Invest in the best stock opportunities right now and every-time.

Start Systematic Stock Investing ...in less than a minute.

Past 10 year's financial track record analysis by Moneyworks4me indicates that Rossari Biotech Ltd is a good quality company.

The key valuation ratios of Rossari Biotech Ltd's currently when compared to its past seem to suggest it is in the Undervalued zone.

The Price Trend analysis by MoneyWorks4Me indicates it is Weak which suggest that the price of Rossari Biotech Ltd is likely to Fall in the short term. However, please check the rating on Quality and Valuation before investing.

Data adjusted to bonus, split, extra-ordinary income, rights issue and change in financial year end.

Value Creation Index Colour Code Guide ⓘ

| Mar'15 | Mar'16 | Mar'17 | Mar'18 | Mar'19 | Mar'20 | Mar'21 | Mar'22 | Mar'23 | Mar'24 | TTM | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| ROCE % ⓘ | 10.7% | 10.3% | 26.4% | 40.4% | 54.4% | 37.9% | 28.8% | 24.4% | 18.5% | 18.4% | - |

| Value Creation Index ⓘ | -0.2 | -0.3 | 0.9 | 1.9 | 2.9 | 1.7 | 1.1 | 0.8 | 0.3 | 0.3 | - |

Growth Parameters ⓘGrowth Parameters Colour Code Guide ⓘ | |||||||||||

| Sales ⓘ | 171 | 179 | 233 | 292 | 516 | 600 | 709 | 1,483 | 1,656 | 1,831 | 1,973 |

| Sales YoY Gr. | - | 4.4% | 30.6% | 25% | 76.9% | 16.3% | 18.2% | 109.1% | 11.7% | 10.6% | - |

| Adj EPS ⓘ | 0.8 | 0.7 | 3.3 | 5.9 | 9.5 | 12.6 | 15.3 | 16.3 | 18.3 | 22.6 | 24.6 |

| YoY Gr. | - | -7.9% | 364.3% | 81.9% | 60.1% | 33.1% | 21.8% | 6% | 12.9% | 23.1% | - |

| BVPS (₹) ⓘ | 9.7 | 10.3 | 13.5 | 19.5 | 25.6 | 56.4 | 78.3 | 145.7 | 165.3 | 189 | 207.6 |

| Adj Net Profit ⓘ | 3.7 | 3.4 | 15.7 | 28.6 | 45.8 | 63.9 | 79.6 | 89.5 | 101 | 125 | 136 |

| Cash Flow from Ops. ⓘ | 8.1 | 25.7 | 7.2 | 23.6 | 71.2 | 56.8 | 47.8 | 29.4 | 152 | 43.3 | - |

| Debt/CF from Ops. ⓘ | 5.4 | 0.9 | 3.1 | 0.9 | 0.1 | 1.2 | 0 | 0.3 | 0.5 | 2.5 | - |

CAGR Colour Code Guide ⓘ

| 9 Years | 5 Years | 3 Years | 1 Years | |||||

|---|---|---|---|---|---|---|---|---|

| Sales ⓘ | 30.1% | 28.8% | 37.2% | 10.6% | ||||

| Adj EPS ⓘ | 45.8% | 19% | 13.8% | 23.1% | ||||

| BVPSⓘ | 39.1% | 49.2% | 34.1% | 14.4% | ||||

| Share Price | - | - | -14.3% | -14.6% | ||||

Performance Ratio Colour Code Guide ⓘ

| Mar'15 | Mar'16 | Mar'17 | Mar'18 | Mar'19 | Mar'20 | Mar'21 | Mar'22 | Mar'23 | Mar'24 | TTM | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Return on Equity % ⓘ | 7.7 | 7 | 27.3 | 35.8 | 42 | 31.1 | 22.9 | 14.7 | 11.8 | 12.7 | 12.4 |

| Op. Profit Mgn % ⓘ | 8.6 | 7 | 10.4 | 15.3 | 15.1 | 17.5 | 17.4 | 11.9 | 13 | 13.3 | 13.1 |

| Net Profit Mgn % ⓘ | 2.2 | 1.9 | 6.7 | 9.8 | 8.9 | 10.7 | 11.2 | 6 | 6.1 | 6.8 | 6.9 |

