Stocks - Q : Quality | V : Valuation | PT : Price Trend

Funds - P : Performance | Q : Quality

Funds - P : Performance | Q : Quality

BSE: 543328 | NSE: KRSNAA | Hospital & Healthcare Services | Small Cap

Data adjusted to bonus, split, extra-ordinary income, rights issue and change in financial year end.

Value Creation Index Colour Code Guide ⓘ

| Mar'14 | Mar'15 | Mar'16 | Mar'17 | Mar'18 | Mar'19 | Mar'20 | Mar'22 | Mar'23 | Mar'24 | TTM | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| ROCE % ⓘ | 0% | 0% | 0% | 0% | 0% | 0% | 0% | 14.5% | 11.8% | 9.9% | - |

| Value Creation Index ⓘ | NA | NA | NA | NA | NA | NA | NA | 0.0 | -0.2 | -0.3 | - |

Growth Parameters ⓘGrowth Parameters Colour Code Guide ⓘ | |||||||||||

| Sales ⓘ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 455 | 487 | 620 | 697 |

| Sales YoY Gr. | - | NA | NA | NA | NA | NA | NA | NA | 7% | 27.2% | - |

| Adj EPS ⓘ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 21.8 | 19.7 | 17.6 | 23.4 |

| YoY Gr. | - | NA | NA | NA | NA | NA | NA | NA | -9.6% | -10.8% | - |

| BVPS (₹) ⓘ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 217.3 | 234.4 | 250.1 | 266.4 |

| Adj Net Profit ⓘ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 68.6 | 62 | 56.9 | 76 |

| Cash Flow from Ops. ⓘ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 128 | 76.3 | 24.4 | - |

| Debt/CF from Ops. ⓘ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.3 | 0.4 | 6.6 | - |

CAGR Colour Code Guide ⓘ

| 9 Years | 5 Years | 3 Years | 1 Years | |||||

|---|---|---|---|---|---|---|---|---|

| Sales ⓘ | NA | NA | NA | 27.2% | ||||

| Adj EPS ⓘ | NA | NA | NA | -10.8% | ||||

| BVPSⓘ | NA | NA | NA | 6.7% | ||||

| Share Price | - | - | 8.7% | 35.5% | ||||

Performance Ratio Colour Code Guide ⓘ

| Mar'14 | Mar'15 | Mar'16 | Mar'17 | Mar'18 | Mar'19 | Mar'20 | Mar'22 | Mar'23 | Mar'24 | TTM | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Return on Equity % ⓘ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 10 | 8.7 | 7.4 | 9.1 |

| Op. Profit Mgn % ⓘ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 28.9 | 25.1 | 23.3 | 25.9 |

| Net Profit Mgn % ⓘ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 15.1 | 12.7 | 9.2 | 10.9 |

| Debt to Equity ⓘ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.1 | 0 | 0.2 | - |

| Working Cap Days ⓘ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 196 | 225 | 107 |

| Cash Conv. Cycle ⓘ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | -20 | 28 | 23 |

| Standalone | Consolidated | |

|---|---|---|

| TTM EPS (₹) | 24.8 | 23.4 |

| TTM Sales (₹ Cr.) | 666 | 697 |

| BVPS (₹.) ⓘ | 269.6 | 266.4 |

| Reserves (₹ Cr.) ⓘ | 854 | 844 |

| P/BV ⓘ | 2.82 | 2.85 |

| PE ⓘ | 30.61 | 32.44 |

| From the Market | |

|---|---|

| 52 Week Low / High (₹) | 527.55 / 1041.80 |

| All Time Low / High (₹) | 354.00 / 1099.50 |

| Market Cap (₹ Cr.) | 2,454 |

| Equity (₹ Cr.) | 16.1 |

| Face Value (₹) | 5 |

| Industry PE ⓘ | 43.1 |

| Mar'24 | YoY Gr. Rt. % | Jun'24 | YoY Gr. Rt. % | Sep'24 | YoY Gr. Rt. % | Dec'24 | YoY Gr. Rt. % | |

|---|---|---|---|---|---|---|---|---|

| Sales (₹ Cr.)ⓘ | 103 | -36.4 | 100 | 6.7 | 130 | 52.3 | 112 | 7.2 |

| Adj EPS (₹) ⓘ | 3.3 | -17.9 | 2.1 | 7.7 | 3 | 151.7 | 1.1 | -39 |

| Op. Profit Mgn % ⓘ | 29.30 | 821 bps | 23.90 | 505 bps | 26.32 | 1177 bps | 16.44 | -492 bps |

| Net Profit Mgn % ⓘ | 17.28 | 393 bps | 11.16 | 9 bps | 12.23 | 481 bps | 5.12 | -391 bps |

| Pledged * | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

Analyzing Krsnaa’s annual report we have compiled a report, with an overview of the sector, growth strategies, balance sheet and management changes as well as our observations. Read our Initiating Note to understand Krsnaa’s business model in depth.

Profile of the company-

Krsnaa Diagnostics (KDL) is one of the largest players in the diagnostic sector through Public-Private Partnerships (PPP). The company focuses on making quality diagnostic services accessible and affordable to a large portion of the Indian population. By collaborating with both government and private hospitals, Krsnaa Diagnostics serves communities in urban, semi-urban and rural areas. Its wide range of radiology, pathology, and teleradiology services has allowed it to expand its presence across the country.

Sector tailwinds and increased government allocation aiding PPP diagnostics-

Opportunity and threats

Growth Strategies

B2C – leveraging existing infrastructure to directly reach customers

KDL is strategically expanding its retail segment, which currently accounts for only 1-2% of its revenue, revealing significant growth potential. The company plans to leverage its existing infrastructure in key locations like Maharashtra, Punjab, Orissa, and Assam to scale its retail presence. The company will first start by offering pathology services and setting up collection centers using existing labs for testing. This will ensure initial capital outlay will be limited. Pricing for such services will be higher than the B2G segment but will remain competitive compared to the broader market. Margins by year-end are expected to be in line with broader operations once stabilized (~25% EBITDA).

Krsnaa has already inaugurated its first B2C private lab in Mumbai, covering 15,000 sq. ft. To enhance brand recall and customer growth, Krsnaa is focusing on telereporting, effective branding, and marketing initiatives while ensuring affordable, high-quality services. Additionally, it aims to strengthen brand recognition and customer loyalty through efficient service delivery and is expanding its in-home visit services for greater healthcare accessibility. To further this expansion, the company plans to broaden its service portfolio, diversify its reach through a franchisee model, and solidify its Hospital Lab Management (HLM) model.

