Invest in the best stock opportunities right now and every-time.

Start Systematic Stock Investing ...in less than a minute.

Past 10 year's financial track record analysis by Moneyworks4me indicates that Nocil Ltd is a average quality company.

The key valuation ratios of Nocil Ltd's currently when compared to its past seem to suggest it is in the Somewhat Undervalued zone.

The Price Trend analysis by MoneyWorks4Me indicates it is Weak which suggest that the price of Nocil Ltd is likely to Fall in the short term. However, please check the rating on Quality and Valuation before investing.

Data adjusted to bonus, split, extra-ordinary income, rights issue and change in financial year end.

Value Creation Index Colour Code Guide ⓘ

| Mar'15 | Mar'16 | Mar'17 | Mar'18 | Mar'19 | Mar'20 | Mar'21 | Mar'22 | Mar'23 | Mar'24 | TTM | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| ROCE % ⓘ | 18.7% | 24% | 20.8% | 25.9% | 25.1% | 13.1% | 8.8% | 17.7% | 13.6% | 11.2% | - |

| Value Creation Index ⓘ | 0.3 | 0.7 | 0.5 | 0.9 | 0.8 | -0.1 | -0.4 | 0.3 | 0.0 | -0.2 | - |

Growth Parameters ⓘGrowth Parameters Colour Code Guide ⓘ | |||||||||||

| Sales ⓘ | 719 | 715 | 742 | 968 | 1,043 | 846 | 925 | 1,571 | 1,617 | 1,445 | 1,410 |

| Sales YoY Gr. | - | -0.5% | 3.8% | 30.4% | 7.8% | -18.9% | 9.3% | 69.9% | 2.9% | -10.6% | - |

| Adj EPS ⓘ | 3.6 | 4.9 | 5.9 | 10.4 | 11.4 | 7.8 | 5.4 | 10.6 | 9 | 7.2 | 7.4 |

| YoY Gr. | - | 35% | 21% | 75.9% | 8.9% | -31.1% | -31.7% | 98.3% | -15.2% | -20.4% | - |

| BVPS (₹) ⓘ | 25.8 | 29.2 | 55.7 | 63.4 | 70.1 | 71.2 | 77 | 86.5 | 92.8 | 101.5 | 106.8 |

| Adj Net Profit ⓘ | 58.3 | 78.8 | 97 | 172 | 188 | 130 | 88.9 | 177 | 150 | 119 | 124 |

| Cash Flow from Ops. ⓘ | 30.1 | 170 | 142 | 102 | 164 | 179 | 93.6 | -30.2 | 282 | 201 | - |

| Debt/CF from Ops. ⓘ | 5 | 0.2 | 0.1 | 0.1 | 0 | 0 | 0 | 0 | 0 | 0 | - |

CAGR Colour Code Guide ⓘ

| 9 Years | 5 Years | 3 Years | 1 Years | |||||

|---|---|---|---|---|---|---|---|---|

| Sales ⓘ | 8.1% | 6.7% | 16% | -10.6% | ||||

| Adj EPS ⓘ | 7.8% | -8.8% | 10.2% | -20.4% | ||||

| BVPSⓘ | 16.4% | 7.7% | 9.7% | 9.4% | ||||

| Share Price | 15.7% | 21.5% | -11.4% | -38.2% | ||||

Performance Ratio Colour Code Guide ⓘ

| Mar'15 | Mar'16 | Mar'17 | Mar'18 | Mar'19 | Mar'20 | Mar'21 | Mar'22 | Mar'23 | Mar'24 | TTM | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Return on Equity % ⓘ | 14.7 | 17.8 | 14 | 17.5 | 17 | 11 | 7.2 | 12.9 | 10 | 7.3 | 7.1 |

| Op. Profit Mgn % ⓘ | 16 | 19.6 | 21.5 | 27.8 | 28.5 | 21.1 | 14.2 | 18.3 | 15.7 | 13.5 | 10.5 |

| Net Profit Mgn % ⓘ | 8.1 | 11 | 13.1 | 17.7 | 18 | 15.3 | 9.6 | 11.2 | 9.3 | 8.3 | 8.8 |

| Debt to Equity ⓘ | 0.4 | 0.1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | - |

| Working Cap Days ⓘ | 194 | 201 | 161 | 141 | 163 | 195 | 188 | 160 | 173 | 167 | 123 |

| Cash Conv. Cycle ⓘ | 110 | 103 | 84 | 92 | 107 | 118 | 113 | 110 | 126 | 123 | 102 |