| Debt to Equity ⓘ | 0.9 | 0.5 | 0.3 | 0.2 | 0 | 0.2 | 0 | 0 | 0.1 | 0.1 | - |

| Working Cap Days ⓘ | 153 | 132 | 107 | 109 | 107 | 140 | 163 | 134 | 166 | 189 | 82 |

| Cash Conv. Cycle ⓘ | 81 | 62 | 42 | 45 | 24 | 13 | 29 | 46 | 68 | 79 | 42 |

Sales growth is growing at healthy rate in last 3 years 37.16%

Net Profit is growing at healthy rate in last 3 years 13.76%

Sales growth is good in last 4 quarters at 12.30%

Return on Equity has declined versus last 3 years average to 12.40%

| Standalone | Consolidated | |

|---|---|---|

| TTM EPS (₹) | 19.6 | 24.6 |

| TTM Sales (₹ Cr.) | 1,319 | 1,973 |

| BVPS (₹.) ⓘ | 188.3 | 207.6 |

| Reserves (₹ Cr.) ⓘ | 1,032 | 1,138 |

| P/BV ⓘ | 3.33 | 3.02 |

| PE ⓘ | 31.98 | 25.51 |

| From the Market | |

|---|---|

| 52 Week Low / High (₹) | 568.05 / 966.00 |

| All Time Low / High (₹) | 536.10 / 1620.60 |

| Market Cap (₹ Cr.) | 3,471 |

| Equity (₹ Cr.) | 11.1 |

| Face Value (₹) | 2 |

| Industry PE ⓘ | 51.6 |

| Jun'24 | YoY Gr. Rt. % | Sep'24 | YoY Gr. Rt. % | Dec'24 | YoY Gr. Rt. % | Mar'25 | YoY Gr. Rt. % | |

|---|---|---|---|---|---|---|---|---|

| Operating Income | 0 | N/A | 0 | N/A | 0 | N/A | 0 | N/A |

| Adj EPS (₹) | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A |

| Net Profit Mgn % | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A |

| Pledged * | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

About the company

Rossari Biotech (Rossari) is a specialty-chemicals manufacturer which was established in 2003 as a partnership, between Mr. Edward Menezes and Mr. Sunil Chari. Rossari has built a strong base of more than 1000 customers across segments with the likes of Hindustan Unilever (Love & Care, Cif, Rin, Vim), Reliance (Enzo), Arvind, Raymond, Gokul Poultry Industries. Currently, they are distributing more than 4,250 products and delivering their services through 435 distributors in 28 states and 8 Union territories in India. Rossari also exports its products to more than 33 countries.

Rossari operates 8 manufacturing facilities at Silvassa and Dahej in Gujarat, with a total production capacity of 354,100 MTPA. It has leveraged its 4 strategically placed R&D facilities, including a cutting-edge certified laboratory at the Mumbai IIT campus, to drive growth through smart chemistry and research. The company's R&D strength lies in its ability to swiftly deliver customized and cost-effective product solutions, encompassing synthesis, formulation, development, and technical services.