Profitability to be driven by newly launched and semi-matured centers-

Source: Moneyworks4me research

Centers operational for over 3 years show higher margins, while those under 3 years tend to be around break-even levels. New centers (less than 1.5 years) face negative margins due to higher initial costs during the ramp-up phase. Revenue growth happens gradually, with investments today laying the foundation for future profitability. Typically, PPP projects take 1-2 years to stabilize, and by year 3, centers reach maturity. Although this can vary by project, this trend indicates performance will improve as projects mature.

Some changes in the balance sheet that are worth highlighting-

Source: Moneyworks4me research; Note- Numbers before FY22 are on standalone basis

Source: Annual report

Source: Moneyworks4me research

Source: Annual report

Source: Annual report

Changes to the board, CEO and capability highlights-

Source: Annual report

In conclusion, Krsnaa Diagnostics continues to strengthen its position as a leading player in the diagnostic sector through strategic initiatives and expansion plans. The company’s focus on Public-Private Partnerships (PPP) and the maturing profile of its centers will drive growth. With increased government support, sector tailwinds, and the expansion of its B2C segment, Krsnaa is well-positioned for the future. The company's financials remain healthy despite temporary working capital challenges, and its leadership changes signal a strong foundation for further growth. Krsnaa’s ability to capitalize on emerging opportunities and deliver affordable, quality healthcare services will be key to its long-term success.

Good results with growth on track. Revenues to be driven by ramp up in recent contracts as well as pathology and retail expansion. EBITDA margin has room to improve further.

Steady growth continues in the quarter, the company achieved 25 % YoY revenue growth and 28% YoY EBITDA growth on account of incremental revenues from newly launched centres & operational efficiencies.

Few points worth noting are:

Particulars | Q2FY24 (Rs. Crs) | YoY Trend | Comments |

| Revenue | 155 | +26% | The company has completed the operationalization of the Orissa Pathology tender. |

| EBITDA | 32 | +3% | Rs. 7 Cr was incurred in operationalizing new centers & ESOP costs. Normalised EBITDA was Rs. 39 Cr. |

| EBITDA Margin | 21% | -460 bps | Higher material costs were on account of higher pathology revenue. Normalised EBITDA margin was 25% |

| PAT | 10 | -33% | Higher Depreciation and Interest costs led to fall in net margins |

Overall decent results even though they look bad optically. We expect positive trajectory of revenues along with 25% EBITDA margin to continue in the coming quarters.

The Indian diagnostic industry is expected to be supported by various fundamental growth drivers like the ageing population, rising awareness for healthcare, penetration in rural areas, as well as increasing investment by both government and private players. The industry is expected to grow at a CAGR of around 15% for the next few years, which presents a huge opportunity size.

With increasing government focus on providing high quality healthcare services, the rising prevalence of schemes like Ayushman Bharat, it is expected to boost the PPP (Public-Private Partnership) model in the diagnostic industry and Krsnaa’s business fundamentals are fully aligned to tap in this growing opportunity.

Krsnaa Business Model:

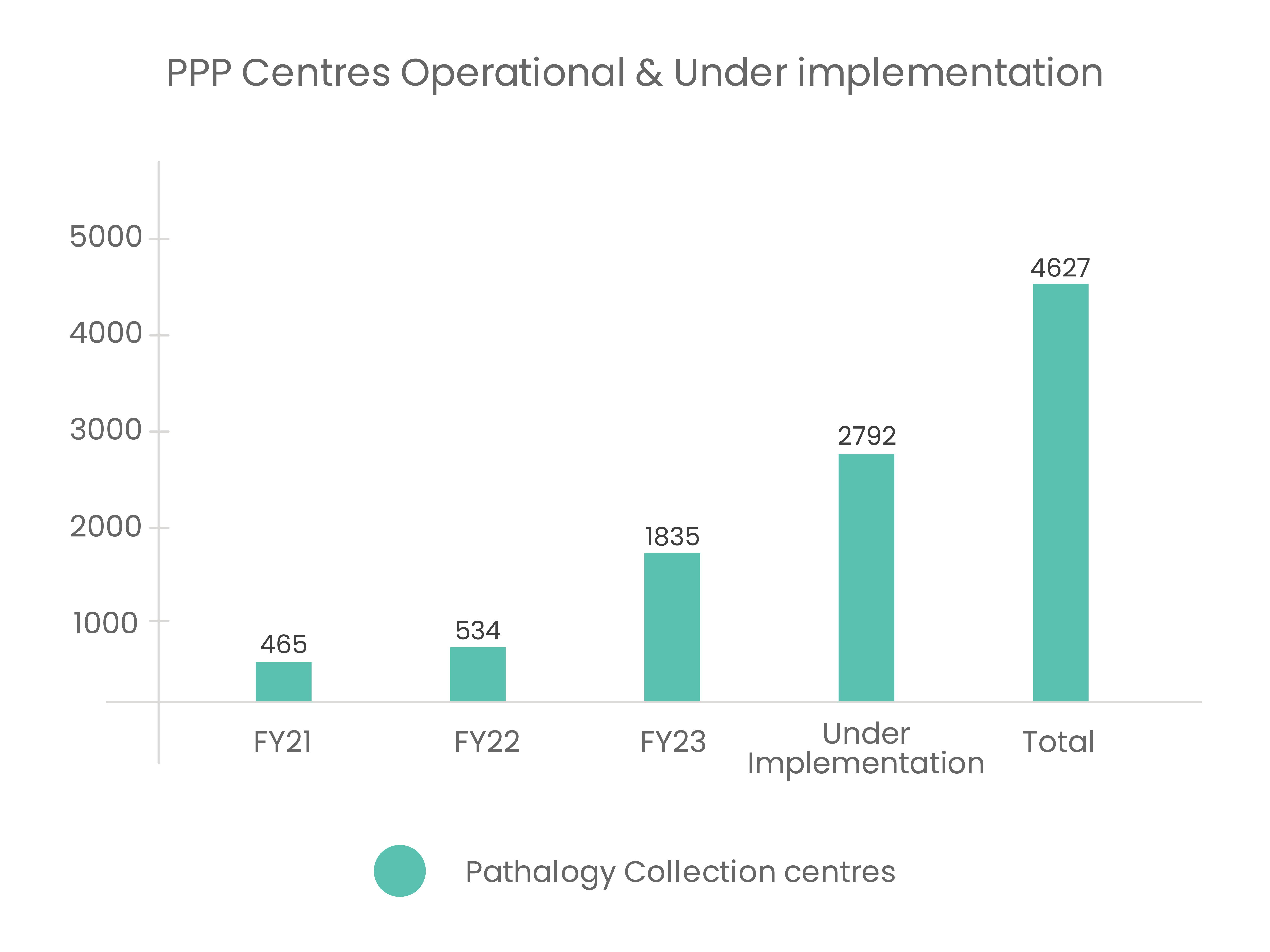

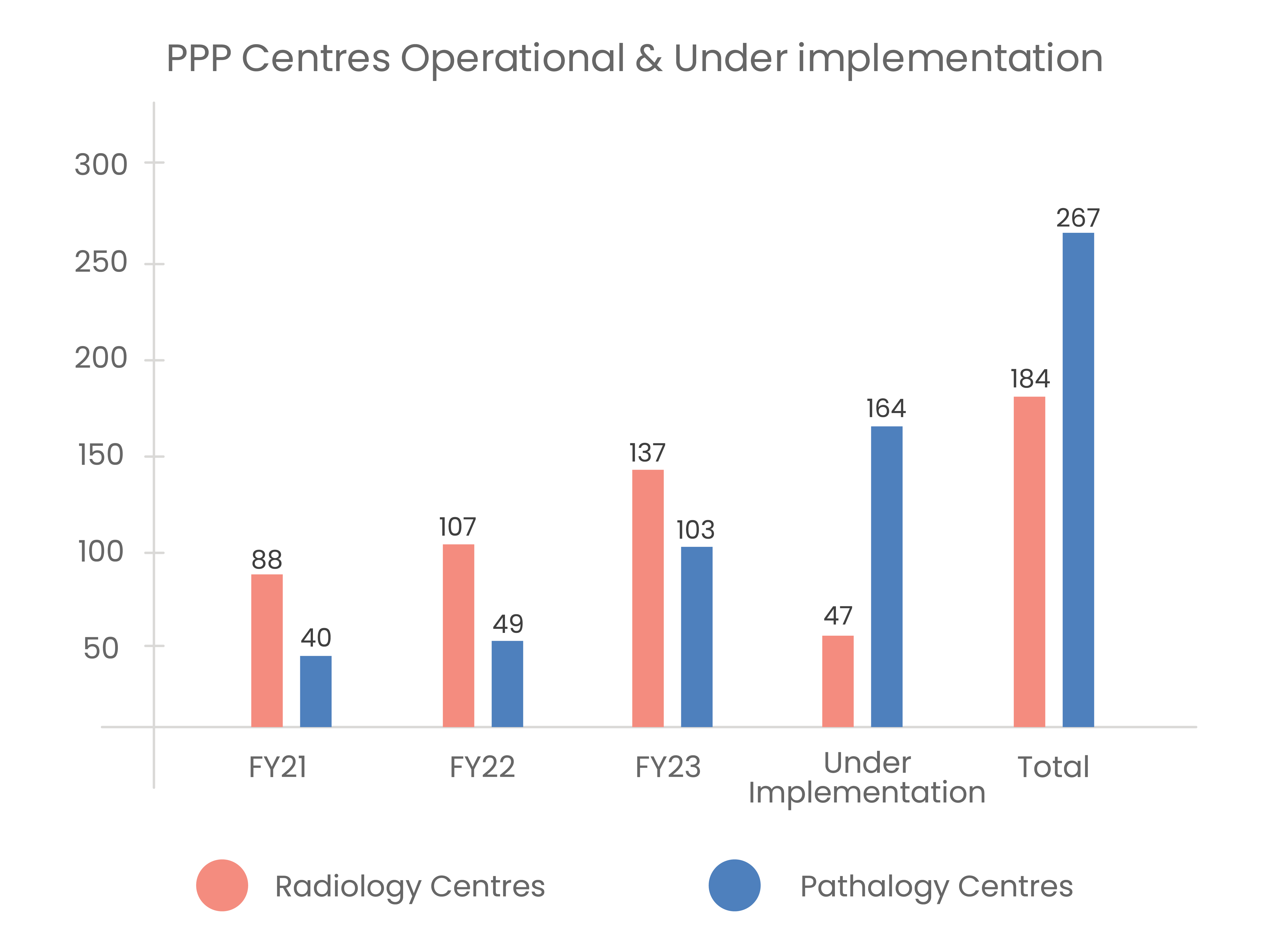

The company provides Radiology, Pathology and Tele-Radiology services. It has a leadership role as a PPP diagnostic entity, boasting 134 radiology centres, 1,370 tele-reporting centres, 105 pathology processing labs, and an extensive network of 1,336 pathology collection centres. The 3 important dimension of its business model are:

Value proposition:

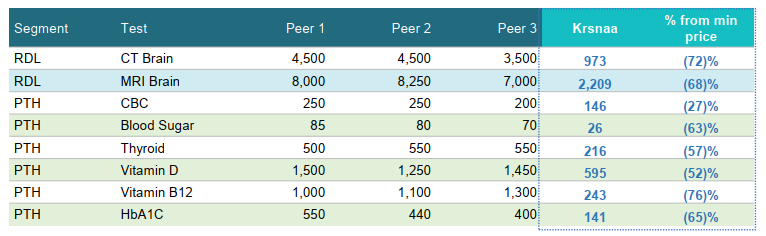

Krsnaa offers quality diagnostic services at disruptive prices. Its tests are almost 40% to 70% lower than the market rates which makes it a good value proposition for low-income households.

