steel sector), revision in margin expectations, and FPI outflows.

Market getting attractive

Nifty 50 index trades 4% above its fair value while there are pockets of extreme overvaluation and undervaluation. Nifty – led by a concentrated portfolio of Top 10 stocks – is around ~4% higher than its fair price, while the same is not true for all stocks. (Nifty@MRP 14,920 Dec’21).

The valuation gap has narrowed down by 10% since March 2022.

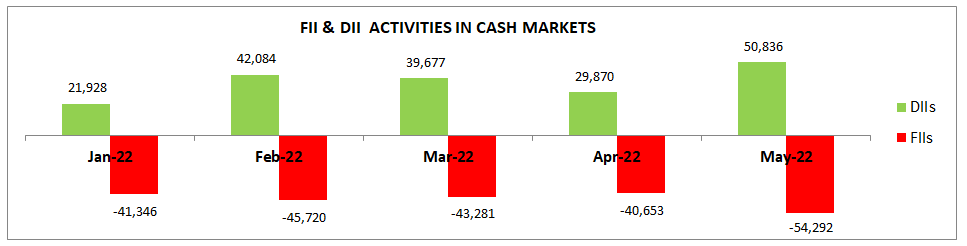

Local inflows countering FPI outflows…till now supporting the markets

India has witnessed one of the highest FPI outflows among peer markets – Indonesia, Philippines, S. Korea, and Taiwan. However, domestic player inflows have been compensating the FPI outflows, implying more resilience in our markets. From Jan’22 to May’22, FIIs have been the net sellers and have sold around $30 bn. This kind of outflow is huge considering the depth of the market. However, the market has been supported by the strong DII buying backed by the retail flows going into the equity market via SIP, Lump sum. We have already seen a record high Demat account opening in the last 2 years. DIIs have been net buyers and have bought ~$25 bn since the start of the year.

The amount of local flow supporting the equity markets is a phenomenon that is never seen before. Interestingly, the average ticket size of SIP is close to ~Rs. 3,000, which shows broader-based participation. Going forward, the flows are likely to be dependent on retail participation-directly and indirectly and the interest rate on other savings products.

Inflation- A decisive factor in rate movement

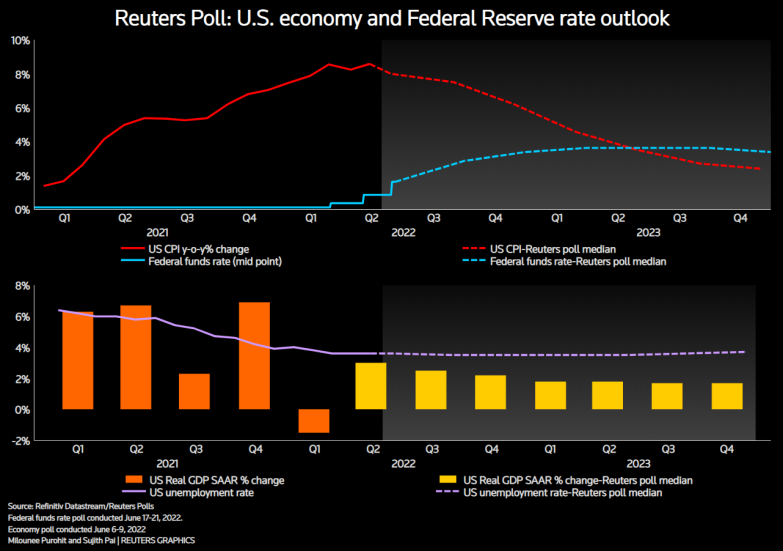

The U.S. Federal Reserve is moving toward policy re-normalization after having zero percent interest rates. The Federal Reserve has been desperately trying to control the inflation which has reached 40 years high at 8.6% as of May’22. FOMC meetings have been in line with market estimates of a 50 bps hike in the past two consequent meetings. The Fed is yet to calendar the contraction of its balance sheet, which is likely to reduce the money supply in the US, and FPI flows from India. Generally, it tends to keep the fed funds rate within a 2.0% to 5.0% sweet spot that helps maintain a healthy economy. Fed has raised the target range for the federal funds rate by 75 basis points to 1.50-1.75%. A further rise of 50 or 75 basis points (expected in July), would bring the total increase for this year to 2.00-2.25%.