Sales growth is growing at healthy rate in last 3 years 16.04%

Net Profit is growing at healthy rate in last 3 years 10.20%

Return on Equity has declined versus last 3 years average to 7.10%

Sales growth is not so good in last 4 quarters at -4.66%

| Standalone | Consolidated | |

|---|---|---|

| TTM EPS (₹) | 7.7 | 7.4 |

| TTM Sales (₹ Cr.) | 1,410 | 1,410 |

| BVPS (₹.) ⓘ | 106.3 | 106.8 |

| Reserves (₹ Cr.) ⓘ | 1,609 | 1,617 |

| P/BV ⓘ | 1.73 | 1.72 |

| PE ⓘ | 23.90 | 24.81 |

| From the Market | |

|---|---|

| 52 Week Low / High (₹) | 163.15 / 336.10 |

| All Time Low / High (₹) | 4.90 / 3500.00 |

| Market Cap (₹ Cr.) | 3,067 |

| Equity (₹ Cr.) | 167 |

| Face Value (₹) | 10 |

| Industry PE ⓘ | 51.6 |

| Mar'24 | YoY Gr. Rt. % | Jun'24 | YoY Gr. Rt. % | Sep'24 | YoY Gr. Rt. % | Dec'24 | YoY Gr. Rt. % | |

|---|---|---|---|---|---|---|---|---|

| Operating Income | 0.2 | -35.3 | 0.2 | -8.3 | 0.2 | -4.2 | 0.1 | -65.2 |

| Adj EPS (₹) | 0.00 | -100 | 0.01 | 0 | 0.05 | N/A | -0.02 | -300 |

| Net Profit Mgn % | -4.91 | -2693 bps | 14.67 | 497 bps | 60.09 | 9836 bps | -89.29 | -10524 bps |

Particulars | Q2FY24 (Rs. Crs) | YoY Trend | Comments |

| Revenue | 351 | -10% | Revenues hit as realization declined sharply albeit volumes grew |

| EBITDA | 45 | -27% | |

| EBITDA Margin | 13% | - 300bps | Negative operating leverage |

| PAT | 27 | -24% |

Muted results on recessionary pressure in export market, domestic volumes were flat QoQ.

|

Particulars |

Q1FY24 |

YoY Trend |

Comments |

|

Revenue |

397 |

-22% |

High base quarter effect; flat QoQ |

|

EBITDA |

55 |

-46% |

|

|

EBITDA Margin |

14% |

-638 bps |

Decline YoY due to negative operating leverage; margin flat QoQ |

|

PAT |

34 |

-48% |

|

Poor quarterly performance on pricing pressure due to Chinese exports and global recessionary environment.

Market Cap = INR 3,758 cr

CMP = Rs 226

P/E = 18.7 X TTM

|

Results |

INR Crore |

YoY Growth |

Comments |

|

Revenue |

389 |

4.85% |

Sales volume impacted due to global recession as exports constitute a major chunk of revenues. |

|

EBITDA |

62 |

21.57% |

EBITDA growth in double digits due to low base in the previous year due to COVID led restrictions |

Key Highlights:-

Management Outlook:-

NOCIL | Market Cap: 3360 Cr

CMP Rs. 202 | P/E 17x FY23;

Recommendation | Hold

Results: NOCIL reported 51% growth in sales and 37% growth in operating profit year on year. For the entire year, sales growth was 9% while volume growth was 14%.

Key highlights:

Outlook: As per the management, the competition is high but demand recovery is very strong. While the realization were lower, the growth in volume compensated for the same. NOCIL is experiencing good growth from customers as they look to diversify away from Chinese supply. China is the largest producer of rubber chemicals, small loss of market share by China can help non-Chinese players to gain market share. This bodes well for growth. The management expects full utilization of capacities by mid FY24.