(Source: Company reports)

Despite these lower prices, the company has been able to deliver healthy operating margins which are equivalent to its peers.It has been able to do this because of the following reasons:

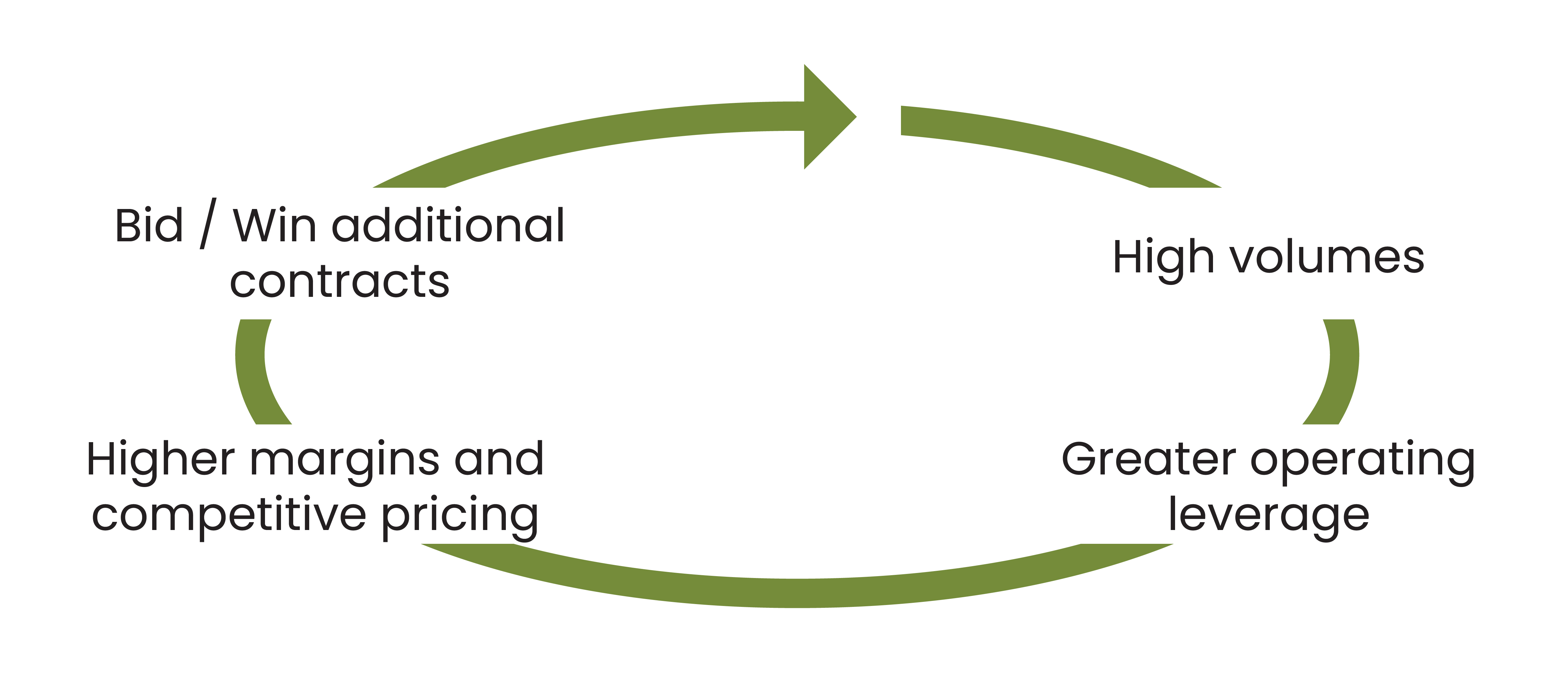

Competitive Advantage:

The loop of low cost due to high volumes & additional contract wins due to being the lowest-cost provider works as follows:

(Source: Company reports)

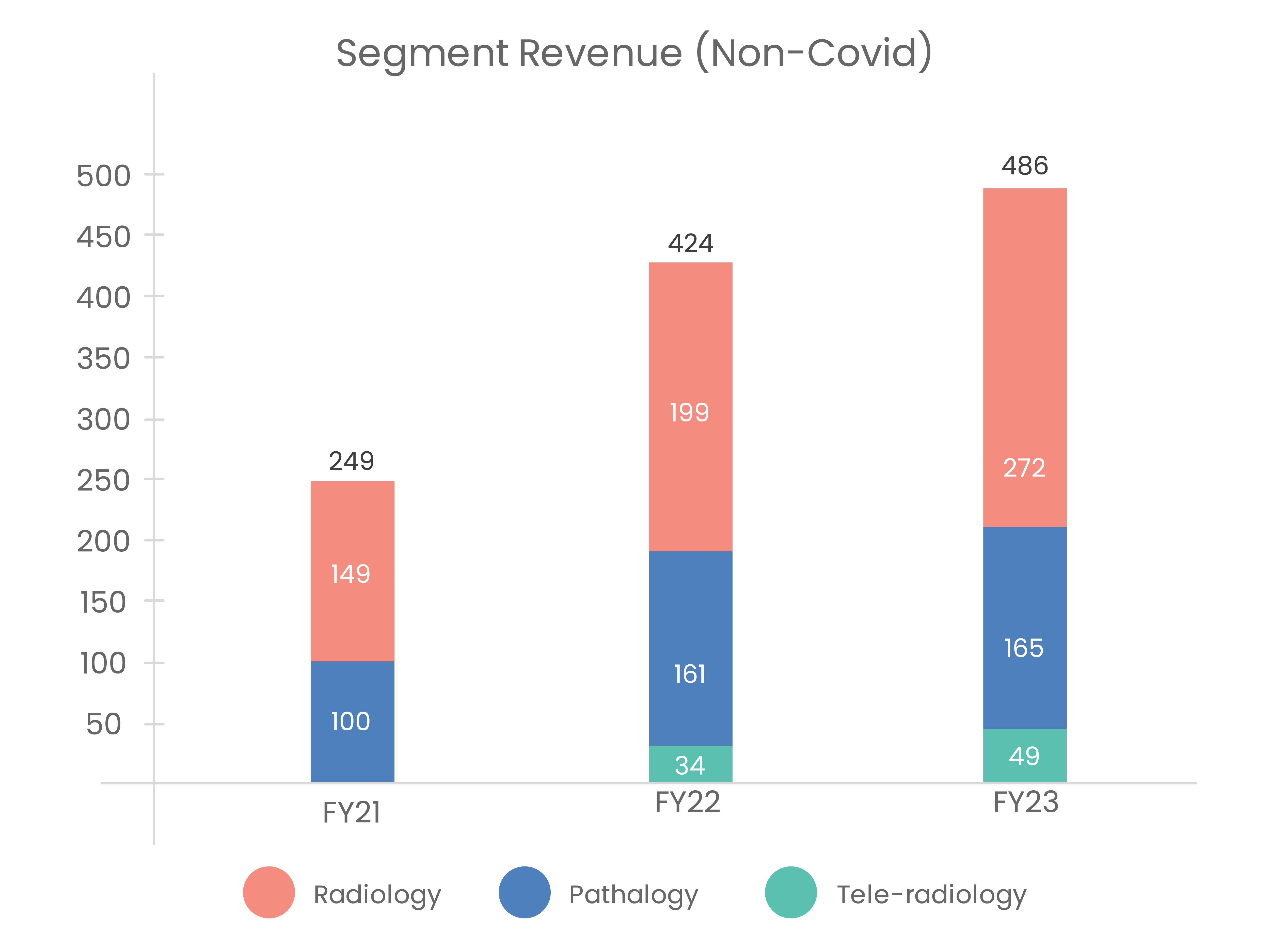

Segment-wise Business Performance:

(Source: Company Reports, Moneyworks4me research)

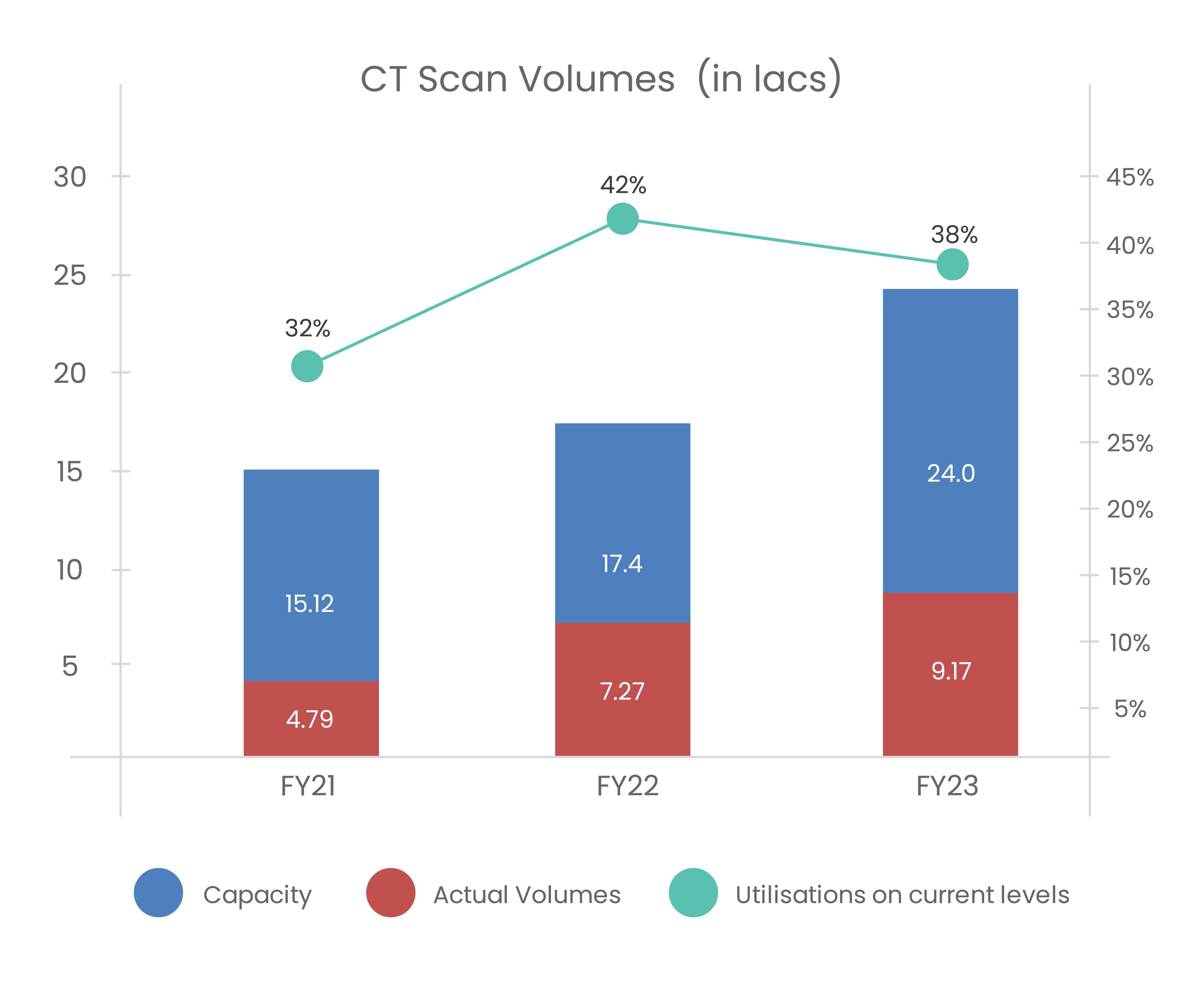

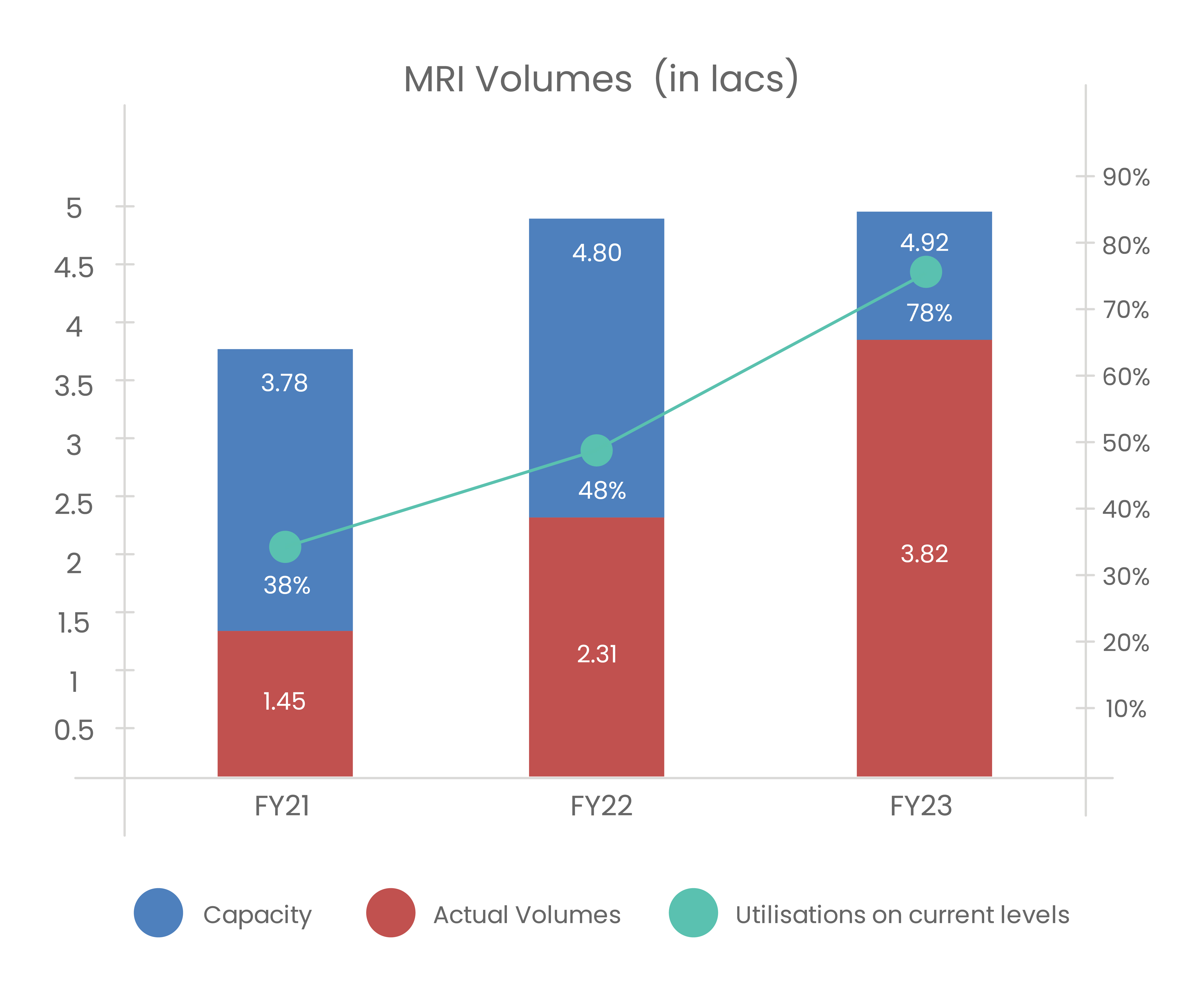

Radiology Segment: This includes CT Scans, MRI, Sonography, Mammography and X-rays. Machinery costs are high in this segment (~2 Cr for a CT scan machine & ~6 Cr for an MRI machine) while variable costs are very low. Once Radiology centres reach optimum utilisation levels (~60-70%) is when we get high ROCE from these centres. The maturity profile for the company’s radiology centers is outlined below.

(Source: Company reports)

Radiology segment has been growing at a CAGR of 36% from FY18 to FY23. Newly launched centres reaching semi-matured stage shall provide a high incremental ROCE for the company going forward.