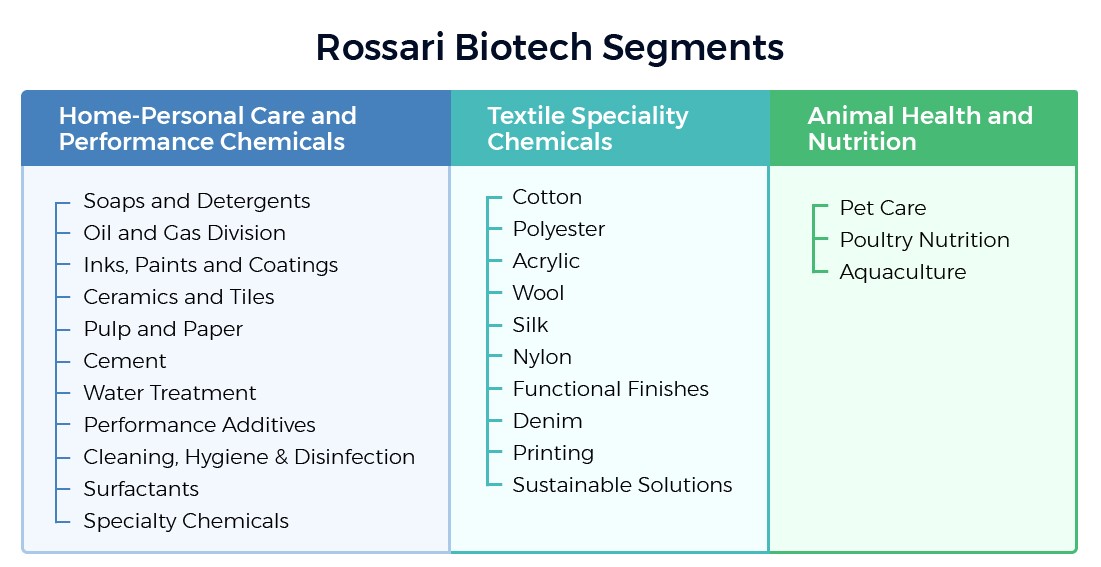

Rossari offers solutions in three main product categories:

Inorganic growth initiatives

Rossari Biotech successfully acquired and integrated three companies in last 2 years- Unitop Chemicals Pvt Ltd (33% FY23 revenue share), Tristar Intermediates Pvt Ltd (13% FY23 revenue share) and Romakk Chemicals Pvt Ltd (2% FY23 revenue share).The strategic acquisition of Unitop has helped Rossari diversify its product portfolio with its expansive product range in the agrochemicals, anti-foams, hand gels, viscosity modifiers, marine cleaners and Anti-Stats segments. Tristar has brought in significant synergy to Rossari in Pharmaceuticals, Textiles, Paints, Automotive and Agro-chemicals segments. The focus of the acquisitions will be on cross-selling products to existing customers and expanding into new areas of specialty chemicals.

In 2019, under the pet care segment, Rossari acquired a reputed Indian pet grooming brand - Lozalo International. The product range includes natural pet shampoos, powders, deodorants, sprays, creams, and floor washing liquid.

Competition

While competition is present across categories, Rossari has created a place for itself on back of a) partnering with customers for solutions, b) long standing relationships, c) expertise in select sub-segments.

Positives and triggers

Concern areas

Client concentration risk and short term contract: Reliance on a limited number of customers for the business may generally involve several risks. Notably, the company does not have any long term agreements with most of their customers, and the loss of one or more of them or a reduction in the demand for their products could adversely affect the business.

Raw Material Risk: Rossari’s largest expense is the cost of raw materials. Their primary raw materials are acrylic acid, surfactants and silicone oils which are subject to volatility due to factors beyond the company's control, such as market dynamics, economic conditions, and transportation and labor costs. The company does not have long-term agreements with suppliers, relying instead on purchaseorders, necessitating precise forecasting of supply and demand. Since product prices are typically fixed upon receiving a customer's purchase order, the company may not be able to fully transfer increased raw material costs to customers. But the same is done with some lag effect.