MoneyWorks4me Opinion: We had recommended BUY on NOCIL at 145/share. We expect bright prospects for NOCIL from capacity addition, demand from customers as they look to diversify away from China, recovery in auto sector, etc. Attractive business prospects and reasonable valuation made us recommend a BUY. Valuations are not excessive but certainly do not offer margin of safety for fresh buy.

NOCIL Ltd | Market Cap Rs 2400 Cr

CMP 143 | PE 16x FY22

Recommendation | BUY

About the company

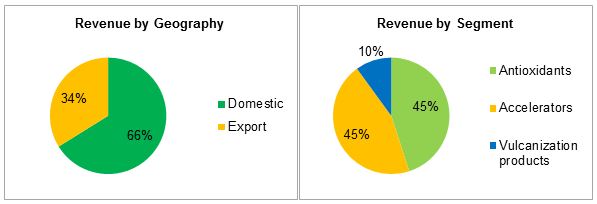

NOCIL –Arvind Mafatlal Company –is Rs. 1000 Cr rubber chemicals manufacturer. The company’s products find application used in both tyre and non-tyre industries (latex industry, footwear and other auto-ancillary products). The bulk (~65%) of rubber chemicals are sold to the tyre industry, domestic and international.

Industry: The Indian tyre industry size is estimated at ~Rs. 60,000 Cr (as of FY18); with demand largely coming from two segments i.e. original equipment manufacturers (OEM ~35-40% of demand) and replacement market (aftermarket ~60-65%).

Chemicals manufactured by the company are essential in the production of rubber and rubber-related products. As a thumb rule rubber chemical constitutes about 3.5% to 4% of the total rubber consumption. Its growth is dependent on increase in usage of rubber.

The company manufactures intermediates as well as a wide range of final products across two manufacturing facilities in Navi Mumbai and Dahej.

Company products include: –

Management

NOCIL is the flagship company of the Arvind Mafatlal group. As of June 2020, the promoters held ~34% stake in the company and the remaining stake was held by public and other institutions. Mafatlal Industries, Navin Flourine and Mafatlal Denim are its sister companies.

Business of NOCIL

NOCIL has a leading market position in the rubber chemicals industry in India (with ~40% market share) and has an established clientele. The company primarily manufactures 4 categories of products namely, Accelerators, Anti-degradants/anti-oxidants, Pre-vulcanisation inhibitors and Post-vulcanisation stabilisers. Dominant portion of the revenues of the company comes from India.

NOCIL is among the few players globally with a wide product basket of 22 rubber chemicals. Furthermore, it has been able to maintain healthy relationships with major domestic and global tyre manufacturers for over 40 years, and hence has a good international presence.

Driven by strong R&D capabilities, the company has developed a process for producing a key intermediate, and has also set up and stabilised a green field production facility in Dahej.

NOCIL competes with Chinese rubber chemical manufacturers who have high scale and cost advantage. However, with recent operational efficiency improvement NOCIL has been able to improve its cost structure. The business is very competitive and NOCIL commands market share of 10% globally.

Financials

NOCIL sales has more than doubled from 2011 to 2019 and fell 20% in FY20 due to slowdown in auto industry. It clocked 14.3% CAGR in earnings growth in last 10 years.

The company has seen decline in its operating margins lately owing to de-growth in the auto sector. NOCIL exhibits cyclicality from auto sector as well as competitive environment.

In recent past, operating margins came off due to cessation of anti-dumping duty (ADD) from August 2019. The anti-dumping duty was present on 6 (out of 22) of its products contributing 50% to overall revenues (as of FY19).

Click here to view complete financials of NOCIL

NOCIL is debt-free despite of regularly increasing its capacity since 2013. The fixed asset of the company has grown ~5.6x in last 10 years. Recently it completed its ongoing capacity expansion programme (of Rs 450 crore), it will fully capitalised by financial year end. No major capex is expected over the medium term. This will lead to higher dividend payout ratio in medium term.

Future Prospects

Positive triggers

Risks

Valuation

At current sales expectation of Rs. 850 Cr, it trades at 14x EV/EBITDA and 20x P/E ratio.