(Source: Company Reports, Moneyworks4me research)

(Source: Company Reports, Moneyworks4me research)

Pathology Segment: This includes Routine Testing (Microbiology, Histopathology, Serology and Immunoassay) and Specialized Testing (Biochemistry, Molecular Biology, Oncology Genomics and personalized precision-based medicine). Capital outlay in this segment is significantly lower as against the Radiology segment. Major costs are Reagents and testing kits (20-25%).

(Source: Company Reports, Moneyworks4me research)

Pathology segment has been growing at a CAGR of 33% from FY18 to FY23. Recently secured tender are dominated by Pathology and thus this segment shall form a significant part of the company’s future revenues.

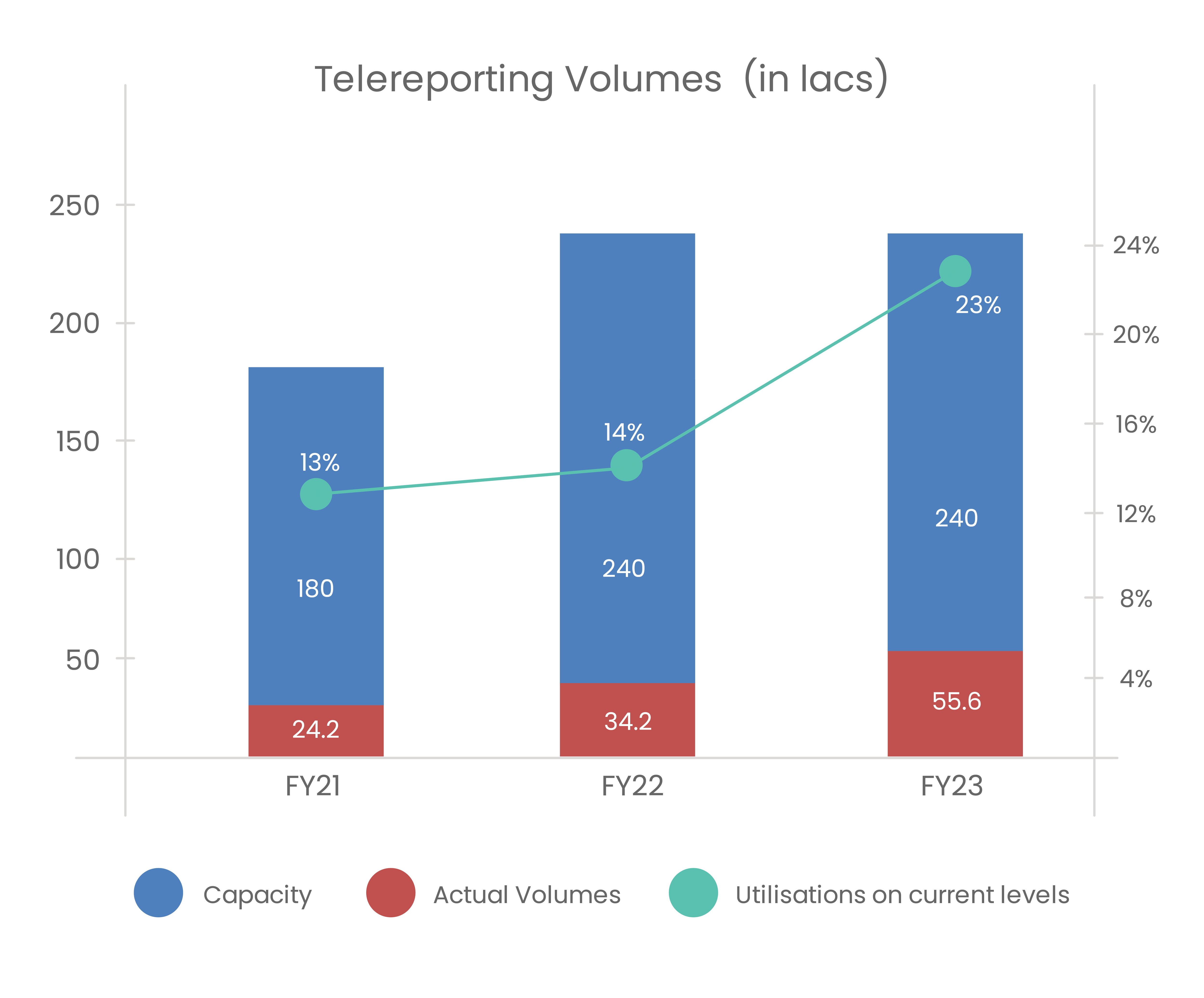

Tele-reporting Segment:

Krsnaa’s Tele-radiology services which it operates from Pune, is one of India's largest Tele-radiology reporting hub. At this facility, it has a team of 240+ radiologists from India and abroad, wherein it examines digital images and prepares reports. It provides 24x7 uninterrupted connectivity between diagnostic centers and the hub. This is a unique proposition that addresses the issue of shortage of full-time doctors and staff in the diagnostic industry. It also considerably increases the turnaround time for the reports. In addition, it also allows it to serve patients in remote locations where diagnostic facilities are limited.

(Source: Company Reports, Moneyworks4me research)

In FY23, the Tele-radiology segment had a revenue contribution of Rs. 49 Cr. However, Reporting costs associated with the tele-reporting segment were Rs. 52 Cr which implies that the segment is making nominal losses at the moment as there are significant fixed costs associated with maintaining such a setup. Currently, utilisation in the Tele-reporting segment is low as seen in the radiology capacity utilisation matrix provided below, but it is improving at a fast pace and soon the segment will provide a lift to the margin profile.

Concerns:

Levers for Growth:

The company is set to deploy & commercialize significant resources in the states of Maharashtra, Rajasthan, Assam, & UP as provided below:

(Source: Company Reports, Moneyworks4me research)

The Rajasthan project hurdles have finally been removed, The Government of Rajasthan earlier had proposed to implement the project in 33 districts only, which it has now increased to 50 districts in total. The expected revenue from this project alone could be to the tune of Rs. 250-300 Cr per year (3 years contract with 2 years extension optional between the parties)

The company has recently secured a significant tender in the state of Assam. This project encompasses a network of 10 laboratories and 1,256 collection centers, significantly boosting its growth prospects in the northern-eastern region of the country, where government healthcare holds an 80% share.

(Source: Company Reports, Moneyworks4me research)

Capex outlay in FY 24 & 25 for the above project is Rs. 120-130 Cr per year. This shall keep ROE diluted in the meantime. The key thing to focus on here is that once all the capex is done and these facilities reach considerable utilisation, how big a size the company can become.

Due to its existing investment in equipment, large scale of operations and cost competitiveness, Krsnaa has a strong bid-win rate of 79% with 100% technical qualification in the past. Tender contracts typically range between 3-5 years for Pathology and go to about 10 years in the Radiology segments. The ability to quote attractive pricing at the time of renewal and a track record of successfully renewing the contract provides them revenue visibility in terms of tenure as well as gives a high chance of renewal.

Presently company is present in 14 states; however majority of the revenue (44%) comes from the West region. In some of the states where it already has a presence, the size of the contracts is very small. Their strategy involves both organic and inorganic growth. They plan to expand organically by partnering with public health agencies, private hospitals, medical colleges, and community health centers. Inorganically, they aim to make value-enhancing acquisitions to consolidate their business and leadership position. There are quite a few states currently that aren’t yet on the bandwagon of the PPP model in hospitals, their coming in will provide further scope for the growth of the company.

| Company Name | CMP(₹) | |||||||

|---|---|---|---|---|---|---|---|---|

| Narayana Hrudayalay | 1,796.9 | -3.1 (-0.2%) | Small Cap | 5,018 | 38.4 | 15.7 | 46.9 | 10.8 |

| Aster DM Healthcare | 510.3 | 4.5 (0.9%) | Small Cap | 3,699 | 105.6 | 5.5 | 4.8 | 7.2 |

| Dr. Lal Pathlabs | 2,787.7 | 20.7 (0.8%) | Small Cap | 1,967 | 55.3 | 19.5 | 50.1 | 10.6 |

| Indraprastha Medical | 420.1 | -4.4 (-1%) | Small Cap | 1,245 | 16.5 | 10 | 25.7 | 7 |

| RainbowChildrenS Med | 1,425.6 | -24.1 (-1.7%) | Small Cap | 1,237 | 23 | 17.4 | 63.1 | 10.3 |

| Krishna Inst.Medi | 667.1 | -24.6 (-3.6%) | Small Cap | 1,222 | 6.4 | 19.3 | 107.4 | 13.3 |

| Kovai Medical Center | 5,598.5 | 18.2 (0.3%) | Small Cap | 1,220 | 188.7 | 14.8 | 29.6 | 5.9 |

| Metropolis Health. | 1,762.9 | 11.4 (0.7%) | Small Cap | 1,208 | 29.7 | 11 | 59 | 7.4 |

| HealthcareGlobal | 567.5 | -6.6 (-1.1%) | Small Cap | 1,099 | -0.8 | 3 | - | 6.8 |

| Jupiter Life Line | 1,498.8 | -0.3 (-0%) | Small Cap | 911 | 28 | 16.7 | 53.6 | 7.1 |

| PARTICULARS | Mar'22 | Mar'23 | Mar'24 |

|---|---|---|---|

| Sales | 455 | 487 | 620 |

| Operating Expenses ⓘ | 324 | 365 | 475 |

| Manufacturing Costs | 135 | 108 | 90 |

| Material Costs | 60 | 74 | 141 |

| Employee Cost | 54 | 75 | 111 |

| Other Costs ⓘ | 75 | 108 | 133 |

| Operating Profit ⓘ | 131 | 122 | 144 |

| Operating Profit Margin (%) | 28.9% | 25.1% | 23.3% |

| Other Income ⓘ | 15 | 19 | 17 |

| Interest ⓘ | 18 | 8 | 16 |

| Depreciation ⓘ | 41 | 54 | 75 |

| Exceptional Items ⓘ | 0 | 0 | 0 |

| Profit Before Tax ⓘ | 87 | 80 | 70 |

| Tax ⓘ | 18 | 18 | 13 |

| Profit After Tax | 68 | 62 | 57 |

| PAT Margin (%) | 15.0% | 12.8% | 9.2% |

| Adjusted EPS (₹) | 21.8 | 19.8 | 17.6 |

| Dividend Payout Ratio (%) | 11% | 14% | 14% |

| PARTICULARS | Mar'22 | Mar'23 | Mar'24 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