Financials

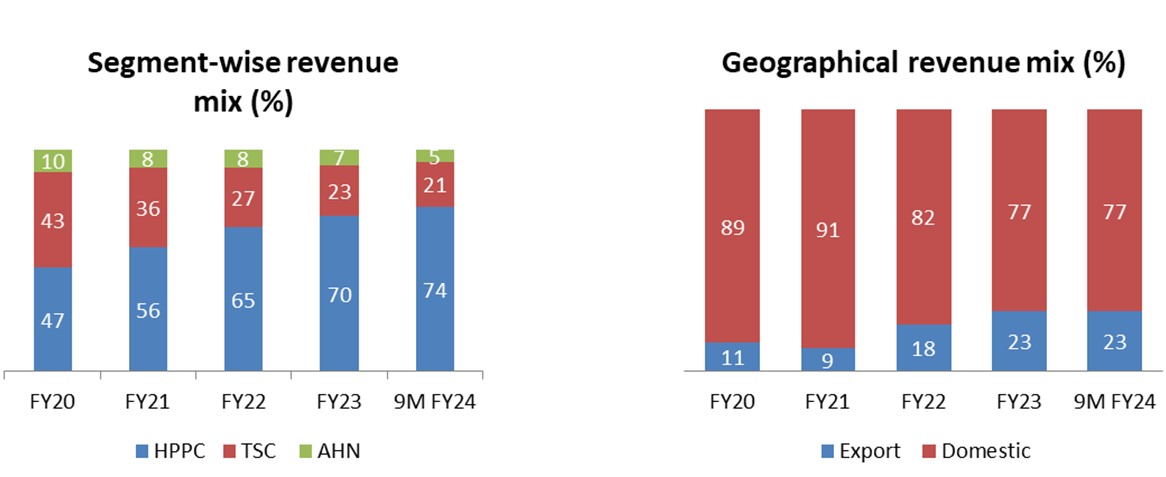

Revenues have more than tripled in the last 5 years from Rs.516 Cr. in FY19 to Rs.1656 Cr. in FY23 at a CAGR of 34%, majorly coming from the growth of HPPC segment. EBITDA has also shown consistent growth of 29% CAGR from FY19 to FY23. PAT has increased from Rs.46 Cr. in FY19 to Rs.107 Cr. in FY23 maintaining a moderate CAGR of 24% owing to increase in raw material costs. However, the raw material pressure has eased off over the last few quarters, which has led to an improvement in gross margins.

Management profile - Founders are technocrats with growth focus and clearly defined business roles.

Mr. Edward Menezes - He is the Executive Chairman and guides the company's technical, manufacturing, and marketing strategies. He has a B.Sc. in Textile Chemistry from University Department of Chemical Technology (UDCT) and master’s degree in marketing management from Prin. L. N. Welingkar Institute of Management Development and Research. His career spans over 34 years in textile processing.

Mr. Sunil Chari- He is the Managing Director and brings over three decades of expertise in textiles and related chemicals. He has a Bachelor's in Arts from Kakatiya University and a diploma in technical and applied chemistry from Victoria Jubilee Technical Institute. He is the cornerstone of Rossari's formidable sales and distribution network, driving market expansion and financial fortitude.

Moneyworks4me Opinion- Rossari has low debt to equity ratio, industry leading asset turnover, and an experienced management team with a great execution track record. It is also a proxy play on FMCG sector wherein branded companies are relatively expensive. Future outlook is strong on a) expansion coming into play, b) entering new industries and increasing target addressable market, c) stable raw material prices. Only short term hindrance looks like muted FMCG volume growth (esp. rural volumes). We value Rossari at Rs.700 (18x forward PE for FY26) and will wait for a better entry price given that current risk reward scenario is not lucrative.

| Company Name | CMP(₹) | |||||||

|---|---|---|---|---|---|---|---|---|

| Tata Chemicals | 812.4 | -36.9 (-4.3%) | Small Cap | 15,421 | -21.9 | 6.9 | - | 1 |

| GNFC | 492.1 | -12.4 (-2.5%) | Small Cap | 7,930 | 34.2 | 6.2 | 14.8 | 0.9 |

| Aarti Inds | 374 | -24.2 (-6.1%) | Small Cap | 6,372 | 10.1 | 6.6 | 39.3 | 2.6 |

| Atul | 5,400 | -225.4 (-4%) | Small Cap | 4,358 | 137.7 | 8.5 | 40.8 | 2.9 |

| Himadri Speciality | 434.3 | -22.4 (-4.9%) | Small Cap | 4,185 | 10.4 | 9.6 | 43.8 | 6.5 |

| Jubilant Ingrevia | 645.4 | -27.5 (-4.1%) | Small Cap | 3,987 | 12.8 | 4.2 | 52.4 | 4.5 |

| Chemplast Sanmar | 428.9 | -8 (-1.8%) | Small Cap | 3,923 | -5.5 | -3.8 | - | 38.5 |

| Guj. Alkalies & Chem | 627.1 | -33 (-5%) | Small Cap | 3,807 | -3.7 | -3.5 | - | 0.7 |

| GHCL | 610.5 | -11.3 (-1.8%) | Small Cap | 3,447 | 62.5 | 18 | 9.9 | 1.8 |

| India Glycols | 1,236.2 | -20.8 (-1.7%) | Small Cap | 3,291 | 54.2 | 4.9 | 23.2 | 2.1 |

| PARTICULARS | Mar'15 | Mar'16 | Mar'17 | Mar'18 | Mar'19 | Mar'20 | Mar'21 | Mar'22 | Mar'23 | Mar'24 |