Assuming 2x asset turnover in new capacities, it can earn around additional sales of Rs. 400 Cr over next 2 years. With expectation of atleast 12% CAGR in sales and 18% in operating margin, implied P/E ratio is 16x FY22. We have assumed operating margins of 18% instead of 22-26% in recent past due to absence of anti-dumping duty.

We recommend BUY in the range of 140-150/share which implies 10-15% CAGR over next 3 years.

While the future potential is large, the execution, competition and regulation can lead to lower than expected performance and hence disappointment. If we find such risks that outweigh future prospects, we will recommend to exit NOCIL even at a small loss.

Note for Booster Stocks: These stocks are more volatile that large cap stocks. They are recommended to enhance your portfolio returns. Should any new information lead us to conclude that the recommended stock may not deliver as per expectations; we will recommend you to sell it. You are expected to act/exit even at a loss. You need to think portfolio returns and not individual stocks.

| Company Name | CMP(₹) | |||||||

|---|---|---|---|---|---|---|---|---|

| Tata Chemicals | 812.2 | -37.1 (-4.4%) | Small Cap | 15,421 | -21.9 | 6.9 | - | 1 |

| GNFC | 489.9 | -14.7 (-2.9%) | Small Cap | 7,930 | 34.2 | 6.2 | 14.8 | 0.9 |

| Aarti Inds | 373.7 | -24.5 (-6.1%) | Small Cap | 6,372 | 10.1 | 6.6 | 39.3 | 2.6 |

| Atul | 5,367.6 | -257.8 (-4.6%) | Small Cap | 4,358 | 137.7 | 8.5 | 40.8 | 2.9 |

| Himadri Speciality | 433.9 | -22.7 (-5%) | Small Cap | 4,185 | 10.4 | 9.6 | 43.8 | 6.5 |

| Jubilant Ingrevia | 645.4 | -27.5 (-4.1%) | Small Cap | 3,987 | 12.8 | 4.2 | 52.4 | 4.5 |

| Chemplast Sanmar | 428.9 | -8 (-1.8%) | Small Cap | 3,923 | -5.5 | -3.8 | - | 38.5 |

| Guj. Alkalies & Chem | 624.5 | -35.6 (-5.4%) | Small Cap | 3,807 | -3.7 | -3.5 | - | 0.7 |

| GHCL | 611.7 | -10.1 (-1.6%) | Small Cap | 3,447 | 62.5 | 18 | 9.9 | 1.8 |

| India Glycols | 1,217.4 | -39.6 (-3.2%) | Small Cap | 3,291 | 54.2 | 4.9 | 23.2 | 2.1 |

| PARTICULARS | Mar'15 | Mar'16 | Mar'17 | Mar'18 | Mar'19 | Mar'20 | Mar'21 | Mar'22 | Mar'23 | Mar'24 |

|---|---|---|---|---|---|---|---|---|---|---|

| Sales | 719 | 715 | 742 | 968 | 1,043 | 846 | 925 | 1,571 | 1,617 | 1,445 |

| Operating Expenses ⓘ | 606 | 576 | 583 | 702 | 750 | 668 | 794 | 1,285 | 1,364 | 1,250 |

| Manufacturing Costs | 110 | 100 | 99 | 120 | 135 | 129 | 137 | 228 | 273 | 234 |

| Material Costs | 389 | 360 | 360 | 441 | 467 | 388 | 505 | 859 | 888 | 815 |

| Employee Cost | 50 | 61 | 64 | 71 | 71 | 77 | 70 | 81 | 87 | 92 |

| Other Costs ⓘ | 57 | 56 | 61 | 70 | 78 | 74 | 82 | 117 | 116 | 108 |

| Operating Profit ⓘ | 113 | 139 | 159 | 265 | 293 | 178 | 131 | 286 | 253 | 195 |

| Operating Profit Margin (%) | 15.8% | 19.5% | 21.5% | 27.4% | 28.1% | 21.1% | 14.1% | 18.2% | 15.6% | 13.5% |