In India, RBI also hiked the repo rates by 50 bps to 4.90% in Jun’22. CPI in the month of April was 7.79% and WPI was 15.1%. The key drivers were – transport, fuel, vegetables, oil, spices, and footwear – driven by indirect effects of the higher oil price impact on fertilizers, freight, derivatives of crude, and food prices among others. The governor cited increased inflation pressures following the Ukraine war and the resultant spike in crude oil prices as the reason for this hike.

Monsoon, Input Prices & Inflation- Key things to watch out for in the Indian Economy

GDP for Q4 FY22 may have slowed to 4.1% on account of the lockdown in January, but manufacturing PMI for May expanded. Monsoon has commenced early by 3 days in Kerala. Experts estimate unevenness between August and September which remains monitorable.

Near-term risks can come from rising inflation and supply chain disruptions caused by geopolitical tensions. India still imports the bulk of its crude oil requirement and gas. Higher crude prices could affect our fiscal deficit and yield assumption. Other commodities like natural gas or coal have also spiked due to shortage issues across several countries.

If this persists, it may result in a worsening trade deficit, and currency weakening and we may see risk to equity valuation. Corporates are highlighting the risks in cost structure as gross margins are getting squeezed. Companies are not taking price hikes in a hurry as it may impact volume growth. Rural wages have been weak as per the commentary from FMCG companies and lower entry-level 2W sales.

Tax Collection is robust, Pick up in rural incomes can drive consumption

On the positive side, GST collection for FY22 amounted to Rs 14.83 lakh crore, up 30% from Rs 11.37 lakh crore in FY21. Many domestic macro factors continue to provide tailwinds to economic growth. Both direct and indirect tax collections are showing robust growth. This could help cushion the widening fiscal deficit. Consumption and industrial indicators are showing improving trends. With higher rural inflation and the subsidy, farm incomes could improve. We believe the cyclical recovery will continue, though at a slower rate led by private CAPEX growth, weaker investment demand, and a softer consumption trend.

Valuations are reasonable

Considering the current valuation which falls in a fair value zone, we are optimistic about the Indian economy over the next 5 years. Even if we purchase shares at slightly higher prices, there is a good chance of earning healthy returns over the next 5 years. The Indian corporate sector is in the best position to gain pricing power and balance sheet strength. The majority of the sectors have seen consolidation. We are seeing this across sectors: Power, Telecom, Cement, Banks, NBFCs, Real Estate, building materials, Paper, pharma, capital goods, consumer durables, etc. This will give strong profitability for incumbents due to the high barrier to entry for the next few years.

Wait & watch as of now, despite the correction in the US

The US S&P500 has roughly 23% from its peak. We have been warning our investors about the overvaluation in the US market and had advised them to reduce their positions. Despite the correction, we would still seek some clarity on the growth and controlled inflation before we consider adding a position in US markets.

“The Federal Reserve is not trying to engineer a recession to stop inflation but is fully committed to bringing prices under control even if doing so risks an economic downturn”, U.S. central bank chief Jerome Powell said at a hearing before the Senate Banking Committee.

The interest rates are expected to rise as Fed has hinted at tightening financial conditions to put an end to the 40-year high inflation in the US. Financial conditions have comparatively tightened off late yet very easily compared to the historical perspective.

Global investment firms are lowering their estimates for real GDP growth for China to 3.8% from 4.3% for 2022 and to 5.0% from 5.4% for 2023, due to longer-than-expected lockdowns and a worse-than-expected housing market correction.

Cooling down of the war between Russia & Ukraine is another factor to be monitored that can decide the further course of global markets.

How are we looking at this?

Based on a current estimate, the average upside of our coverage universe is closer to 13-14% CAGR over the next 5 years basis.

Today, we are looking at opportunities in banking and finance, infrastructure, Utility PSUs, hospitals, autos, and logistics. We continue to remain positive on existing companies that are delivering good growth.

We have added stocks in the industrials and infra segment as their balance sheets are healthy and can participate in the CAPEX cycle. We expect cash flow growth to be better than past.

Despite of correction, we see Pharma and Chemicals trading at prices ahead of their earnings growth. As of now, we have limited our allocation in that space. The same is true with few private companies in the power sector.