|---|---|---|---|---|---|---|---|---|---|---|

| Sales | 171 | 179 | 233 | 292 | 516 | 600 | 709 | 1,483 | 1,656 | 1,831 |

| Operating Expenses ⓘ | 156 | 166 | 209 | 247 | 439 | 495 | 586 | 1,307 | 1,441 | 1,587 |

| Manufacturing Costs | 4 | 4 | 6 | 3 | 13 | 14 | 21 | 38 | 49 | 64 |

| Material Costs | 123 | 131 | 166 | 197 | 339 | 372 | 462 | 1,108 | 1,171 | 1,294 |

| Employee Cost | 11 | 12 | 14 | 20 | 28 | 37 | 42 | 68 | 99 | 103 |

| Other Costs ⓘ | 18 | 20 | 23 | 28 | 59 | 73 | 61 | 93 | 123 | 127 |

| Operating Profit ⓘ | 15 | 13 | 24 | 45 | 78 | 105 | 123 | 176 | 215 | 243 |

| Operating Profit Margin (%) | 8.5% | 7.0% | 10.4% | 15.3% | 15.0% | 17.5% | 17.3% | 11.9% | 13.0% | 13.3% |

| Other Income ⓘ | 0 | 0 | 1 | 1 | 1 | 4 | 9 | 19 | 14 | 14 |

| Interest ⓘ | 5 | 4 | 2 | 1 | 3 | 4 | 3 | 13 | 22 | 19 |

| Depreciation ⓘ | 5 | 5 | 4 | 5 | 12 | 17 | 23 | 48 | 63 | 60 |

| Exceptional Items ⓘ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Profit Before Tax ⓘ | 5 | 5 | 19 | 40 | 63 | 88 | 107 | 136 | 144 | 178 |

| Tax ⓘ | 1 | 1 | 3 | 11 | 18 | 23 | 27 | 39 | 37 | 47 |

| Profit After Tax | 4 | 3 | 16 | 29 | 46 | 65 | 80 | 98 | 107 | 131 |

| PAT Margin (%) | 2.2% | 1.9% | 6.7% | 9.9% | 8.8% | 10.9% | 11.3% | 6.6% | 6.5% | 7.1% |

| Adjusted EPS (₹) | 0.8 | 0.7 | 3.3 | 6.0 | 9.4 | 12.9 | 15.5 | 17.7 | 19.5 | 23.7 |

| Dividend Payout Ratio (%) | 6% | 0% | 0% | 30% | 5% | 4% | 3% | 3% | 3% | 2% |

| PARTICULARS | Mar'15 | Mar'16 | Mar'17 | Mar'18 | Mar'19 | Mar'20 | Mar'21 | Mar'22 | Mar'23 | Mar'24 |

|---|---|---|---|---|---|---|---|---|---|---|

Equity and Liabilities | ||||||||||

| Shareholders Fund | 47 | 50 | 65 | 94 | 124 | 286 | 407 | 802 | 912 | 1,044 |

| Share Capital ⓘ | 4 | 4 | 4 | 4 | 4 | 10 | 10 | 11 | 11 | 11 |

| Reserves ⓘ | 42 | 46 | 61 | 90 | 119 | 276 | 396 | 791 | 901 | 1,033 |

| Minority Interest | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Debt | 39 | 22 | 22 | 20 | 4 | 61 | 0 | 0 | 64 | 96 |

| Long Term Debt | 9 | 7 | 2 | 1 | 1 | 34 | 0 | 0 | 35 | 33 |

| Short Term Debt | 30 | 15 | 20 | 19 | 3 | 27 | 0 | 0 | 29 | 63 |

| Trade Payables | 18 | 28 | 32 | 40 | 106 | 97 | 131 | 186 | 181 | 219 |

| Others Liabilities ⓘ | 10 | 8 | 5 | 11 | 49 | 80 | 107 | 429 | 415 | 465 |

| Total Liabilities ⓘ | 114 | 109 | 124 | 166 | 283 | 525 | 645 | 1,417 | 1,572 | 1,825 |