| Other Income ⓘ | 4 | 4 | 10 | 15 | 10 | 9 | 15 | 4 | 6 | 39 |

| Interest ⓘ | 17 | 9 | 2 | 1 | 1 | 1 | 1 | 1 | 1 | 2 |

| Depreciation ⓘ | 14 | 15 | 20 | 24 | 24 | 34 | 37 | 48 | 56 | 53 |

| Exceptional Items ⓘ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Profit Before Tax ⓘ | 86 | 119 | 147 | 255 | 278 | 152 | 107 | 241 | 202 | 180 |

| Tax ⓘ | 29 | 41 | 50 | 85 | 93 | 22 | 19 | 65 | 53 | 47 |

| Profit After Tax | 57 | 78 | 97 | 170 | 185 | 131 | 88 | 176 | 149 | 133 |

| PAT Margin (%) | 7.9% | 10.9% | 13.1% | 17.6% | 17.7% | 15.4% | 9.6% | 11.2% | 9.2% | 9.2% |

| Adjusted EPS (₹) | 3.6 | 4.9 | 5.9 | 10.3 | 11.2 | 7.9 | 5.3 | 10.6 | 9.0 | 8.0 |

| Dividend Payout Ratio (%) | 28% | 25% | 30% | 24% | 22% | 32% | 38% | 28% | 34% | 38% |

| PARTICULARS | Mar'15 | Mar'16 | Mar'17 | Mar'18 | Mar'19 | Mar'20 | Mar'21 | Mar'22 | Mar'23 | Mar'24 |

|---|---|---|---|---|---|---|---|---|---|---|

Equity and Liabilities | ||||||||||

| Shareholders Fund | 415 | 470 | 910 | 1,043 | 1,159 | 1,179 | 1,279 | 1,440 | 1,546 | 1,692 |

| Share Capital ⓘ | 161 | 161 | 164 | 164 | 165 | 166 | 166 | 167 | 167 | 167 |

| Reserves ⓘ | 254 | 309 | 747 | 879 | 993 | 1,014 | 1,113 | 1,274 | 1,380 | 1,525 |

| Minority Interest | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Debt | 126 | 16 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Long Term Debt | 51 | 15 | 5 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Short Term Debt | 75 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Trade Payables | 84 | 73 | 81 | 116 | 98 | 89 | 170 | 215 | 127 | 118 |

| Others Liabilities ⓘ | 181 | 200 | 164 | 172 | 185 | 173 | 165 | 175 | 183 | 205 |

| Total Liabilities ⓘ | 806 | 759 | 1,161 | 1,331 | 1,442 | 1,442 | 1,615 | 1,831 | 1,857 | 2,015 |

Fixed Assets | ||||||||||

| Gross Block | 451 | 459 | 708 | 701 | 854 | 1,028 | 1,183 | 1,221 | 1,253 | 1,282 |

| Accumulated Depreciation | 140 | 153 | 166 | 174 | 197 | 231 | 266 | 312 | 365 | 413 |

| Net Fixed Assetsⓘ | 311 | 307 | 542 | 527 | 657 | 797 | 917 | 909 | 887 | 869 |

| CWIP ⓘ | 3 | 6 | 4 | 42 | 131 | 156 | 14 | 8 | 9 | 16 |

| Investmentsⓘ | 22 | 22 | 176 | 281 | 130 | 54 | 68 | 53 | 218 | 399 |

| Inventories | 188 | 133 | 115 | 155 | 171 | 136 | 166 | 333 | 285 | 223 |

| Trade Receivables | 167 | 151 | 167 | 243 | 232 | 203 | 309 | 450 | 346 | 340 |

| Cash Equivalents | 8 | 15 | 122 | 32 | 40 | 14 | 80 | 16 | 57 | 96 |

| Others Assetsⓘ | 107 | 124 | 35 | 50 | 82 | 81 | 60 | 61 | 54 | 72 |

| Total Assets ⓘ | 806 | 759 | 1,161 | 1,331 | 1,442 | 1,442 | 1,615 | 1,831 | 1,857 | 2,015 |

| PARTICULARS | Mar'15 | Mar'16 | Mar'17 | Mar'18 | Mar'19 | Mar'20 | Mar'21 | Mar'22 | Mar'23 | Mar'24 |