Equity and Liabilities | ||||||||||

| Shareholders Fund | 682 | 736 | 807 | |||||||

| Share Capital ⓘ | 16 | 16 | 16 | |||||||

| Reserves ⓘ | 667 | 720 | 791 | |||||||

| Minority Interest | 0 | 0 | 0 | |||||||

| Debt | 33 | 24 | 138 | |||||||

| Long Term Debt | 33 | 24 | 42 | |||||||

| Short Term Debt | 0 | 0 | 96 | |||||||

| Trade Payables | 77 | 62 | 82 | |||||||

| Others Liabilities ⓘ | 83 | 86 | 143 | |||||||

| Total Liabilities ⓘ | 875 | 909 | 1,170 | |||||||

Fixed Assets | ||||||||||

| Gross Block | 491 | 627 | 874 | |||||||

| Accumulated Depreciation | 106 | 156 | 226 | |||||||

| Net Fixed Assetsⓘ | 386 | 471 | 647 | |||||||

| CWIP ⓘ | 28 | 25 | 10 | |||||||

| Investmentsⓘ | 0 | 0 | 0 | |||||||

| Inventories | 9 | 25 | 36 | |||||||

| Trade Receivables | 58 | 73 | 176 | |||||||

| Cash Equivalents | 242 | 109 | 54 | |||||||

| Others Assetsⓘ | 152 | 205 | 247 | |||||||

| Total Assets ⓘ | 875 | 909 | 1,170 | |||||||

| PARTICULARS | Mar'22 | Mar'23 | Mar'24 |

|---|---|---|---|

| Cash Flow From Operating Activity ⓘ | 128 | 76 | 24 |

| PBT ⓘ | 87 | 80 | 70 |

| Adjustment ⓘ | 49 | 45 | 70 |

| Changes in Working Capital ⓘ | -1 | -36 | -97 |

| Tax Paid ⓘ | -7 | -13 | -19 |

| Cash Flow From Investing Activity ⓘ | -241 | -109 | -129 |

| Capex | -131 | -135 | -193 |

| Net Investments | -126 | 16 | 54 |

| Others ⓘ | 17 | 10 | 10 |

| Cash Flow From Financing Activityⓘ | 176 | -33 | 84 |

| Net Proceeds from Shares ⓘ | 400 | 0 | 23 |

| Net Proceeds from Borrowing ⓘ | -159 | -9 | -6 |

| Interest Paid ⓘ | -16 | -5 | -12 |

| Dividend Paid ⓘ | 0 | -8 | -9 |

| Others ⓘ | -48 | -11 | 88 |

| Net Cash Flow ⓘ | 64 | -66 | -20 |

| PARTICULARS | Mar'22 | Mar'23 | Mar'24 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Ratios | ||||||||||

| ROE (%) | 10.02 | 8.76 | 7.36 | |||||||

| ROCE (%) | 14.47 | 11.75 | 9.94 | |||||||

| Asset Turnover Ratio | 0.52 | 0.55 | 0.6 | |||||||

| PAT to CFO Conversion(x) | 1.88 | 1.23 | 0.42 | |||||||

| Working Capital Days | ||||||||||

| Receivable Days | 46 | 49 | 73 | |||||||

| Inventory Days | 7 | 13 | 18 | |||||||

| Payable Days | 468 | 343 | 187 | |||||||

Krsnaa Diagnostics is one of the largest differentiated diagnostic service provider in India. It provides a range of technology-enabled diagnostic services such as imaging (including radiology), pathology/clinical laboratory and tele-radiology services to public and private hospitals, medical colleges and community health centres pan-India. It also operate one of India’s largest tele-radiology reporting hubs in Pune that is able to process large volumes of X-rays, CT scans and MRI scans round the clock and 365 days a year, and allows it to serve patients in remote locations where diagnostic facilities are limited. It provides quality and inclusive diagnostic services at affordable rates across various segments.

The company offers range of diagnostics imaging services and clinical laboratory tests that include both routine and specialized tests / studies and profiles, which are used for prediction, early detection, diagnostic screening, confirmation and/or monitoring of diseases. Its diagnostic imaging/radiology services include conducting X-rays, computed tomography (CT) scans, magnetic resonance imaging (MRI) scans, ultrasounds, bone mineral densitometry and mammography. In its pathology segment, its primary focus includes biochemistry, haematology, clinical pathology, histopathology and cytopathology, microbiology, serology and immunology. A suite of diagnostic equipment is located at its tele-radiology hub along with a team of radiologists which provide it significant operating efficiencies and scalability.

Business area of the company

Krsnaa Diagnostics is one of the fastest-growing diagnostic chains in India. The company offers a wide range of diagnostic services such as imaging/radiology services (X-rays, MRI, etc.), routine clinical laboratory tests, pathology, and tele-radiology services to private and public hospitals, medical colleges, and community health centres.

Key awards, accreditations or recognitions

Major events and milestones

MoneyWorks4Me rating and ranking of funds for SIP is available to subscribers only. Moneyworks4Me is not a rating and ranking agency, however it is required that users have a way of selecting funds and building a Portfolio. The method used by it are described below to enable users to understand the logic behind the rating and ranking Subscriber will find more details on this in the various content made available from time to time. In case you need more please write to besafe@moneyworks4Me.com

MoneyWorks4Me rates and ranks mutual funds based on the following data-driven system:

Funds ranking in screeners: Performance Consistency and Quality are two parameters used for ranking funds for SIP. The ranking as follows GG, GO, GR, OG, OO, OR, RG, RO and RR.

With the same color-coded funds, the one with the higher Average 3-year rolling returns (over 5 to 10 years), the number that appears in the Performance tag, ranks higher.

Here is the summary:

The third tag Upside Potential is not relevant for SIP. It is relevant for lumpsum investments in Mutual Funds.

Make an informed decision for Stocks

Invest using an intelligent system with powerful data-driven tools that help you identify opportunities and make informed buy-hold-sell decisions

Buy quality Stocks when they are available at reasonable prices and supported by an upward price trend and Sell when they are Overvalued using the Decizen Rating System. Covers 3500+ stocks

Account Discovery

- OTP from CAMS

Account Linking for Stocks & MF

- One OTP per link Eg. NSDL, CDSL, CAMS, KFin etc.

One Click Upload for your Current Portfolio and Future Transactions!

Download APP

Download APP