IT has seen a sharp correction after a 2 year long Bull Run. We are being selective in that space. The company management is giving guidance for good growth for a year or two.

We look at companies that have good earning triggers over the next 2 years.

We are investing in companies;

- Coming out of sector consolidation/debt reduction, or

- Introducing new products, or

- Commissioning new capacities, or

- Executing orders in hand.

This gives certainty of growth rather than plain anticipation.

What sectors we are looking at?

After the intent of the government to continue giving a boost to the CAPEX and investment in public infrastructure, we remain positive on the companies that would benefit from the Capex cycle. Infra, logistics, and industrial-related companies would be the key beneficiaries.

We are incrementally adding to banks. Banks are the key beneficiaries of credit cycle pick-up. As industrial activity improves, the working capital loans will be drawn from banks which will lead to credit growth. In a period of rising interest rates, the banks tend to benefit for a limited period of time. That is because their liabilities are locked in at a fixed rate (which is lower) and their assets (loans) are at a floating rate. This gives them the benefit of better margins in a short term.

We had a cautious stance on banks as we expected slippages in unsecured and SME loans. But as economic recovery happened faster, we are seeing stability in retail and corporate balance sheets. Large banks (AUM > 1,00,000 Cr) have made sufficient provisions as well as raised money to maintain a healthy capital adequacy ratio. However, almost all the banks from our coverage universe have reported good earnings. March’22 earnings of Nifty were dominated by the earnings of Banks.

With the fear of NPA being behind, they will start lending in areas that are growing well. Recently, top managements from big-sized banks have confirmed that the companies in Infra, PSU, and manufacturing are seeing good traction in asset growth backed by order book and demand both domestic and overseas. The rising inflation has led to increasing in demand for working capital loans.

We expect this to be the start of the structural credit cycle and not a one-off considering all the factors in place. The factors such as clean and capitalized balance sheets of banks (lenders), de-leveraged balance sheets of corporates (borrowers), lesser capacity addition in the economy post-2013 leading to the need for more capacity given rising demand, Capex program by government improving the sentiments of private players to participate.

Beware of expensive stocks that have corrected from their highs

Not all the stocks that have corrected from their highs are worth buying. We recommend being cautious about prices that you are paying for the stocks and avoiding buying high P/E stocks that have fallen off from their highs. The current high-interest rate regime may lead to some of these stocks to not reach to those levels anytime soon. We believe that being selective in this kind of market towards quality stocks generating earnings and trading at reasonable valuations is a key to generating returns.

We recommend treading cautiously in small-cap companies where sales figures are below 2019 levels but may optically look at high growth today on a low base of 2020. We recommend using FY19-20 sales as a base while evaluating growth or valuation. (Compute P/E ratio using EPS of 2019/20, Compute P/S ratio using Sales of 2019/20). We use 1-year forward Sales and EPS figures as we estimate the future growth of companies.

We have shifted focus to Core stocks (Large Cap, market leaders) that have strong future prospects which will provide better downside protection. However, one has to keep return expectations moderate as valuations are no longer cheap but in the fair value zone.

What is MoneyWorks4me’s action plan for its subscribers?

Since we follow the QaRP way of investing we were cautious on markets in the past few months and that seems to have worked in our favor. We have been warning on higher perceived valuations and were not giving out buy calls despite some pressure from some subscribers.

Now that market is correcting, we are excited to BUY existing opportunities or new ones in near future. The deleveraged balance sheets of Indian corporates, sub-par capacity addition in the past decade, and increasing utilisation levels give us confidence on the credit cycle. This combined with the underperformance of the financial sector in the last couple of years gives us confidence on the prospects of lenders (BFSI sector).

We believe that the current economy recovery is led by the credit growth cycle which can be delayed but remains definitive. Also, the Indian corporate sector is in the best position to gain pricing power and balance sheet strength. The majority of the sectors have seen consolidation. We are looking at sectors that will be early beneficiaries of these two themes.

MoneyWorks4me Outlook:

How to Invest in Stocks Systematically & Succeed?:

Best Stocks From:

Nifty 50 Nifty Next 50 Nifty 100 Nifty 200 Nifty 500 Nifty Financial Services SmallCap 250 MidCap 100

![]()

Need help on Investing? And more….Puchho Befikar

Why MoneyWorks4me | Call: 020 6725 8333 | WhatsApp: 8055769463