|---|---|---|---|---|---|---|---|---|---|---|

| Cash Flow From Operating Activity ⓘ | 30 | 170 | 142 | 102 | 164 | 179 | 94 | -30 | 282 | 201 |

| PBT ⓘ | 86 | 119 | 147 | 255 | 278 | 152 | 107 | 241 | 202 | 180 |

| Adjustment ⓘ | 29 | 20 | 13 | 17 | 16 | 26 | 25 | 45 | 51 | 13 |

| Changes in Working Capital ⓘ | -66 | 62 | 28 | -88 | -42 | 52 | -38 | -256 | 80 | 48 |

| Tax Paid ⓘ | -19 | -31 | -46 | -81 | -88 | -51 | 0 | -60 | -51 | -40 |

| Cash Flow From Investing Activity ⓘ | -5 | -12 | -10 | -142 | -101 | -106 | -62 | 31 | -217 | -77 |

| Capex | -9 | -14 | -13 | -47 | -237 | -180 | -27 | -36 | -29 | -17 |

| Net Investments | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Others ⓘ | 3 | 2 | 3 | -94 | 136 | 73 | -36 | 67 | -187 | -60 |

| Cash Flow From Financing Activityⓘ | -33 | -151 | -31 | -43 | -50 | -101 | 0 | -34 | -54 | -55 |

| Net Proceeds from Shares ⓘ | 0 | 0 | 6 | 4 | 5 | 1 | 4 | 3 | 1 | 0 |

| Net Proceeds from Borrowing ⓘ | -21 | -47 | -11 | -10 | -5 | 0 | 0 | 0 | 0 | 0 |

| Interest Paid ⓘ | -17 | -10 | -2 | -1 | -1 | -1 | -1 | -1 | -1 | -2 |

| Dividend Paid ⓘ | -10 | -16 | -23 | -35 | -50 | -98 | -1 | -33 | -50 | -50 |

| Others ⓘ | 15 | -78 | 0 | 0 | 0 | -2 | -2 | -2 | -4 | -4 |

| Net Cash Flow ⓘ | -8 | 7 | 102 | -82 | 13 | -28 | 32 | -33 | 11 | 68 |

| PARTICULARS | Mar'15 | Mar'16 | Mar'17 | Mar'18 | Mar'19 | Mar'20 | Mar'21 | Mar'22 | Mar'23 | Mar'24 |

|---|---|---|---|---|---|---|---|---|---|---|

| Ratios | ||||||||||

| ROE (%) | 14.41 | 17.69 | 14.07 | 17.4 | 16.79 | 11.18 | 7.19 | 12.95 | 9.99 | 8.21 |

| ROCE (%) | 18.74 | 24.04 | 20.84 | 25.85 | 25.14 | 13.09 | 8.75 | 17.71 | 13.56 | 11.17 |

| Asset Turnover Ratio | 1.02 | 1.01 | 0.85 | 0.79 | 0.75 | 0.59 | 0.6 | 0.91 | 0.88 | 0.75 |

| PAT to CFO Conversion(x) | 0.53 | 2.18 | 1.46 | 0.6 | 0.89 | 1.37 | 1.07 | -0.17 | 1.89 | 1.51 |

| Working Capital Days | ||||||||||

| Receivable Days | 73 | 74 | 71 | 76 | 83 | 94 | 101 | 88 | 90 | 87 |

| Inventory Days | 81 | 74 | 55 | 50 | 57 | 66 | 60 | 58 | 70 | 64 |

| Payable Days | 72 | 65 | 62 | 53 | 54 | 71 | 72 | 58 | 53 | 42 |

NOCIL Limited (formerly known as National Organic Chemical Industries) is a limited company incorporated on May 11, 1961, and is engaged in manufacture of rubber chemicals domiciled in India. The Company has manufacturing facilities at Navi Mumbai (Maharashtra) and at Dahej (Gujarat). The products manufactured by the Company are used by the tyre industry and other rubber processing industries.