Fixed Assets | ||||||||||

| Gross Block | 67 | 38 | 76 | 88 | 86 | 122 | 234 | 704 | 743 | 791 |

| Accumulated Depreciation | 30 | 0 | 38 | 43 | 12 | 29 | 53 | 97 | 158 | 213 |

| Net Fixed Assetsⓘ | 38 | 38 | 38 | 45 | 74 | 94 | 181 | 607 | 585 | 578 |

| CWIP ⓘ | 7 | 8 | 8 | 10 | 3 | 22 | 0 | 1 | 16 | 47 |

| Investmentsⓘ | 0 | 0 | 0 | 7 | 0 | 18 | 0 | 36 | 51 | 63 |

| Inventories | 31 | 25 | 24 | 35 | 55 | 58 | 95 | 190 | 188 | 282 |

| Trade Receivables | 30 | 31 | 47 | 60 | 86 | 94 | 144 | 305 | 354 | 425 |

| Cash Equivalents | 1 | 3 | 2 | 1 | 6 | 127 | 88 | 52 | 124 | 30 |

| Others Assetsⓘ | 7 | 5 | 5 | 8 | 59 | 112 | 135 | 225 | 253 | 399 |

| Total Assets ⓘ | 114 | 109 | 124 | 166 | 283 | 525 | 645 | 1,417 | 1,572 | 1,825 |

| PARTICULARS | Mar'15 | Mar'16 | Mar'17 | Mar'18 | Mar'19 | Mar'20 | Mar'21 | Mar'22 | Mar'23 | Mar'24 |

|---|---|---|---|---|---|---|---|---|---|---|

| Cash Flow From Operating Activity ⓘ | 8 | 26 | 7 | 24 | 71 | 57 | 48 | 29 | 152 | 43 |

| PBT ⓘ | 5 | 5 | 19 | 40 | 63 | 88 | 107 | 136 | 144 | 178 |

| Adjustment ⓘ | 9 | 7 | 6 | 6 | 17 | 20 | 21 | 55 | 83 | 76 |

| Changes in Working Capital ⓘ | -5 | 13 | -14 | -11 | 11 | -31 | -48 | -112 | -28 | -157 |

| Tax Paid ⓘ | -1 | -1 | -3 | -11 | -20 | -20 | -31 | -50 | -48 | -54 |

| Cash Flow From Investing Activity ⓘ | -2 | -5 | -6 | -20 | -36 | -190 | -37 | -299 | -181 | -103 |

| Capex | -2 | -5 | -6 | -14 | -44 | -76 | -56 | -36 | -31 | -126 |

| Net Investments | 0 | 0 | 0 | 0 | 7 | -18 | 14 | -6 | -14 | -9 |

| Others ⓘ | 0 | 0 | 0 | -7 | 1 | -96 | 5 | -257 | -136 | 32 |

| Cash Flow From Financing Activityⓘ | -6 | -19 | -2 | -5 | -29 | 157 | -25 | 292 | 61 | 16 |

| Net Proceeds from Shares ⓘ | 0 | 0 | 0 | 0 | 0 | 100 | 43 | 302 | 4 | 4 |

| Net Proceeds from Borrowing ⓘ | 0 | 0 | 0 | 0 | -1 | 39 | -34 | 0 | 45 | -12 |

| Interest Paid ⓘ | -5 | -3 | -2 | -1 | -2 | -3 | -4 | -2 | -6 | -16 |

| Dividend Paid ⓘ | 0 | 0 | 0 | 0 | -11 | -3 | -3 | -3 | -3 | -3 |

| Others ⓘ | -2 | -17 | 0 | -4 | -16 | 24 | -27 | -5 | 21 | 43 |

| Net Cash Flow ⓘ | 0 | 2 | 0 | -2 | 6 | 23 | -14 | 22 | 32 | -44 |

| PARTICULARS | Mar'15 | Mar'16 | Mar'17 | Mar'18 | Mar'19 | Mar'20 | Mar'21 | Mar'22 | Mar'23 | Mar'24 |

|---|---|---|---|---|---|---|---|---|---|---|

| Ratios | ||||||||||

| ROE (%) | 8.18 | 6.99 | 27.27 | 36.33 | 41.88 | 31.83 | 23.11 | 16.17 | 12.52 | 13.36 |

| ROCE (%) | 10.7 | 10.3 | 26.4 | 40.37 | 54.4 | 37.93 | 28.81 | 24.37 | 18.48 | 18.39 |

| Asset Turnover Ratio | 1.43 | 1.6 | 2 | 2.06 | 2.3 | 1.49 | 1.22 | 1.45 | 1.11 | 1.08 |