Business area of the company

NOCIL’s involvement in the Rubber chemicals business spans over 4 decades. The company is one of the few players in this business to offer wide range of rubber chemicals to suit the customer needs. Due to rich experience and offering a one stop shop to customers, NOCIL is today acknowledged as a dependable supplier of rubber chemicals. NOCIL today is the Largest Rubber Chemicals Manufacturer in India with the State of the Art Technology for the manufacture of rubber chemicals.

Products

Certifications

MoneyWorks4Me rating and ranking of funds for SIP is available to subscribers only. Moneyworks4Me is not a rating and ranking agency, however it is required that users have a way of selecting funds and building a Portfolio. The method used by it are described below to enable users to understand the logic behind the rating and ranking Subscriber will find more details on this in the various content made available from time to time. In case you need more please write to besafe@moneyworks4Me.com

MoneyWorks4Me rates and ranks mutual funds based on the following data-driven system:

Funds ranking in screeners: Performance Consistency and Quality are two parameters used for ranking funds for SIP. The ranking as follows GG, GO, GR, OG, OO, OR, RG, RO and RR.

With the same color-coded funds, the one with the higher Average 3-year rolling returns (over 5 to 10 years), the number that appears in the Performance tag, ranks higher.

Here is the summary:

The third tag Upside Potential is not relevant for SIP. It is relevant for lumpsum investments in Mutual Funds.

A 5-Step Journey to Financial Freedom

Read this Book for Free.*This Offer is only valid till this month only. Claim it now.

Read NowDid you know that market corrections can actually present great opportunities to buy high-quality stocks at discounted prices? By taking advantage of these times of volatility, you can position your portfolio for long-term growth.

At MoneyWorks4me Portfolio Advisory, we specialize in helping investors navigate market fluctuations and build a strong, diversified portfolio. With our collaborative approach, you can maintain control over your investments while benefiting from our expertise and guidance.

If you're interested in learning more and with a minimum portfolio size of 25 L+, we can help you manage your portfolio, no matter the size. let's connect and discuss how we can work together. And as a bonus, we're offering a FREE Portfolio Review using our "Portfolio Manager" tool during our conversation.

So why wait?

Let's get started today and take your portfolio to the next level!

#Limited slots available.

Do you want to Invest in Undervalued Handpicked stocks and earn high Returns?

Winning and long lasting portfolio is made of Quality Stocks, but how simple is that?

As an Investor most important decision making questions are?

Make an informed decision for Stocks

Invest using an intelligent system with powerful data-driven tools that help you identify opportunities and make informed buy-hold-sell decisions

Buy quality Stocks when they are available at reasonable prices and supported by an upward price trend and Sell when they are Overvalued using the Decizen Rating System. Covers 3500+ stocks

Make an informed decision for Funds

*Color code for outperformance consistency

*Number is average 3 year rolling returns

Want to invest successfully in stocks?

How the heck do you select a solution that ensures it?

Check how good is your current solution!Does it get you focused on meeting your financial goals?

Does it get you focused on meeting your financial goals?

Investing is to means to funding your goals. Your solution must help you get clarity of your goals and how you should invest to reach them. Does your solution include Financial Planning?

Does it have a way of investing that you are confident will work for you?

Does it have a way of investing that you are confident will work for you?

Are you clear of the rationale behind recommendations?

Do you have a way of answering the most important questions: Which stocks are worth investing in, at what price and how do you build your portfolio?

Does it make it easy to find opportunities without wasting your time?

Does it make it easy to find opportunities without wasting your time?

Does it share the tools to enable decision making transparently?

Does it share the tools to enable decision making transparently?

Finally stock investing is all about make informed decisions.

Does your solution provide easy-to-use decision enabling data, information and tools?

Does it help you become a better investor

Does it help you become a better investor

Account Discovery

- OTP from CAMS

Account Linking for Stocks & MF

- One OTP per link Eg. NSDL, CDSL, CAMS, KFin etc.

One Click Upload for your Current Portfolio and Future Transactions!

Don't miss out! First 10 users today get it FREE

With this 4 hrs Masterclass, you’ll be able to:

Take control of your financial future and start building your ideal portfolio today

- with reliable research at your fingertips.

Unlock the Power of Core Superstars Now →

Download APP

Download APP