| PAT to CFO Conversion(x) | 2 | 8.67 | 0.44 | 0.83 | 1.54 | 0.88 | 0.6 | 0.3 | 1.42 | 0.33 |

| Working Capital Days | ||||||||||

| Receivable Days | 62 | 62 | 61 | 66 | 51 | 54 | 61 | 55 | 72 | 77 |

| Inventory Days | 78 | 58 | 38 | 36 | 32 | 34 | 39 | 35 | 42 | 47 |

| Payable Days | 68 | 65 | 66 | 67 | 79 | 100 | 90 | 52 | 57 | 56 |

The company was initially incorporated as Rossari Labtech on March 6, 2003, as a partnership firm under the Indian Partnership Act, 1932, pursuant to a certificate of registration dated June 22, 2003, issued by the Registrar of Firms, Mumbai. The name of the partnership firm was changed to Rossari Biotech on December 5, 2003 and further the firm converted into a joint stock company on August 10, 2009, under part IX of the Companies Act, 1956 as Rossari Biotech Limited with a certificate of incorporation granted by the Registrar of Companies, Maharashtra at Mumbai (RoC). The company received its certificate of commencement of business on August 13, 2009.

Business area of the company

The company is one of the leading specialty chemicals manufacturing companies in India providing customized solutions to specific industrial and production requirements of its customers primarily in the FMCG, apparel, poultry and animal feed industries through its diversified product portfolio comprising home, personal care and performance chemicals; textile specialty chemicals; and animal health and nutrition products. The company’s business is organized in three main product categories - (i) home, personal care and performance chemicals; (ii) textile specialty chemicals; and (iii) animal health and nutrition products.

The company is the leading manufacturer of acrylic polymers in India and manufactures many products for its customers in the soaps and detergent, paints, inks and coatings, ceramics and tiles, water treatment chemicals and pulp and paper industries. It also manufacture institutional cleaning chemical formulations for hospitality, facility management, airports, corporates, food service, commercial laundry, malls, multiplexes, educational sector, places of worship etc. It is in advanced stages of expanding its home, personal care and performance product portfolio to water treatment formulations, specialty formulation for breweries as well as dairies. Besides, the company provides specialty chemicals for the entire value-chain of the textile industry starting from fiber, yarn to fabric, wet processing and garment processing. The company has also diversified into animal health and nutrition and currently supply poultry feed supplements and additives, pet grooming and pet treats including for weaning, infants and adult pets.

Major Events & Milestones:

Awards & accreditations:

MoneyWorks4Me rating and ranking of funds for SIP is available to subscribers only. Moneyworks4Me is not a rating and ranking agency, however it is required that users have a way of selecting funds and building a Portfolio. The method used by it are described below to enable users to understand the logic behind the rating and ranking Subscriber will find more details on this in the various content made available from time to time. In case you need more please write to besafe@moneyworks4Me.com

MoneyWorks4Me rates and ranks mutual funds based on the following data-driven system:

Funds ranking in screeners: Performance Consistency and Quality are two parameters used for ranking funds for SIP. The ranking as follows GG, GO, GR, OG, OO, OR, RG, RO and RR.

With the same color-coded funds, the one with the higher Average 3-year rolling returns (over 5 to 10 years), the number that appears in the Performance tag, ranks higher.

Here is the summary:

The third tag Upside Potential is not relevant for SIP. It is relevant for lumpsum investments in Mutual Funds.

Make an informed decision for Stocks

Invest using an intelligent system with powerful data-driven tools that help you identify opportunities and make informed buy-hold-sell decisions

Buy quality Stocks when they are available at reasonable prices and supported by an upward price trend and Sell when they are Overvalued using the Decizen Rating System. Covers 3500+ stocks

Account Discovery

- OTP from CAMS

Account Linking for Stocks & MF

- One OTP per link Eg. NSDL, CDSL, CAMS, KFin etc.

One Click Upload for your Current Portfolio and Future Transactions!

Don't miss out! First 10 users today get it FREE

With this 4 hrs Masterclass, you’ll be able to:

Download APP

Download APP